Can you please share the source of con call …thanks

Posts in category Value Pickr

Alembic & Alembic Pharma (27-08-2015)

Hi Rohit,

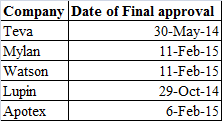

Please find below the date of approval for the generic players for gCelebrex:

The good thing about gCelebrex is its a pretty big molecule and still there are limited players in the market for it. I am not sure on the price erosion front but given limited competition, I dont think it would be more than 40 – 50%. May be we can go through Lupin concall and get the data if available.

Fluidomat – Where perfection meets technology (27-08-2015)

@chiragjain1976

Yes, But if you see the figure 40lacs annual salarie may not be so high for CMD. Isn’t it?

Is there any regulation?

Triveni Engineering – Special Situation- Loss making business hived off (27-08-2015)

Triveni group has strong tie ups with industrial sector and with General Electric for technology and exports.

Triveni Engineering has announced demerger of its loss making sugar & allied business, along with all related assets and liabilities into a separate entity.

Market Cap – Rs.600 Crores,

CMP – Rs.22

Debt – Rs. 1258 Crores (mainly owing to sugar business working capital)

Holding in Triveni Turbine Ltd (@21.8%) = ~ Rs.700 Crores

Shareholder having 1 share of Triveni Engineering will receive

– 1 additional share of Triveni Industries Limited . The loss making sugar business Triveni Sugar Limited having a turnover of ~Rs.1900 Crores will be a subsidiary in this business.

What is interesting, of course is the Engineering business that remains. Make in India and strong relationship with GE at the start of the capex cycle should provide a good upside with low downside.

FY 2015 Engineering business

Sales – Rs.300 Cr

PBIT Rs.25 Crore

Order book of 600 Cr+ (mainly in Water business)

Gears business

– Tie up with GE Lufkin

– 60% market share uses technology from GE for higher power gears

Excerpt from BSE Announcement : The major boost in exports is expected to come from the sourcing drive of major OEMs including from GE–Lufkin, GE Oil & Gas and the business is having good enquiries under this arrangement.

Not strictly comparable but Triveni Turbine which has similar arrangement with GE is quoting at 5 times Sales

Water business

This business is focused on providing world-class solutions in water and waste-water treatment

to customers in industrial and municipal segments.

Latest management update link below

http://corporates.bseindia.com/xml-data/corpfiling/AttachHis/CBF4485D_438B_4442_864B_8EABC12D5A5A_202049.pdf

Views invited for forming a better opinion on this special situation.

Disc : Invested @ Rs.24

ValueQuest moat fund portfolio (27-08-2015)

Can you please provide the source of his exit from vaibhav global

Fluidomat – Where perfection meets technology (27-08-2015)

Generally CMD remuneration upto 4-5% of the profit is considered reasonable and at optimum levels. 7.8% is definitely very high.

Premco Global — Narrow Fabric (A critical component for inner wear) (27-08-2015)

Really worried by the sequential drop in stock price despite good results and cheap valuation.

Can anybody tracking the stock explain the reason ?

Not worried about stock price, but anything happening which I may not be knowing.

Disc : Invested from 445 levels. Now at same level from 731

Ambika Cotton Mills (27-08-2015)

I would say that wind mills were required for securing the power, which was scarce in Tamil Nadu. So I would still call it capex. Though agree with other points.

Alembic & Alembic Pharma (27-08-2015)

I saw on Pharmacompass that Mylan and Teva had an exclusivity period on this which expired on 2nd June. So Alembic is a late entrant in the game. This was not the case in Abilify, which was a day 1 launch. So it may be difficult to take market share. What do you think?

Other players are

Teva

Mylan

Lupin

Apotex

Watson

Looks like Lupin has already been exporting to US

Ambika Cotton Mills (27-08-2015)

Hi, please note that a lot of capex in past has been for setting up windmills and thus not on core plant machinery. Capex in windmill besides providing low cost power on LCOE basis, also provided tax savings (accelerated depreciation of 80% in one full FY in the year of investment).

I am not much conversant with balance sheets, but someone into it can perhaps explore how much capex has been in windmills and plant machinery. This should provide a better view on FCF. Infact, it will be helpful if such an analysis can be posted here. Many thanks