(post deleted by author)

Posts in category Value Pickr

Bulk Deals Bi-Weekly Log (28-08-2024)

Thanks for insight,keep up the good work

MOLD TEK PACKAGING—dividend plus growth (28-08-2024)

Hi Narendar, the company has a health balance sheet if you look at the Net Debt/EBITDA or interest coverage ratios. They can sustain 30%+ dividend payout without really hurting the balance sheet so by paying a dividend they send a positive signal into the market. Also, the capex need of the business has reduced relative to last few years and this a good cash conversion business. If they hoard this cash on their balance sheet the returns will get impacted so net net its a positive that they do pay dividend while keeping a relatively healthy balance sheet

Narayana Hrudayalaya Ltd (28-08-2024)

Narayan Hrudayalay.pdf (155.2 KB)

Disc: Invested

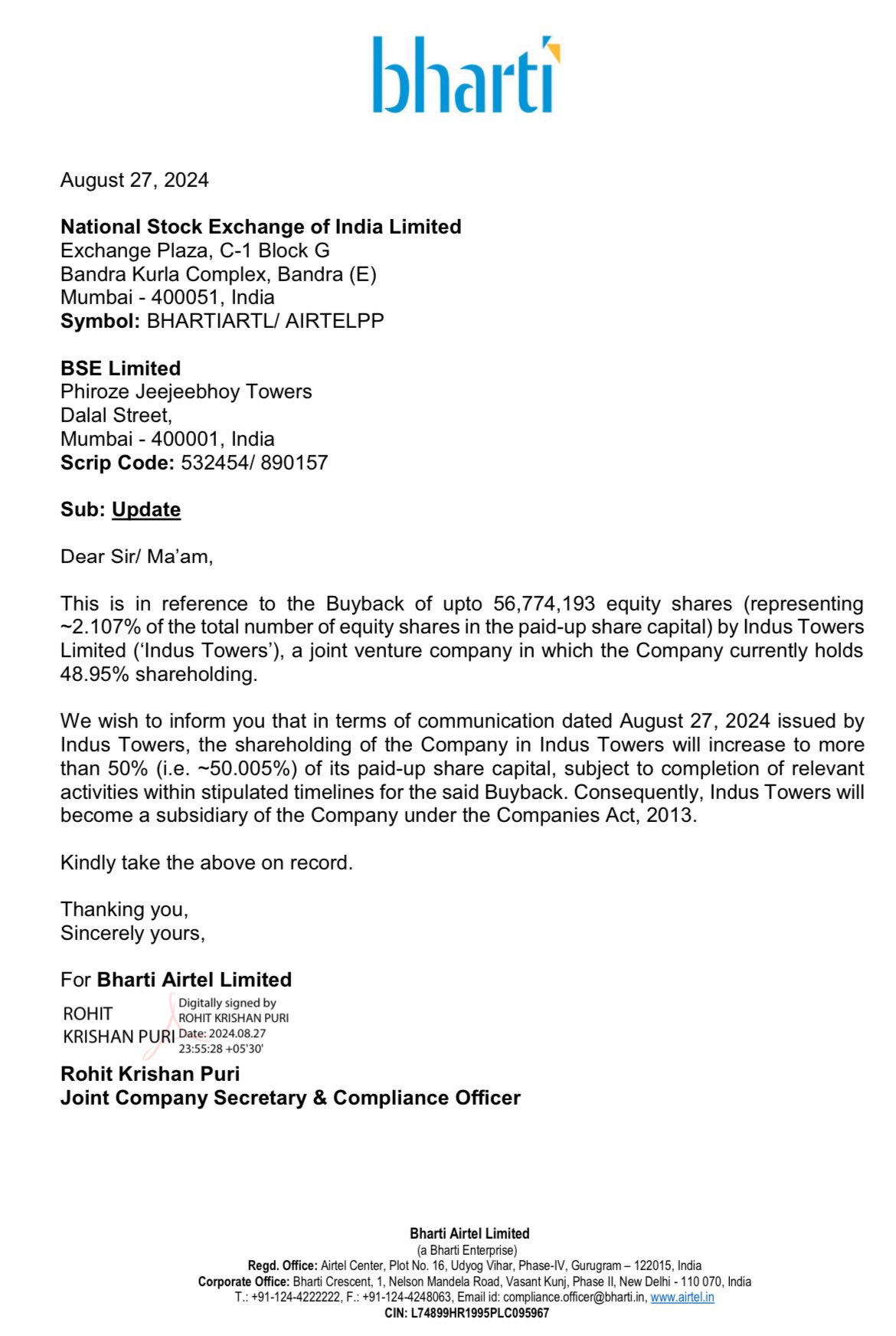

Bharti Airtel – What doesn’t kill you makes you stronger? (28-08-2024)

Indus Towers will become subsidiary of the company post buyback under the companies act 2013 as shareholding of the company will increase to more than 50 percent of its paid up capital

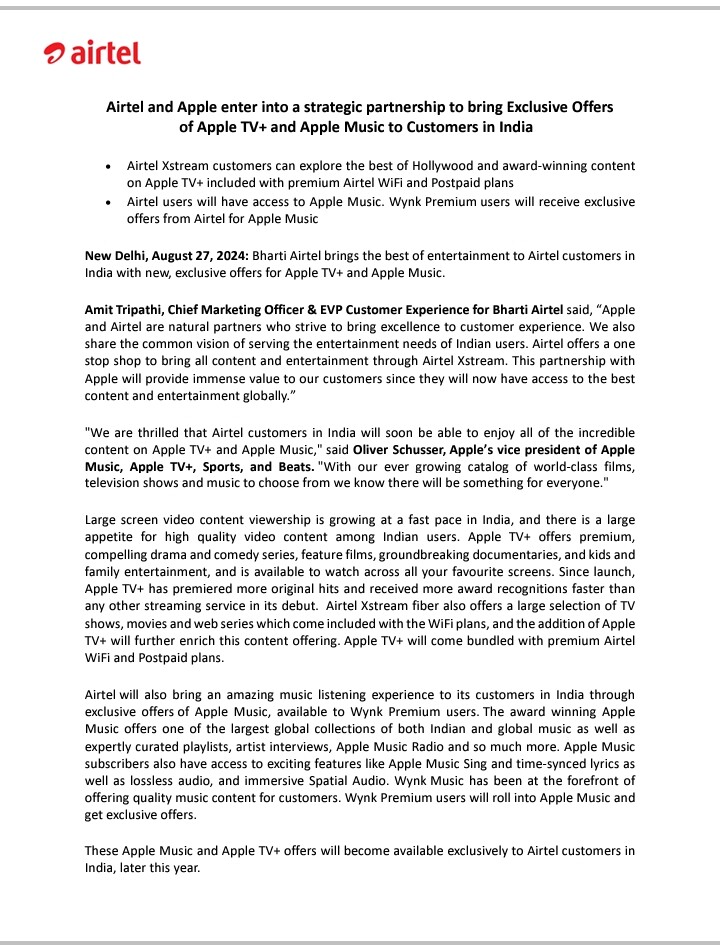

Airtel and Apple enter into a strategic partnership to bring Exclusive Offers of Apple TV+ and Apple Music to Customers in India

Disc-holding not buy/sell recom

Varun beverages fast growth duopoly business (28-08-2024)

Analysis of Varun Beverages Limited (VBL) – Focus on the Indian Market

Industry Overview:

The Indian non-alcoholic beverage industry is projected to experience varying growth rates across different segments in the medium term:

Carbonated Soft Drinks (CSD): Mid single-digit growth

Packaged Drinking Water: High single-digit growth

Juices: Low double-digit growth

Sports Drinks/Energy Drinks: Mid-double-digit growth

Major Players: Coca-Cola and PepsiCo dominate the market.

Growth Drivers:

- Climate: Increased temperatures boost demand for beverages.

- Demographics: A youthful population drives consumption.

- Urbanization/Rising Income/Household Spending: Higher disposable incomes and increased urbanization fuel beverage consumption.

- Rural Advancement/Rural Electrification: Improved infrastructure and access in rural areas enhance market reach.

Varun Beverages Limited (VBL) Overview:

-

Relationship with PepsiCo: VBL has a symbiotic relationship with PepsiCo, accounting for 90% of its sales volume from PepsiCo India. The bottling and trademark license agreement extends until April 30, 2039, covering manufacturing, supply chain, and end-user distribution. VBL operates across 27 states and 7 Union Territories in India.

-

Revenue Contribution: The Indian subcontinent (India, Sri Lanka, Nepal) contributes 83% to VBL’s revenue.

-

Financial Performance:

Revenue Growth: 25% CAGR over the last 5 years.

Profit After Tax (PAT) Growth: 47% CAGR over the last 5 years.

Sales Volume Growth: 17% CAGR over the last 4 years. -

Debt Metrics:

Net Debt (as of June 30, 2024): Rs. 5,808 crore

Debt-to-Equity Ratio (as of June 30, 2024): 0.67x

Debt-to-EBITDA Ratio (TTM, as of June 30, 2024): 1.37x -

Cost Structure:

Raw Materials: Concentrate, sugar, PET chips, packaging.

Franchise Fee: Payment to PepsiCo.

Logistics: Distribution and supply chain costs.

Advertising: Shared and company-specific marketing expenses. -

Profitability:

EBITDA Margin (H1 2024): 25.9%

PAT Margin (H1 2024):15.7%

- Free Cash Flow (FCF): Given significant capital investments and acquisitions (both debt-funded and cash-based), FCF is not currently a primary focus. Conversion of net profit to operating cash flow is more relevant at this time.

Risks:

- Branding/Marketing/Pricing: Limited control over branding and pricing due to reliance on PepsiCo.

- Health Concerns: Growing consumer shift towards low-sugar/no-sugar beverages, with 46% of VBL’s sales volume in these categories.

- Seasonality: Demand fluctuations due to seasonal variations.

- Raw Material Pricing: Volatility in costs for PET chips, sugar, and packaging materials.

- Supply Chain Disruptions: Potential disruptions affecting production and distribution.

- Foreign Currency Risk: Exposure to currency fluctuations in international markets.

- International Exposure: Risks associated with operations in Africa and other international markets.

- Taxation: Potential impacts from changes in tax policies and regulations.

- New Entrants & Competition from CoCo Cola – PepsiCo will take care

Valuation: The stock is currently trading at a PE ratio above 80. Given this high valuation, the market appears to be pricing in most of the known factors and long-term double-digit growth.

Thoughts are welcome.

VIP Industries : Luggage (28-08-2024)

VIP Gross margins and OPM seems significantly impacted. Do you see any recovery to mean and management commentary on the.

Sona Comstar BLW – Direct EV Play (28-08-2024)

Thank you, Murali, for pointing that out ![]() . I missed the recent notifications regarding the PLI. With revenue recognition starting in the next financial year, I’m optimistic about seeing strong numbers in the company’s bottom line next year.

. I missed the recent notifications regarding the PLI. With revenue recognition starting in the next financial year, I’m optimistic about seeing strong numbers in the company’s bottom line next year.

The harsh portfolio! (28-08-2024)

Hi Harsh,

What’s the investment hypothesis for Ambika Cotton?