- 70% export from US. Most of the export market is developed country and hence get INR depreciation advantage for this year.

- Some one can expect 30% EPS growth expected in FY16.

- Debt can be 0 in FY18 basis if they grow only 15-20% on current earnings.

- Huge potential at current level at 19 p/e with long term prospect of 3-4 years. Very rare combination we can get for such company.

Posts in category Value Pickr

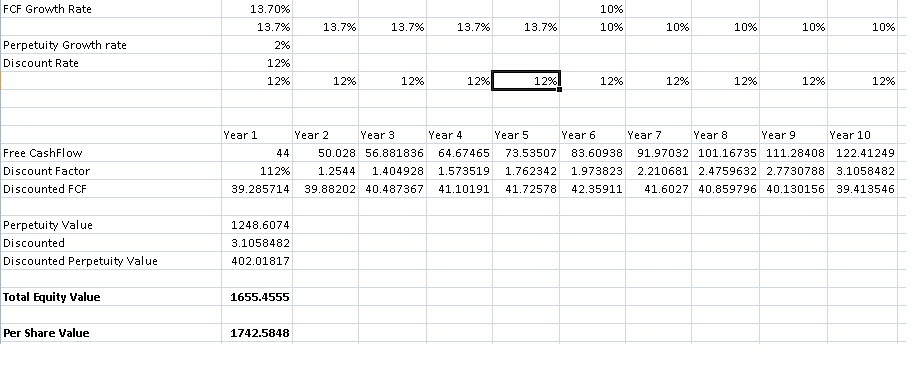

Indocount notes from AR (26-08-2015)

NGL Fine Chem-Re Rating Possible? (26-08-2015)

ICRA Upgrade the NGL rating from A3 to A3+

ICRA ratings for Indian debt instruments-Aug 26

NGL Fine-Chem Ltd ST: Non-FB A3+ 35.5 Upgraded from A3

Hitesh portfolio (26-08-2015)

@kapil1301

http://www.forcemotors.com/page/index/assembling#&panel1-1

Though not too much information is given.

Hitesh portfolio (26-08-2015)

Hi Hitesh,

I wanted to know ur views regarding Force Motors.

My rationale for it is

Market Cap of 3100 CR Debt To Equity 0.02 Mcap To Sales 1.29

Although we cannot directly compare it to Atul Auto But it seems cheaper on above parameters.

Also it manufactures Engines for Mercedes and BMW.

There Operating Margin Seems to be Stabilizing near 11 (Quatrely OPM)

They are a Dividend Paying Company

Comapany is is operations Since very long have been acuired by Jaya Hind Group

Above points Plus the Strong Presence of Their Force Traveller and also increasing number of luxury cars in India (BMW and Mercedes) Gives me Confidence.

(Form My Office to Home in a stretch of 9 Kms I almost site 40 Force travellers)

However I went Through their last Annual Report in that there was no mention of manufacturing of engines

for Merc and BMW also on their site their is no information of these products.

Also one general question

What do you do in such situations where U r seeing the the Company products are being used company posting decent numbers paying dividend but information about their products are not fully covered in their Website or AR.

Regards,

Kapil

How do we get more women investors participating? (26-08-2015)

Here is an interesting article relevant to the thread:

Hitesh portfolio (26-08-2015)

Hi Hitesh,

Please let us know how to manage cash % part of PF. Do you prefer to keep the Cash in regular bank and getting FD returns (or) to keep invested in stable business say (ex: HDFC Bank) to move them for purchases.

Torrent Pharma — Have done the AR and investor presentation reading. Q1FY16 itself they’ve given 48 EPS due to good sales and big NPM. And expected to continue in Q2FY16 as well. Overall FY16 will be more than 100 if we’re including this and valuation will be different in that case.

You’re also using technical analysis (tech-fundo analysis) and it will be great to know the signals (SMA or WMA?) which we may be useful for entry.

Thanks,

-Muthu

Tree house education and accessories ltd. – Potential candidate for improvement in RoE (26-08-2015)

Dear Prashant,

about pledging of promoter’s shares – Would you like to elaborate pledging for personal reasons? Doesn’t this mean that promoters are not interested in their stock itself?

regards,

Ashish

How do we get more women investors participating? (26-08-2015)

This is from the free preview available on amazon…. read on: http://bit.ly/1UczaxY 1

I have read books aimed at popular audience by same author and it have helped me a lot in understanding various aspects of same topic.

thought it would be helpful