I have invested a decent percentage of my portfolio in NCL industries in recent times.

Posts in category Value Pickr

What you are buying in this major correction ? PF readjustment! (07-09-2015)

Bought some Hdfc bank Eicher motors gruh finance today.

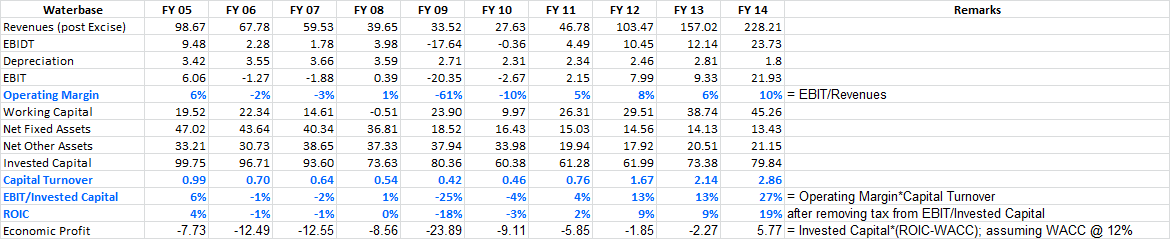

Waterbase – Can it be Next Avanti Feeds? (07-09-2015)

Hi everyone,

I was looking at the discussion on Business Quality: Calculating the value drivers of a business and wanted to tryout similar thing for Waterbase and the numbers look encouraging.

The way i see it is that the company has now started on a path of creating high ROIC and Economic Profit. It would be interesting if someone could do the same exercise on Avanti Feed so that we can compare these two businesses.

The numbers are from screener.in, if there are any mistakes or changes that need to be made let me know (I am new to equity analysis).

Disc: Hold a few shares at Rs.100 level. Currently trying to increase my confidence in the company.

Syngene International IPO – Views invited (07-09-2015)

That’s the strength and main attraction towards Syngene….catering to the entire lifecycle of an NME……it is far superior to any high quality CrAMS players of India…..it builds an extra amount of trust and rarely you will find an innovator moving towards any other CRAMS player than Syngene if it’s involved with NME from the beginning…..Three dedicated centres that you see are the result of the same……I think you are misunderstanding the business model……onus here also is on innovator in case of failure….it is almost identical to PI business model wherein PI is involved with an NCE at process research stage and in case of NCE’s failure, contract provides for take-or-pay…….similarly in case of Syngene, in case of failure there is minimum guarantee fee amount payable by the innovator which covers almost the entire cost or is to be compensated by another NME from the same innovator……

Syngene is a services company in a way and not innovator that you need to understand…..Question arises asto then why an innovator gets involved with Syngene ??? ……The cost of research is rising tremendously every passing year so is the percentage of failure……so innovators are constantly looking at ways to cut cost of research……and if they get a reliable partner which can offer confidentiality, quality and reliability at say 70 % of the cost that they would otherwise have to incur, they immediately go ahead with it,,,,,,Syngene has this advantage……

Lifecycle of an NME is quite long till commercialisation and it is the history of Syngene that is now working in its favour…..similar to the way PI reaped benefits of its 10 year long investments starting 2010, PI seems to be at a similar stage…..three of the molecules where it was involved since the beginning have reached commercialisation stage and ~6-8 % of the total molecules it is working on are in later stages of their lifecycle close to commercialisation……the 1200 cr. investments that you see over next three years are because of this……almost the entire investment will be backed by firm contracts similar to PI which incurs CAPEX only based on firm contracts…….

Kiran M Shaw is not directly involved in Syngene and her intention seems to be to ultimately de merge Syngene after extracting maximum cash from it for Biocon and then eventually pass it on to a professional management or PE backed structure……Biocon is her dream project……as far as her management ability goes, one thing I am assured of is her credibility…..the credibility she enjoys in the industry as well as government circles, she might not do anything to ruin that……its a very clear and transparent management…..otherwise who will bother to announce IPO band before 10 days of opening of issue…..who will declare not only Annual figures but also Q1 numbers before opening of issue……who will immediately after listing post Annual Report 2015 as well Q1FY16 results and q1FY16 Balance Sheet on the website…….all this point to great corporate governance……

When we have past 14-16 years of history for all of us to see…..when we have not only industry players but also company’s employees talking very respectfully for the company……..when we have industry itself likely to grow in double digits in foreseeable future……..its like not believing and finding something ugly which is not there…..although such practice is great on most of the occasions but is not right on all occasions……I see no problem in management…..what many are seeing is history of Biocon but parallely no one is seeing the history of Syngene…..Syngene is now an independent company and now it might find its own valuation multiples in the marketplace.

Rgds.

Kesar Terminals and Infrastructure Ltd (07-09-2015)

Hello all,

Thought I’d share a few nuggets I’d uncovered on KTIL. I just spoke to the company secretary who told me that KMML was basically waiting on two key approvals from the government:

1. ICD – Inland container depot for road logistics

2. PFT – Private Freight Corridor (Railway)

He told me that the work on Phase 1 of KMM was nearing completion and was not yet fully complete. He told me that there has not yet been any intimation from the government regarding the approvals. So that got me thinking and after some googling, I got this link : http://commerce.nic.in/trade/national_tpa.asp

This basically gives links of minutes of the meeting of various ministries for all CFS/ICD proposals (or so I believe). Clicking on one of these links, I got to this page: http://commerce.nic.in/trade/ICD_list.pdf

This page is titled “List of ICDs/CFSs approved by IMC (inter-ministerial committee) which are under implementation or functional” gives the status of all ICD/CFS projects. In this page I found two links lines pertaining to Kesar:

- Kesar Terminal and Infrastructure: Pipavav CFS – I.U.

- Kesar Multimodal Logistics: Powarkheda ICD – I.U.

I.U. means under implementation. From what I could surmise, the ministries have these projects on their approval list. I’m sure certain other approvals are still pending for these projects (PFT, etc) else there would have sure been some sort of notification by the company but I guess it does provide some comfort as to the veracity of the projects and their nearness to completion. I am unable to comment any more on this but thought I’d share and invite some discussion nonetheless.

Disc: Invested

Cupid Ltd – Helping the world play safe! (07-09-2015)

Rajeev

Very impressed with the AR – I get impressed when someone apppreciates the value of relationships built during hard/lean times. Anyway the video shows om garg as a man with a larger purpose. Such entreprenereurs are rare to find.

Waiting for a good correction to get in – its’ a rare indian medical product company that competes across the world and has high ROCE and ability to generate FCF’s.

At an OCF of about Rs. 6 Cr. for FY 15 and an expected Rs. 15 Cr. OCF for this year, a OCF yield of 10 % or so, which means Rs. 150 or so in terms of price, should provide MoS IMHO.

Syngene International IPO – Views invited (07-09-2015)

Mahesh, as usual your research is super.

I think Syngene being involved right from the starting stages of a molecule i.e., Innovation is what makes market think twice on according high valuations. At least until it sees consistency and sustainability or the impact on revenues will no longer depend on molecule innovation.

Contrast this with other high quality CRAMS Players where the costs of R&D, innovation is the onus of MNCs while the Indian companies happily end up bulk manufacturing them with the cost advantages that Indian companies have.

Not invested in Syngene.

Also, I’m not convinced about Ms. Kiran Mazumdar Shaw’s management ability and who after her will run the show – I have not researched enough though. Please throw more light on this aspect of management capabilities.

Thank you so much.

Mutual fund investment first time (07-09-2015)

@sunilsurana Alternatively, you can DIY analysis on mutual fund by learning it through http://freefincal.com/

Hope this helps

ValueQuest moat fund portfolio (07-09-2015)

VQM owns 0.78 % of accelya kale – saw it in AR – built the position during FY 2015. I hold and am bullish too on it

Syngene International IPO – Views invited (07-09-2015)

Prashant…..Not only till FY07 but also go beyond till FY02 which you will find attached in Biocon ARs…If you want to go still further then refer IPO prospectus of Biocon filed in 2004 where you will find data till 1999….Its a real treat to study the company :

14 Years’ Average Pure EBITDA margin (excluding forex effect) of 37.35 %….

10 Years’ Average Pure EBITDA margin (excluding forex effect) of 36.50 %….

Post initial low scale (less than 100 cr.) high margin (43 % +) phase, once company went into 30s in EBITDA margins over last 8 years, average pure EBITDA margin (excluding forex effect) is at 33.77 %….

EBITDA’s conversion to Net Cash Generated from Operations has been robust at 14 Years’ average of 79.70 %, 10 Years’ average of 70.78 % and 5 Years’ average at 65.66 %….

Not only that but even EBITDA’s conversion to Free Cash Flows (FCF) is excellent with 5 out of 14 years showing negative FCF with 9 Years’ average positive EBITDA to FCF conversion at 50.72 %

If we go further to look at health of balance sheet over last 14 years, with a Gross Block addition of 920.19 cr., we have a cash surplus of ~106 cr. in the balance sheet.

Now this is the kind of investment opportunities which a long term investor loves to invest….we have a great history in front of us and with the management confident of continuing with this historical parameters of 30 % + margins, promise of low D/E of not more than 0.5 and an investment plan of 1200 cr. over next 3 years —and this too from a management which exhibits great investor friendliness — an example — you have balance sheet published each quarter instead of half yearly requirement…

When I summed up all and looked at the future with just sustenance of 28 % + EBITDA margins, 50 % + EBITDA to OCF conversion, Asset Turn of just 1.1 post stabilisation of CAPEX and derisked business model because of focus on only NMEs, I fail to understand why this stock is still trading at discount to PI Ind. and Divis Lab on EV/EBITDA basis….Over next few quarters I expect majority of shares getting into the hands of pure long term funds and not remaining much with public category as with a free float of only 12.2 % equity capital or 2.44 cr. equity shares, at current market price of 320, only half the amount invested by funds in parent Biocon, can absorb the entire free float of Syngene……study of history of PI Ind as well as Divis Lab is a perfect case study for this as I remember once fund interest picked up, public category shrinked from ~11 % to 7-8 % with a simultaneous rerating in PI ; similarly in Divis, once fund interest picked up, public category shrinked from ~20 % to ~6 % with a simultaneous rerating.

Let’s keep our fingers crossed and hope the anomaly gets corrected soon by Mr. Market.

Rgds.

Discl. – Invested.

Note — This is not a buy/sell/hold recommendation and is just part of a general discussion.