Jupiter Wagons: ‘Focus Is On Wagons, Capacity Ramp Up’, On Track To Achieve FY25 Sales Target?

Posts in category Value Pickr

Sumit’s Portfolio (27-08-2024)

I sincerely thank you all for the encouraging words and feel grateful that I could share my portfolio for critical evaluation.

My Journey and Lessons Learned

My journey before COVID, when I was investing part-time, was filled with many mistakes. The following are some errors I made during my investment journey (though this is not a comprehensive list):

- Over-diversification (Deworsification): I bought up to 50 stocks without developing conviction in any of them.

- Paying Attention to Just Numbers and Not the Narrative: I used to only look at historical numbers and invest if I found them to be good enough.

- Selling Winners Too Early: I was an early investor in companies like Vinati Organics and Persistent Systems, but I sold them with only marginal returns. They went on to become multibaggers.

- Over-concentration: At certain points during my investing journey, I held fewer than four stocks. It was concentration for the sake of it, not because I had great conviction in the story.

- Not Having an Investing Philosophy: This was a big one. I used to invest purely based on past performance without an investing philosophy.

- Not Tracking: I hardly used to read quarterly calls or annual reports of my holdings, foolishly believing that I should simply hold stocks for the long term regardless of how the underlying companies performed or are performing.

- Not Being in the Market: I used to check out from the market for several months, thereby missing some crucial bull runs.

Immediately after COVID, I liquidated all my holdings and was sitting on cash for a year or so. At this point, I was trying to automate my business so it could run without me. This led me to miss the massive bull run that happened after COVID. This remains one of my biggest regrets. When I realized I had made a big mistake by not being in the market, it was a wake-up call for me, and I decided to dedicate myself full-time to investing, swearing never to miss another bull run again.

I started building the above portfolio in mid-to-late 2022. Investing in SME stocks is a recent phenomenon, except for Beta Drug and Macfos, which I have been holding for more than a year, the rest of the SME stocks were purchased recently (less than six months). I am new to SME investing and hope to increase my allocation as I gain more confidence in the space.

So far, in the last 1.5 years, my portfolio has returned a little over 100%, with Anand Rathi returning 4x, Aditya Vision returning 3.5x, Caplin Point returning 2.7x, and Beta Drugs returning 1.5x.

About Me

I was born into poverty, and growing up with limited means inspired an aspiration to build great wealth. I figured out very early on that in order to be truly wealthy, one either needs to be a celebrity or a business owner. I lacked the talent to be a celebrity, so I focused on becoming a business owner. I figured you can be a business owner either by creating your own business (entrepreneurship) or by buying pieces of businesses other people have created (investing). Since my 12th grade, I dabbled in various business ideas, trying as many as seven businesses until I found success in the last semester of my college. Meanwhile, I always considered investing as my Plan B should I never succeed in my ventures. I soon realized that business was always a means to an end for me and I was never truly interested in entrepreneurship. Investing, on the other hand, always fascinated me, and I am glad that eight years later, I was able to build enough capital base to not have to work and focus full-time on what I truly love.

My (Current) Investing Philosophy

I invest in businesses with the intention to hold them for the long term (5-10 years). I am not very comfortable with churning my portfolio very often. I am comfortable holding a stock even if it hasn’t performed price-wise, as long as the business stays good (case in point: Ugro Capital, whose performance has been muted for a year). I am comfortable because I have observed that most of the returns in a stock come in just a few trading days, and if you miss those days, you will miss a massive portion of the potential returns. Also, once a stock breaks out, it more than compensates for the period of no returns (case in point: Caplin Point, which didn’t perform for several years and suddenly broke out to give 2.7x returns in less than 1.5 years, with most of those returns coming in about 20 trading days).

This buy-and-hold approach forces me to look for long-term growth stories, where market opportunity and size are huge. It also means I must have able and honest management running those businesses, and the financial health of the company must be strong to ensure their survivability across various cycles. This means I invest in companies with management that are good at capital allocation, are financially prudent enough to not take on too much debt, and always balance growth with fiscal discipline.

I have a return expectation of ~25% CAGR from my stocks and only invest in those businesses where I believe this kind of return is possible.

I believe in diversification only when a stock meets my return expectations. This means I will only invest in a new stock when it matches or surpasses my return expectations, and since such ideas are hard to come by, the result is a fairly concentrated portfolio. This kind of diversification helps me sit through times when some of my stocks are underperforming because other stocks often compensate, and the overall portfolio tends to do well.

When I Sell My Stocks

I sell my stocks when:

- I realize there are holes in my thesis that I initially overlooked.

- My perception of the management changes for the worse.

- The future returns from the companies aren’t meeting my return expectation.

- I find a new idea that has much better prospects than an existing one.

I don’t sell when:

- My stocks have appreciated a lot.

- There is fear or greed in the general market.

- My stocks have underperformed relative to the general market.

My Approach to SMEs

With respect to SMEs, the main priority is growth with good management. Since they lack history, I simply optimize for companies growing at 40-50% where management seems to be competent and ambitious. I am willing to pay a little higher valuation for such stocks, although my allocation in such companies will be small.

PS : I am not a momentum investor, nor do I follow a sectoral or top-down approach. While these investment philosophies intrigue me, I haven’t fully delved into them yet. For me, the fact that a sector is currently out of favor—such as the financial sector right now—doesn’t deter me from seeking opportunities within it. In fact, I often find my investment picks in these undervalued sectors, where valuations tend to be more reasonable. My primary focus is on sectors with significant growth potential, irrespective of whether they are currently attracting capital.

Forensics and the art of triangulation (27-08-2024)

Sir,how to use Screener Specter and how to analysis of the company through Screener Spectrer,what is the features of Screener Specter

E-pack durables – ODM worth a serious look (27-08-2024)

There is another thread on E-Pack durables but since it is locked starting a new one. (Admin can merge if deemed fit).

Industry Overview

-

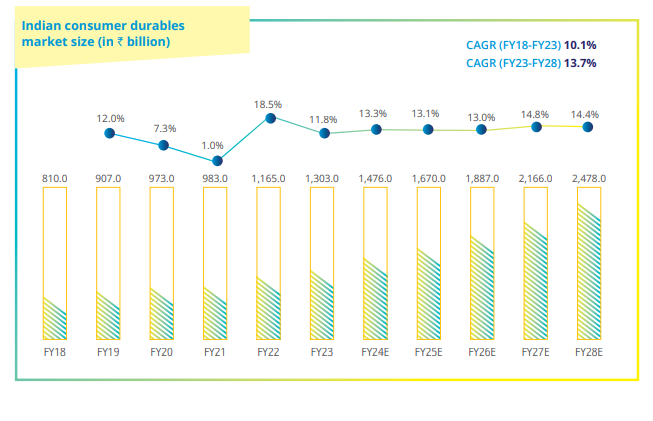

Indian Consumer durables industry is poised to grow from c.1300 bn to c. 2500 bn Rs at 13.7% CAGR from 2023-2028 with significant growth projected from the RAC segment.

-

Indian RAC market achieved a domestic sales value of C. 250 bn Rs in FY23 with volumes reaching 8.4 mn units.

-

This has substantially grown in FY24 due to heat wave conditions in most of India as the same is evident from the numbers reported by all major OEMS and ODMs in AC segment.

-

RAC manufacturers heavily relied on imported critical components (60-70% import reliance) , however the PLI scheme with c. 6500 cr has prompted many OEMs and ODMs to backward integrate.

-

The RAC market is estimated to grow at a CAGR of 12.1 % in volume reaching c.15 mn units in FY28 and 15.7% CAGR in value reaching c. 525 bn by FY28.

About the Business

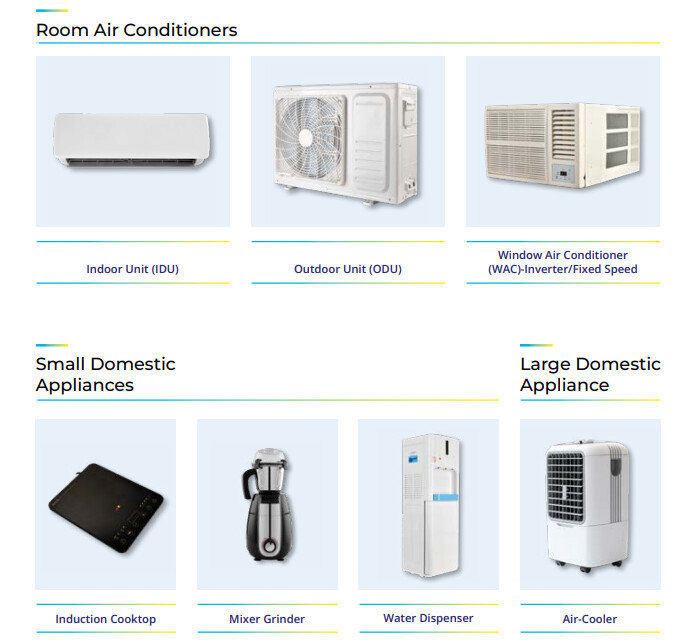

Epack durable is an ODM (Original design Manufacturer) which got listed in January 2024 . They claim to be the second largest ODM for RAC in India.

They also manufacture Small Domestic Appliances (SDA) : Mixer Grinders, Induction Cook top , Water dispenser and are planning to venture into Large Domestic Appliances (LDA) : Washing Machines, Room oil heater, tower fan, Induction water heater, hair dryer etc.

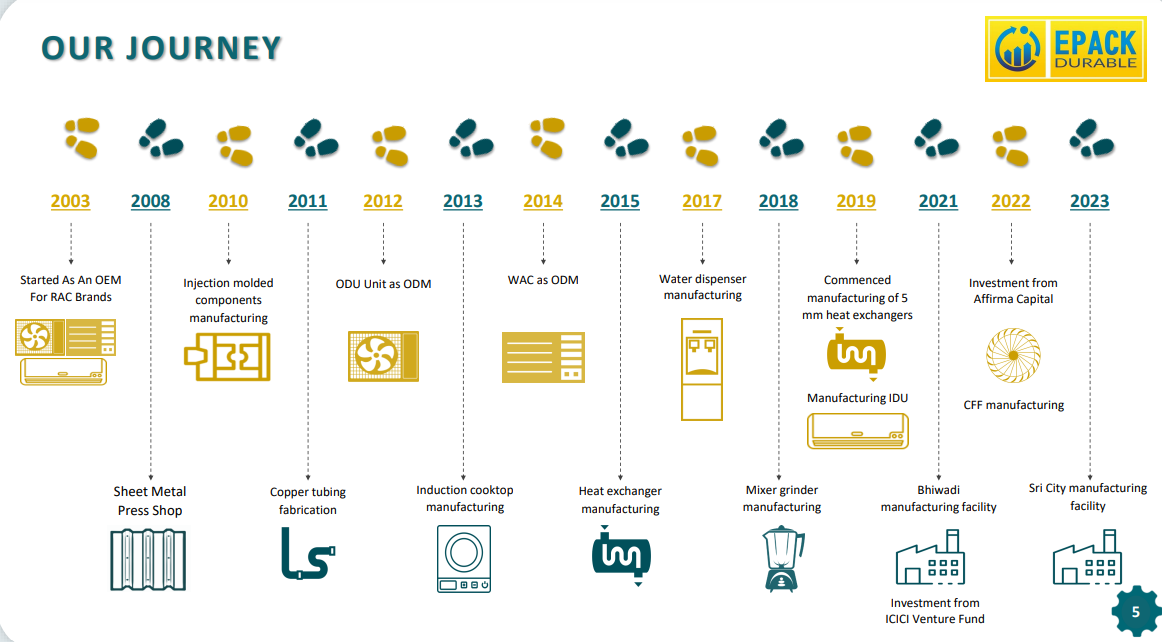

Incorporated in 2003, EPACK Durable (EPACK) started off as a contract manufacturer of

consumer durables such as RACs, Induction Cooktops, Juicer-mixer grinders, and water

dispensers for OEMs.

• Later in 2012 it transformed into an Original Design Manufacturer (ODM) for Air conditioners

and small domestic appliances. EPACK has grown significantly since then to become the second

largest ODM player with a market share of ~24%

• EPACK was founded by the Singhania and Bothra family who have been involved in

manufacturing consumer durables for more than two decades with extensive industry

knowledge and experience.

• It has 3 manufacturing facilities located strategically in Dehradun, Bhiwadi, and Sri city. All the

facilities enjoy strong backward integration offering cost competencies against its peers.

• About 80-85% of the company’s revenues come from the sale of RACs and their components

and the balance from small domestic appliances.

• It has marquee clientele, including Voltas, Haier, Philips, Godrej, Daikin, Havells, Bosch &

Siemens, Bajaj, Crompton & Greaves, Blue Star among others with whom it has established

strong relationships.

• EPACK received a total private equity investment of ~$40 million (approximately Rs. 320 crores)

from ICICI Ventures and Affirma Capital during FY2022 and FY2023 respectively, which was

largely utilized in capital expenditure during FY23 & FY24.

E-Pack has a fair amount of backward integration in its AC manufacturing including heat exchangers, cross flow fans, copper tubing, sheet metal, Plastic molding etc.

Manufacturing Facilities

.

** About the Management**

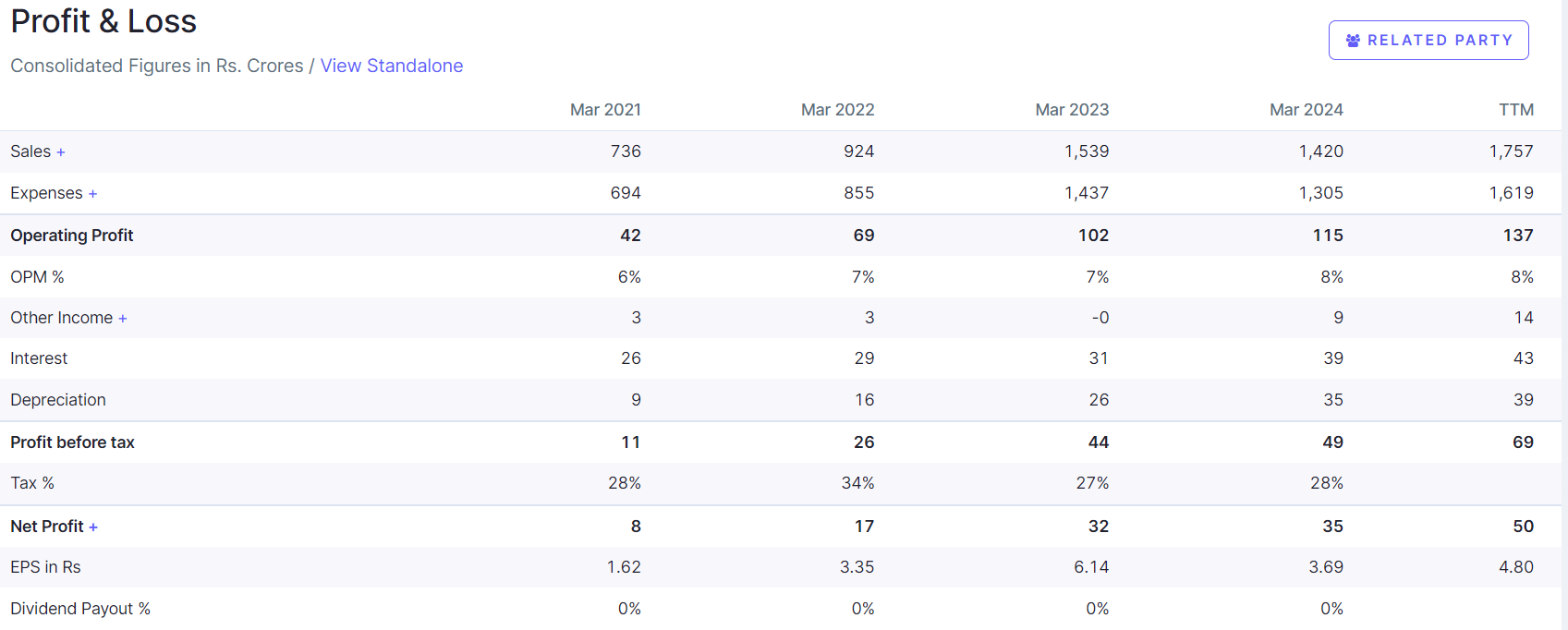

Financials and Valuation

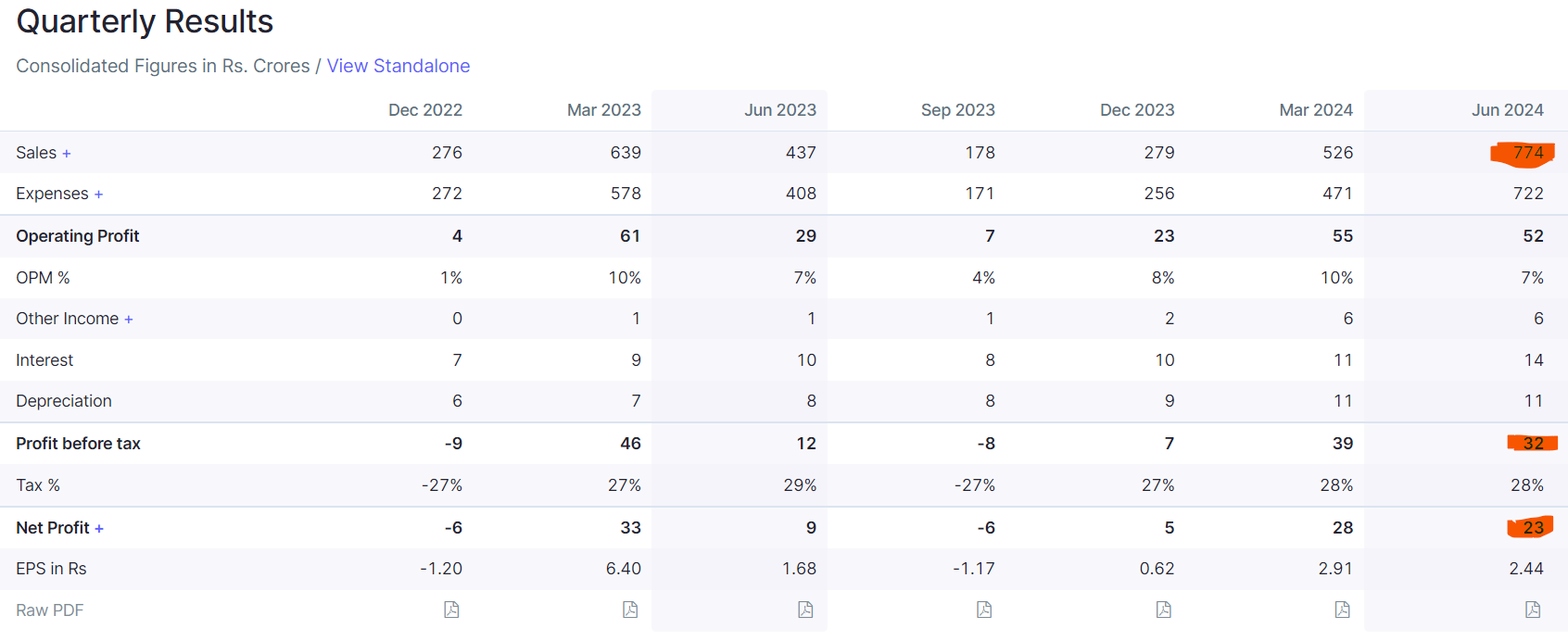

Epack has achieved a 3 yr CAGR of 66% on bottom line.

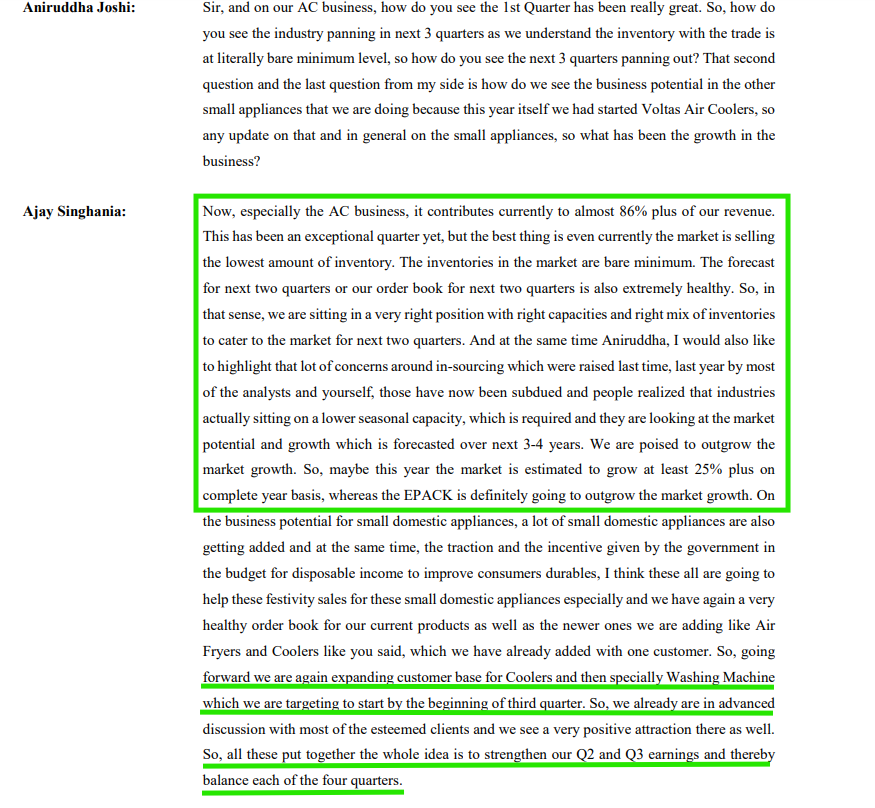

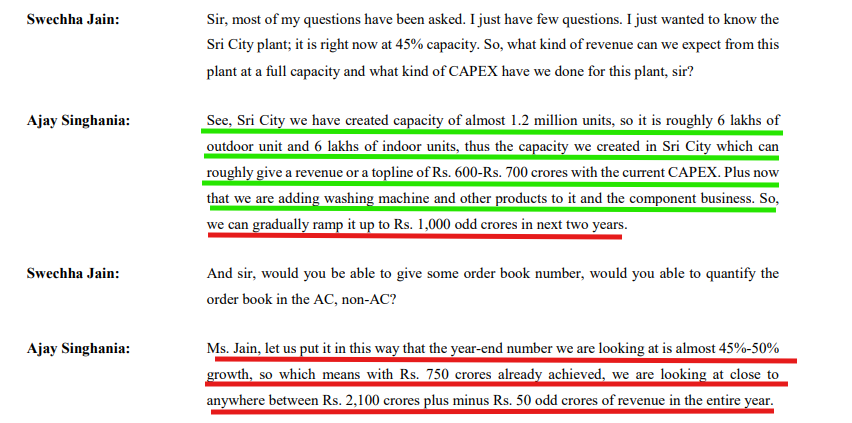

Few inputs from the Concall

-

Reason for lower margins in QoQ is due to Sri City plant getting commissioned and material cost escalation. Due to pass through nature of cost , this can get postively impacted in subsequent quarter.

-

E-pack is starting Washing Machines with Fully automatic Top load variants and have signed with several top OEMs .

-

In FY 25 the total outlay for PLI is going to be C. 37.5 Cr and out of which C. 15cr is accounted in Q1.

-

Epack has acquired 26% stake in associate company EPAVO in which 76% is held by M/s Rama Ratna Wires. Epack plans to enhance the holding to 50% soon. The company manufactures BLDC motors for AC, Fans etc. This unit also has PLI support.

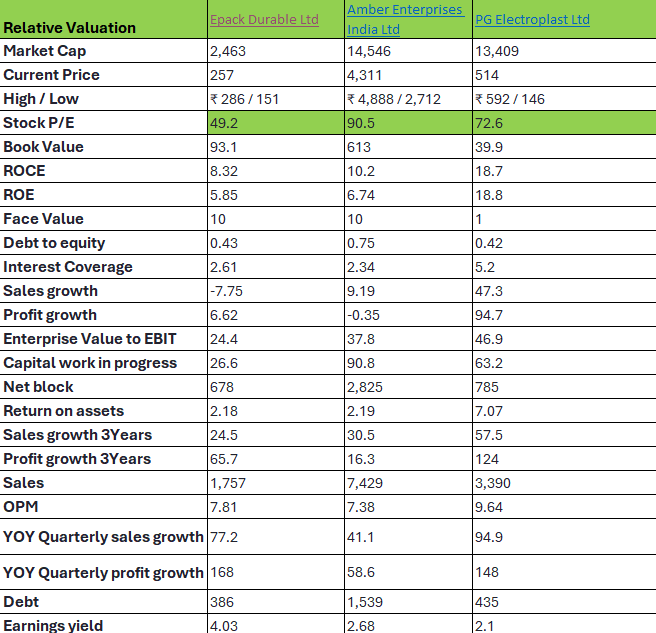

On a relative basis Epack looks cheap compared to peers Amber and PG electroplast.

Based on the management guidance of 45% growth and 100 Bps improvement in margins ;

(Cooling of raw material prices , Sri City plant getting fully operational , Last 2 qtr trends )

FY 25 revenue = 2100 cr.

PAT = 63 Cr

@ 50 PE (current P/E : Industry peers at 75+) market cap= Rs 3150 Cr.

Current Market Cap = 2475 Cr

Potential Upside = 27%

Risks and Threats to the business

-

Several OEMs have started their own manufacturing facilities due to import restrictions and PLI benefits. Since Fy 24 AC sales soared due to Heat wave conditions the impact was not fully understood. Once the OEM facilities come on steam fully only the impact will be understood.

-

Epack is diversifying into Washing Machines and other Large domestic Appliances. How they manage this transition is to be seen.

-

RAC business is seasonal in nature with Q2 and Q3 typically muted in nature. This can lead to short term pain and price erosion.

-

The company has c. 350 Cr debt. Even though the interest coverage is comfortable and company has done most of the capex already this can be a deterrent if the cycle turns .

Conclusion

E-pack durables is available at almost the listing price, it has several industry tailwinds going for it and looks to be cheap relative to peers. The company adding new product lines and additional capacity can add to future top line growth. The company has good amount of back ward integration , with the govt push for components (via PLI and import duties) will also aid the growth.

Disc : Invested a tracking quantity . Might add or reduce without prior intimation. Pls do your due diligence

Sources : Company Presentation, AR, Concall transcripts

Forensics and the art of triangulation (27-08-2024)

(post deleted by author)

SmallCap Hunter : Trying to find the dark horses with triggers (27-08-2024)

There is a company named Filtra consultants…involved in the trading business of such water related products

Tasty Bites: A proxy play to India’s QSR industry (27-08-2024)

The video link is fails to open, how is this enabled for you? I tried from different browsers but had no luck.

My 0.001% stock market journey (27-08-2024)

My Top 3 holding in each basket.

Long-term

Polycab

KPR Mill

Titan

Stock SIP

PROTEAN

IREDA

JIO

Passive income

ONGC

Engineers India

RAJOO Eng.

Disclaimer: I am not a SEBI registered or a financial advisor. Any of my investment or trades I share on this post are provided for educational purposes only and do not constitute specific financial, trading or investment advice.

Balrampur Chini Mills – A Sweeter Aftertaste? (27-08-2024)

Balrampur Chini is completely changing now, With the new Polylactic acid capex announcement the business is et to become structural and re-rate going forward.

HBL Power: Signs of change (27-08-2024)

There are 8 new Kavach tenders which have been floated in last week. Other than some specific routes they have come up with Kavach for Mumbai Howrah section. Not attaching any docs as they are all available on ireps, just putting a summary here:

| Section | KM (approx) |

|---|---|

| Nalwar – Guntakal – Yerraguntla – Renigunta | 500 |

| BHUTESHWAR (INCL) – DHOLPUR | 400 |

| Bina- Itarsi- Jujharpur | 230 |

| MAS-GDR, MAS-AJJ, AJJ-RU | 271 |

| Nalwar – Guntakal – Yerraguntla – Renigunta | 650 |

| Dholpur – Bina | 320 |

| Duvvada-Vijaywada | 350 |

| Nagpur Station Kavach Equipment | |

| Solapur – Sainthia (Howrah) | |

| Bhusaval – Sainthia (Howrah) | |

| Pune- Sainthia (Howrah) | |

| BB (Mumbai)-Sainthia (Howrah) | |

| Viramgam- Rajkot-Okha | 434 |

| AHMEDABAD-PALANPUR SECTION AND AHMEDABAD- SAMAKHIYALI | 402 |

| GD & GQ routes (Kolkata Division) | 688 |

Along with the above is a 10000 locos tender.