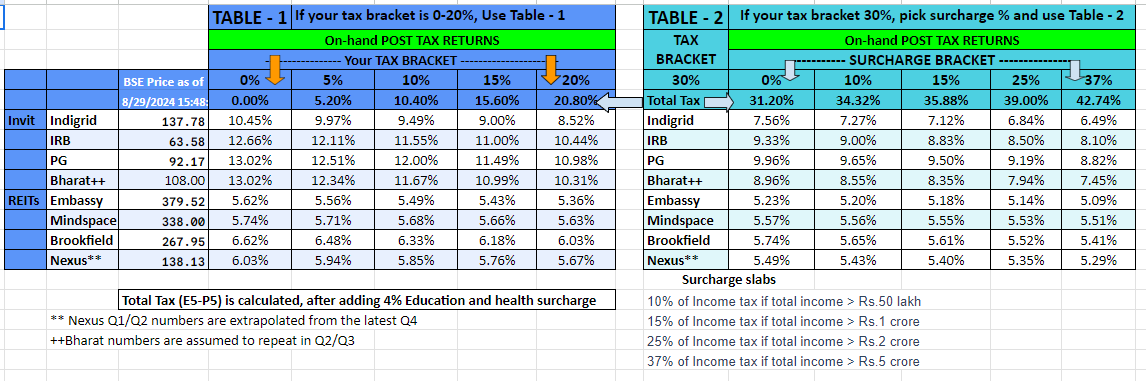

I have added Bharat Invit (assuming that the remaining quarters, will continue with same distribution, as their recent annoucement…in fact, that is their guidance as well) to the table

I have added Bharat Invit (assuming that the remaining quarters, will continue with same distribution, as their recent annoucement…in fact, that is their guidance as well) to the table

I have added Bharat Invit (assuming that the remaining quarters, will continue with same distribution, as their recent annoucement…in fact, that is their guidance as well) to the table

The call transcript from RACL Geartech Limited’s Q1 FY 2024-25 Earnings Conference Call, held on August 23, 2024, discusses several key points related to the company’s performance and outlook. Here is a summary:

RACL Geartech is navigating through a challenging period with a focus on maintaining growth, improving operational efficiency, and exploring new business opportunities. The management is confident that the current global challenges are temporary and that the company is well-positioned for future success.

Sure, I’d be happy to share my thoughts on Anand Rathi Wealth Limited (ARWL).

When it comes to wealth management, especially in the HNI (High Net Worth Individual) segment, trust is the ultimate differentiator. Unlike other sectors, building trust or a strong client relationship in wealth management takes years. And once you have that trust, it becomes a powerful competitive advantage. The wealth management business itself also has several inherent strengths compared to brokerages or other financial players.

1. Scalable and Asset-Light: First off, wealth management is a highly scalable and asset-light business. You don’t need heavy capital investment to grow, unlike traditional financial services like lending. This means they can expand rapidly without significant additional costs.

2. High Return Ratios: It typically delivers high returns on capital employed (ROCE) and return on equity (ROE). This is because wealth management firms generally have lower fixed costs and, with the right strategy, can achieve significant revenue growth without a proportional increase in expenses.

3. Less Volatile Compared to Brokerages and AMCs: Wealth management is also less volatile compared to brokerages and asset management companies (AMCs). Brokerages are directly exposed to the stock market’s ups and downs, which can make their earnings quite choppy. On the other hand, a big chunk of wealth managers’ AUM (Assets Under Management) is in debt instruments, which tend to be more stable. This means their AUMs don’t swing as wildly with market movements.

4. Multiple Growth Drivers: The success in wealth management comes from a few key growth drivers. First, AUMs naturally grow with market returns. Second, satisfied clients tend to give more of their wallet share, refer friends and family, and build a positive reputation for the firm. Third, as new Relationship Managers (RMs) join, they bring in their client base. All these factors together create a ‘lollapalooza’ effect — a compound growth driven by multiple forces working in tandem.

5. High Entry Barriers: Another point is the significant entry barriers in this space. Unlike lending, where people receive money, wealth management requires people to trust you with their hard-earned capital. That level of trust doesn’t come easy; it takes years to build and is incredibly hard for new players to replicate. Anand Rathi has established itself as a highly trustworthy name in this space, which is a significant competitive moat.

6. Untapped Potential in the Wealth Management Sector: We’re still just scratching the surface in wealth management in India. A large portion of the country’s wealth is held by HNIs and Ultra-HNIs (UHNIs), and this group is growing rapidly. Plus, these individuals are starting to realize that the best returns often come from financial assets rather than traditional assets like gold or real estate. So, there’s a huge market opportunity waiting to be tapped.

On the Valuation Front: Yes, the valuation may seem high right now, but given the growth potential, the asset-light model, the high ROCE, and the significant moat around its business, Anand Rathi falls into the category of those rare companies like Asian Paints, HUL, and Nestle when they were smaller. These businesses looked expensive at one point, but their strong fundamentals and growth trajectory made them great investments over time.

So, while it might look pricey today, the fundamentals suggest it could be a great long-term bet.

CSD All India volumes should be 15 K for Indri and for CmiKara can be another 15-20 K ,

PMF volumes can be 5K for Indri and 4k for Camikara Rum

WEALTH CREATION IN INVESTING.

Having interacted with a lot of fellow investors who have made it big in the last few years, one thing that comes across is that the difference between the men and boys is in the kind of outsized bets the successful investors manage to take. Now this term BIG is a bit confusing.

For a reasonably diversified investor say having 15-20 stocks, levels of 10-15% allocation may be big whereas for those who hold less than 10 stocks, anything between 20-30% is big. I have seen folks take nearly 40-50% allocation on their best ideas.

It is for an investor himself to decide what is big for him/her.

There will often be times when there are 2-3-5 equally attractive ideas to bet on and in such times one has to use prudent judgement to allocate capital in terms of ranking of attractiveness.

The key attribute here is that you have to know what you are buying and what are its triggers. What are the key monitorables in the company, and when to exit when things do not appear to be going right.

There has to be no emotional attachment to the company you own. If facts change, act fast and decisively. There is no place for hope or hail Marys. The markets don’t care for your Egos.

Once an idea is identified, and investment is done, usually it is done at a very attractive entry point, because that is where good investors excel. Their risk reward is clearly defined. And if and when the stock price starts moving in your favor, after rally ( can be brief or prolonged) there will be periods of pause, inspite of continuous positive developments.

Initially when the idea is identified, picture is not very clear, and there is a lot of intelligent guesswork, scuttlebutt etc involved. But as time progresses, new facts, new data points emerge to make the picture more clear. When this happens, the periods of pause, consolidation are the times when position can be scaled up. There will be folks who start off with big allocations and after run up are hampered by overall portfolio allocation to the particular big idea. For them scaling up is difficult, though some really smart and aggressive folks do manage to scale up. But for others with space to scale up, it makes sense to scale up. It always makes sense to keep up with the developments in the company and sector in question by going through concalls, scuttlebutt, attending the AGMs, or meeting management at any possible time, going through useful resources like good write ups on relevant VP threads etc.

This is often the most difficult part of the whole process. Often times because of the mind blowing rallies in the big idea, investors tend to get into inertia mode and are often carried away by price momentum and keep holding inspite of dark clouds on the horizon. There will be times when the picture becomes darker, or other times when run up has been so strong that there is mismatch in price performance. Stocks often start factoring in earnings of next 2-3-4 years. If this kind of scenario emerges, one has to take action, often going against contrary public opinion.

Exits can be in form of tranches, or if opportunity presents itself in form of parabolic moves, in a single shot. This depends on individual mindset.

For faster wealth creation, capital being limited has to work harder and once all the positives are factored in, it makes sense to trim/exit to create fund for the next big idea and next big allocation.

HOW TO REACH ABOVE STAGE IN AN INVESTING CAREER.

Most important factor in being capable to bet big is to be ready as an investor.

Learn the important aspects of investing. Do not take short cuts in terms of You Tube videos, or short training courses. This is a journey of a lifetime and the beginning phase involves lot of reading and more importantly re reading of good books. If on first reading of a book, things start resonating with you, then read it multiple times till you master whatever is written in the book.

For the sake of repetition, I am listing books which helped me immensely in growing as an investor.

No guesses. ![]() One up on wall Street by Peter Lynch. . For me this was a life changing read and the more number of times i read this book, the more clarity I got regarding various types of companies, market froth, so on and so forth. I must have read it nearly 12-15 times and still enjoy re reads. Easy narration, good wit and clear articulation.

One up on wall Street by Peter Lynch. . For me this was a life changing read and the more number of times i read this book, the more clarity I got regarding various types of companies, market froth, so on and so forth. I must have read it nearly 12-15 times and still enjoy re reads. Easy narration, good wit and clear articulation.

How to make money in stocks by William O Neil. I am guilty of not reading this book multiple times and aim to correct it over time. But having read some books that are offshoots of learnings provided in this book, like The next apple, or the Minervini books which basically are momentum investing books, we get a fair idea about what O Neil preaches.

Five rules for successful stock investing by Pat Dorsey. This is the book which deals with science part of investing. You can latch on to an idea from whatever source. But analysing that company in details needs some skill because betting big on the best idea requires a lot of clarity of thought, and a detailed analysis is a good way to reach there.

There are many more books, but in my view the above list is the absolutely must for someone with no background or formal education on subject of investing. Make notes of your learnings and try to formulate a mental template of how to analyse a particular company and a particular sector.

Keep learning and trying out new things even if initially it is shunned by most people, or it appears difficult to learn or master. Given enough efforts, very few things are too difficult to learn. Don’t brush off anything in the process of learnings. Learn to get rid of your biases while learning something new.

Few years back, I had seen people bad mouth technical analysis and nowadays it seems to be the new fad. I have seen folks who were hardcore Warren Buffett/Charlie Munger fans learn technical analysis and excel at that. Just because WB has denounced technical analysis does not mean it is useless. Its just that he does not need it because he excels at fundamental analysis to an extent that he finds other disciplines of investing useless. But for other ordinary folks like us, it makes sense to have as many arrows in the quiver as possible, to excel as an investor.

This can be in different forms. There is no alternative to common sense when it comes to investing and learning.

If one is a keen market observer and observes and analysis stuff and things, it is a great way of being street smart. Observing froth, apathy, affecting a particular company or a sector inspite of positive developments is often the key to exit in time , or find winners respectively.

If someone is a regular visitor on forums like VP, then a keen observer will be able to discern who among the boarders are the smart, generous, honest and forthcoming folks. Whose ideas click more regularly over time. Learn to read whatever they write and try to absorb and analyse.

Try to find out whose style resonates with your style and follow him regularly.

This is a big turn off for any person. When someone asks a question “What do you think about this company? , without providing any kind of background on the company it is a big turn off for folks like me. It tells me that the guy asking the question has not done any hard work and just wants spoon feeding. For the sake of nicety, generous people will provide reasonable answers, but those will be brief. If a question is asked, it has to be with proper background information and with such relevant details that the guy answering feels pleased and excited to respond to it.

Spoon feeding is not going to take you places. It will provide you with an idea or two, but the most important aspect in betting big, which is conviction will be lacking. That’s where sincere and systematic learning comes in. Idea is to learn the process from anyone ready to teach, rather than get ideas straightaway.

FINALLY once you have reached the place you have desired to reach, be ready to share. Sharing learning is the biggest form of philanthropy. Provide a helping hand to someone willing to learn and do the hard yards.

AVOID BOASTING. Dont blow your trumpets and keep publicising your winners or success. It is the first step towards destruction and desolation.

In Motilal’s case it’s not true. While AMC business tends to be cyclical, linked to market cycles, wealth management business is a lot more secular. MFS’s revenue mix is more concentrated towards wealth management and that’s why stock is getting rerated.

Stock is still trading below 10 year historical averages so I don’t see any concerns for valuation, especially in the light of their increasing focus on wealth management which commands higher valuations than an AMC business.

Ethos has launched much awaited Favre Leuba watches in Geneva watch days today.

Can be read here:

https://www.watchpro.com/historic-watchmaker-favre-leuba-brought-back-for-a-third-life/

hi Shail, I did allocate 6% of my portfolio to HDFC long duration couple of months back and now sitting at 4.49% absolute return since last 6 months.

With markets being very high i would like to reallocate 6% more from equity to debt. Do you suggest to choose HDFC long duration? I was reading somewhere that constant duration (or something similar sounding) may be a better choice as they adjust debt duration with the interest cycle.

regards