I am hearing news (not verified) that Saregama is in talks to buy a significant stake in Karan Johar’s Dharma Productions.

This is pretty big, if true. Does anybody here have any info on this?

I am hearing news (not verified) that Saregama is in talks to buy a significant stake in Karan Johar’s Dharma Productions.

This is pretty big, if true. Does anybody here have any info on this?

300 cr raise thorugh warrants at a price of 425 for current and future acquisitions, debt repayment, expanding operations and future expansion.

Major 200cr out of 300cr is by promoter group, 20crs by shareholders of Monga

Strayfield Private Limited and rest 75cr by non promoters.

Very well poised to achieve 500cr revenue this year and also hints on company’s future acquisitions to increase synergies and grab group orders.

In the concall, company has guided for 100cr revenue of ME energy in FY25 which it acquired last year and had a revenue of 30cr.

So clearly the company enhances its possiblities of converting its enquiry pipeline (currently 2000cr) into orders by such acquisitions. Management also states that they do not proceed with another acquisition till they finish one. Management has walked the talk for the last 4-5 quarters.

Interesting thing is promoters infusing money into the company even after a big surge in stock price in last 1.5yrs.

press release for acquisition.pdf (320.0 KB)

Kilburn warrants disclosure.pdf (381.4 KB)

Disclaimer : invested from lower levels.

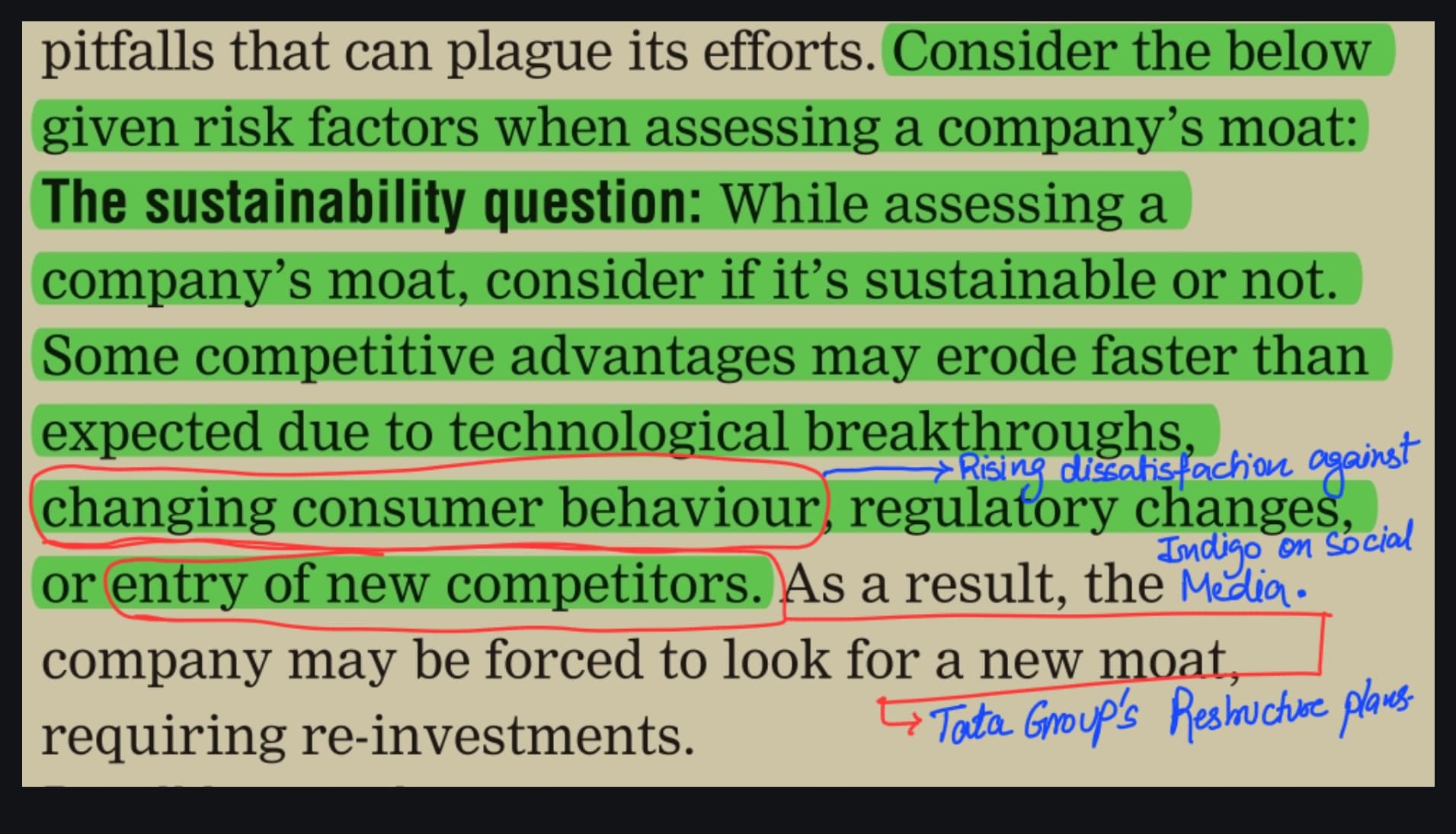

My thoughts aline with you. Recently, i had noted this down in my notes [image]. The indigo’s pricing and market share moat may be under danger as times pass due to increasing customer dissatisfaction and entry of lovable competitor (tata group).

as per Motilal oswal

Great discussion on smartlink. Thanks for sharing the link to this discussion.

I had a similar view, small unproven company in a interesting space. Promoter is ethical, but capability to take to next level is not proven. This will be on my watchlist to see how things move, and if in required direction.

1st ever Presentation by Batliboi ltd.

Something is changing here, Merger, Foray into CNC Machines, Green Hydrogen, Preferential @ Rs 118.5, few months ago.

(post deleted by author)

Surya Roshni –

Q1 FY 25 concall and results highlights –

Revenues – 1893 vs 1875 cr ( despite slowdown due to elections, price erosion in Steel Pipes and Lighting divisions )

Gross Margins @ 24 pc

EBITDA – 151 vs 114 cr, up 36 pc ( margins @ 8 vs 6 pc )

PAT – 92 vs 59 cr, up 56 pc

EBITDA uptick led by sharp uptick in EBITDA / Ton in the steel pipes business and steady margin improvement in lighting and consumer durables segment

Company is debt free. Cash on books @ 156 cr

Segment wise results –

Lighting and consumer durables –

Revenues – 385 vs 374 cr ( despite 9 pc price erosion in LED lighting segment )

EBITDA – 35 vs 33 cr

Margins @ 9 vs 8.8 pc

PBT – 26 vs 26 cr

Steel pipes and Strips –

Revenues – 1509 vs 1503 cr ( volumes up 7 pc despite slowdown in Govt spending in Q1 )

EBITDA – 124 vs 83 cr

EBITDA / Ton @ Rs 6065 vs Rs 4388 ( on account of better product mix. Value added pipes – Galvanised, API and Spiral accounted for 46 pc of revenues )

PBT – 97 vs 55 cr

Steel Pipes manufacturing facilities –

Bahadurgarh, 53 acres

Anjar, 96 acres

Gwalior, 51 acres

Hindupur, 17 acres

Lighting manufacturing facilities –

Kashipur, 46 acres

Gwalior, 44 acres

Company is largest manufacturer and exporter of ERW pipes. Company is also No-2 lighting brand in India – mainly focussed on rural / semi urban areas

Company is the leading player in Large Diameter pipes, API pipes in India. Their products in these segments command a premium pricing of 6-8 pc over its peers – which is a very big deal in the pipes business. The company has earned this through 40 years to hard work

Fans business showed a 43 pc volume growth

Appliances business showed a 15 pc volume growth

Have launched – residential pumps in Q1

Aim to grow the consumer durables and lighting business by 10-12 pc in FY 25

Expecting 12-15 pc volume growth in steel pipes segment in FY 25

Gross margins improved in Q1 due company’s greater focus on value added products – both in Steel pipes and Lighting segments

Gross margins should further improve wef Q2

Additional capacities of 50k MT ( CR pipes and 8″ pipes ) should come online in Q3. Additional capacities of spiral pipes ( additional 60k MT ) should also come on stream in Q3

Company has lined up a capex of 250 cr and 200 cr respectively for this FY and next FY – for steel pipes division. Post this capex, company’s capacities will increase from 12 lakh MT / yr to 19 lakh MT / yr

Not likely to add any more capacities in Lighting and CD segment for next 1 – 1.5 yrs ( as they have adequate capacities )

Likely to maintain EBITDA / Ton > 6000 for FY 25

Aim to generate an EBITDA of 675 – 700 cr for FY 25

Company believes, there is a strong case for de-merger of both the businesses. The board will finalise the same

Company has good brand equity in the FMEG space. Hence the new launches in recent years ( like fans, pumps ). Company can leverage the same going forward. At present Fans + Consumer Durables account for 18 pc of this division’s sales

Lighting business had a rough past 2-3 yrs due steep price erosions. Going fwd, things should improve as a lot of unorganised and non-core competition is likely to abate. This should augur well for the company

Company is hopeful that lighting division’s EBITDA margins should improve to 12 pc levels in 1-2 yrs. In Steel pipes division also, EBITDA / Ton should improve to > Rs 7000 / Ton due greater focus on value added products ( this should structurally improve the margins trajectory of the company )

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation

Evening Hitesh sir.

Aavas Financier has an open offer (Since more than 25% was acquired by CVC Capital) at ₹1766. The entire process will take almost 2 months to complete.

Is the share price capped at ₹1766 for the time being? What happens/has happened in such situations in your experience?

Thank you

DCX meeting with Singular & Aditya Birla Money this Friday → https://www.bseindia.com/xml-data/corpfiling/AttachLive/957dd3b3-8d2b-43be-9be9-7f9237bff149.pdf

Singular Capital has a very accomplished team → Team – Singular Capital