Has anyone here used SOVERENN who claim to find multibagger stocks early on.

Posts in category Value Pickr

Sakar Healthcare – Tiny Pharma Company for promising Growth ahead (29-08-2024)

EPS has fallen 2 years in a row now. The March 2024 eps is lower than the March 2020 eps. Its trading at a PE of 60 (ind avg is 35). PB is 2.6.

No dividends being paid. Both ROE and ROCE are among the lowest in the industry. Don’t see how such a high PE is justified.

BCL Industries – Ethanol Pick (Capacity 3.5x in Next 2 Yrs) (29-08-2024)

While the Grain based Distilleries, Poultry and Strach industries have been complaining about high maize prices, there are also cases like these.

Regarding allowing FCI Rice and Maize Import, I agree it seems highly unlikely, specially seeing how tentative the Govt has been recently. They would not like to be labeled as ‘anti-farmer’ by allowing imports or preferring ‘fuel over food’ by allowing FCI rice for Ethanol, by the opposition, just before State elections.

Hopefully it is a short term (1-2 Quarters) issue.

SastaSundar Ventures Ltd (a new venture in the nascent epharmacy space) (29-08-2024)

There is another company recently listed as Entero Healthcare Solutions Ltd Leading Healthcare Product Disributor The company is among the top three healthcare distributors in India in terms of revenue. Please comment on this company as well. I think the business now similar to SVL.

Laxmi Organics – Indian Specialty Chem Candidate (29-08-2024)

Co doesnt seem to offer enough risk reward even at these current levels,

Mgt guided for 2x rev, 2.7x ebitda, & capex of 1000cr (fy24-fy28),

assuming dep -200cr, int cost – 20cr, tax – 29%, gives a 400cr PAT by FY28

@25xPE, this results in 10,000cr.

current mkt cap is 8000cr. A 25% appreciation in 4 yrs from current level, if mgt executes perfectly.

not enough risk reward

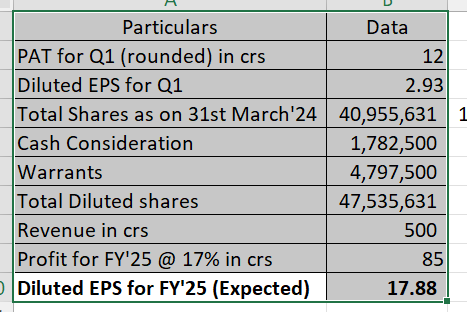

Kilburn Engineering – Huge undervaluation (29-08-2024)

I did some digging and found this to be true.

Promoter group had lent funds from Mcleod Russel to other promoter group companies. And those promoter group companies were loss making and had no capacity (or intention) to pay back. Interestingly, another promoter group company Eveready (the famous battery maker) has been struggling due to leverage.

To make it further complex, there’s a family dispute between Aditya Khaitan & Amritanshu Khaitan over certain family properties – Both of them are on board of Kilburn Engg.

To summarise, promoter group created financial troubles via leveraging for operationally wonderful companies and w/o those loans these companies fortune could have been different!

Moving to Kilburn, my observations (on which I would like comments from the fellow members)

- There’s not much leverage (Net debt of 0.2x as Mar’24);

- But the Company has been diluting continuously – may be they have learned the lessons and want to stay away from leveraging – But still this will have an impact on the EPS growth

- The positives (revenue growth) about the company have come in post joining of Ranjit Lala as MD who actually has relevant experience (PS: other promoter group companies too had professional management)

- Have done a simple projected EPS calculation:

Pls share your take on the same.

Source article on Family/Promoter group:

Disc: Invested at current levels

Manappuram Finance (29-08-2024)

It’s fascinating to observe how people’s perspectives on book value vary. When the book value was less than 1, many argued that the business was unsustainable. Now that the book value has risen above 1, some feels it’s bit expensive. Meanwhile, Manappuram continues to grow steadily at a long-term average rate of 15-20%, with its price-to-earnings ratio consistently remaining below 10 as it keeps growing more than the price movement

Cyclicality tends to balance out over time, often leading to significant growth following periods of flat performance. The long-term upward trend in gold prices provides an additional boost to growth. Inflation also contributes to this growth. As a developing country, India will continue to have a strong demand for money, and it will take decades for India to reach the status of a developed nation when growth may slow ( but even in developed nations microfinance sector is growing )

These differing perspectives are what keep the market dynamic, ensuring that at any given time, there are always both buyers and sellers actively trading.

———

Typically, when a business trades below its book value, it’s often due to some underlying issues the company is facing, leading people to wait for clarity and resolution before investing. However, once the situation improves and clarity emerges, the stock often becomes more expensive. If you buy at a price below book value and the issue remains unresolved, the price may drop further, making it a risky move. Therefore, it’s rarely a guaranteed win. Luck plays a significant role when investing in a company dealing with multiple challenges—if the issues are resolved, it can result in substantial returns.

——-

Anything can happen but current valuation ( single digit pe and double-digit growth ) seems paradoxical to me

And I am accumuling it at regular intervals )

BCL Industries – Ethanol Pick (Capacity 3.5x in Next 2 Yrs) (29-08-2024)

Maize prices strong and expected to go higher in Sept and Oct – till new harvest starts.

Advait Infratech: A detailed analysis (29-08-2024)

What is the source of costs that you have mentioned for manufacturing electrolyzers

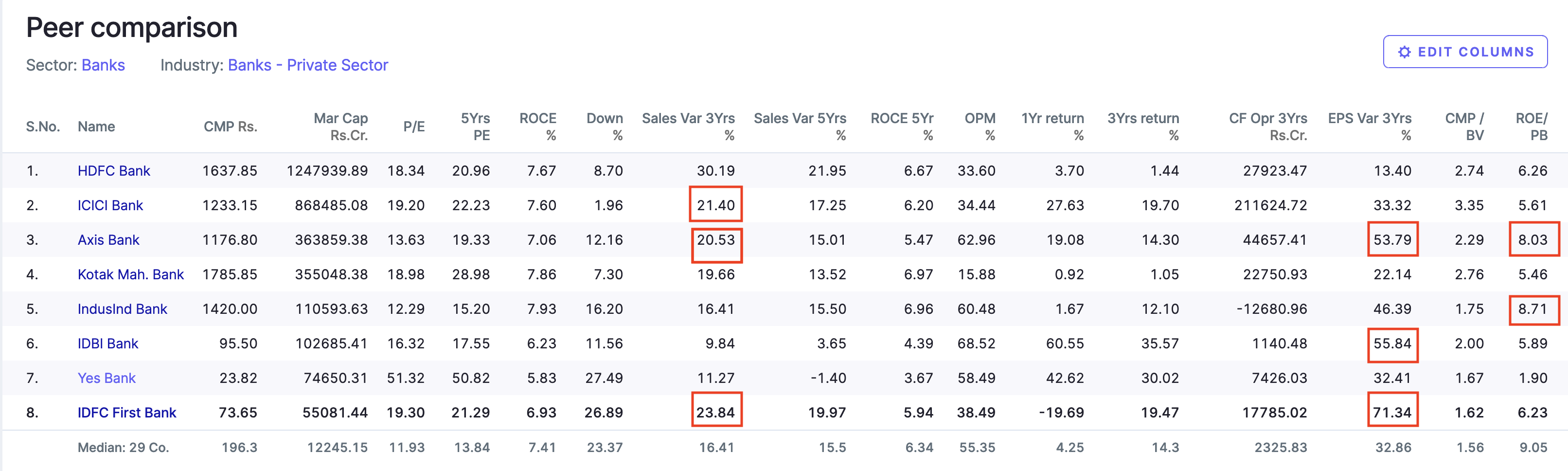

IDFC First Bank Limited (29-08-2024)

Peer Comparison of IDFC First bank

While IDFC has the best sales/EPS growth, but so is its valuation. Axis and IndusInd looks better in terms of valuation.

Theoretically, ROE/InterestRate should be equal to P/B. In these terms Axis Bank looks the best valued with decent growth

Matter of fact is Private Bank ETF that started in Sept 2021 has given similar returns to IDFC first bank with no concentration risk