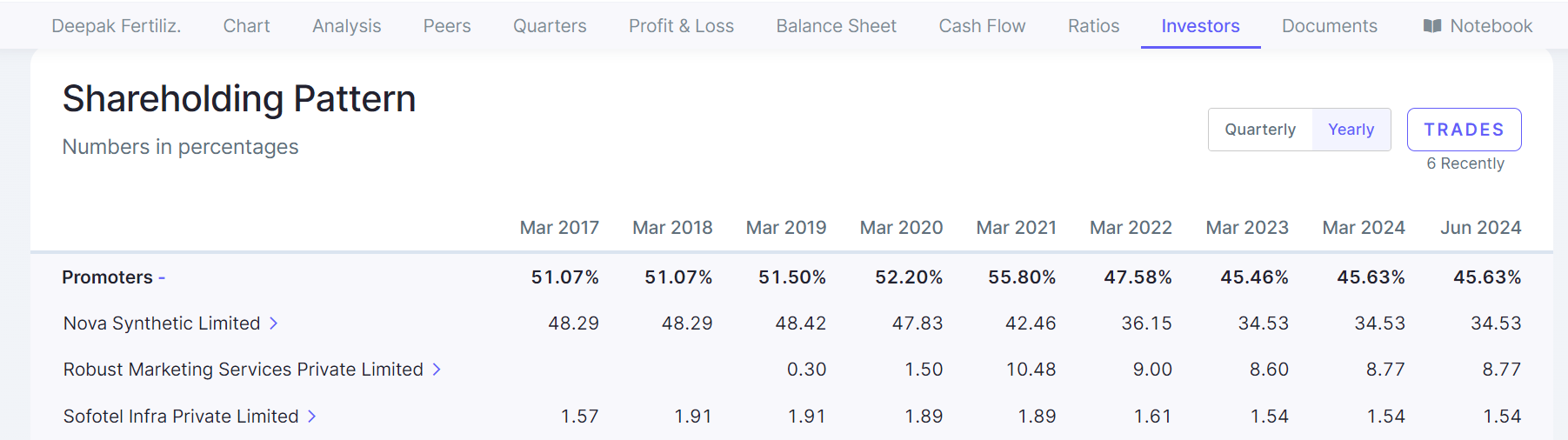

The shareholding that you’ve shared is not of the CEO but of private holding companies.

The shareholding that you’ve shared is not of the CEO but of private holding companies.

I dont see CWIP in the financial statements to substantiate such a growth ? What am i missing ?

nice work, can you keep it in google sheet and share link? instead of downloading we can just browse with read access and easily shareable across ?

I have tried to summarize key points based on what I have seen in the hospital sector. These are broad points which includes some softer aspect to give insights(posting the same from Narayan hospital thread)

1.First established multispecialty hospital in a city will have significant moat in attracting patients. Main reason being the trust of that particular hospital gained over decades of service and is difficult for the new competitor to replace it. Many patients and relatives keep coming to the particular hospital because someone known to them was treated and recovered in that hospital even if it’s more than a decade back. This happens despite the same specialty being available in some other hospital near to them which was not existent earlier. Even for the same level of service and specialty doctor the existing one is preferred even at slightly higher cost. The feeling that someone known to them recovered in a particular hospital and trust has an ever lasting impact on people and probably the greatest moat.

Longer the hospital is functioning, the better will be its revenue and margins as they can keep on expanding their capabilities like , oncology, higher radiology services, specific surgical capabilties like organ transplants, robotic surgeries etc. As the hospital expands these superspeciality services, the revenue per patients and margins improve with limited additional investment.

Mix of patients in terms of paying: Best is to have a private insurance patients pool as the money is guaranteed on time and there are standard payment terms with the insured. Also standard hospital rates are defined and the patient knows what will be their share in paying. Hospital charges are highest for cash patients but the problem is at least 5% of cash patients do not pay the full amount and the hospital has to let go a reasonable amount for such cases under various circumstances like death/influential calls from local leaders/politicians.

Mix of surgical vs medical patients. In general higher the number of surgical mix better the profitability of hospitals. As cost of operation and associated charges like OT charges, radiology imaging before surgery etc… are much higher per bed compared to patients undergoing only medical treatment. If the occupancy of such a hospital improves the operating leverage is significantly higher as fixed cost of operation theater/pre and post op care is better absorbed.

Typically hospitals agree for most of the Govt schemes like ECHS,CGHS etc in the beginning as it helps them to cover certain basic costs. It also helps to gain good will among patients over the years as the family members/friends of such scheme patients will start availing the particular hospital services and increasing occupancy. Govt schemes come with their own risk of increasing receivables, significantly less consultation fee/operation fee impacting margins. As occupancy of a particular hospital reaches around 70%, typically hospitals will start to withdraw from Govt schemes. This helps in freeing up sufficient beds for other patients and increases average revenue per patient. The consultation fee and other charges for a private patient is 10-20 times higher compared to Govt schemes. This may lead to some drop in occupancy for particular hospitals in the short term but the ARPOB are much much higher for a pvt patient compared to Govt scheme. It also helps in reducing receivables, reduction in manpower employed in Govt insurance desk, lesser requirement of healthcare workers as overall no of patients comes down but with much better profitability.

Hospital with optimum ALOS. In general the maximum billing for any patient happens during the first few days of hospital admission. Initial evaluation including lab tests, radiology investigations and critical therapeutic intervention happens during the first 1-4 days. After that it’s generally the ongoing maintenance therapy of the initial plan and revenue per patient per day drops after 3-4 days. It’s better to look for hospitals with ALOS of 3-4 days. It also indicates how efficient the hospital system is in terms of quick admission, evaluation, treatment and discharge process and dealing with insurance companies for quick discharge. Reducing ALOS less than 3 days in multispecialty hospitals is practically impossible as the number of sicker patients, superspeciality, and complex surgical treatment increases.

Presence of long serving doctors who can get more patients to hospitals on their own. Impact of it is more in particular surgeons/gynecologists. Obviously patients do prefer to go under knife with the same surgeon who has done it successfully in the past for them or relatives.

One of the key things to look at is retention of consultants by hospitals. If the same consultant remains to work with the same hospital for a longer time of more than 5/10yrs it brings a lot of repeat patients. The time and efforts required spent in evaluating known patients with readily available past history is lesser than a new case. Probably this is one of the key but ignored question to ask in company concalls.

Presence of DrNB educational program in hospital.It makes the particular medical fraternity of the hospital to be updated about ongoing changes in the medical field and improve the care of patients. It also gives the hospital administration adequate junior level doctors to work during their training period. Generally if some of the junior doctors are good during their training period will be absorbed into the unit as they complete the degree.

International patient mix; Higher mix of international patients bring higher revenue and better profitability. Generally international patients come to India for superspeciality care like Oncosurgery, Organ transplantation etc… The cost of the same is higher by ~25% compared to domestic patients helping in better revenue and margins for hospitals.

Discl: currently not invested in hospital stocks.

What is the reason for lack of faith in management… corp governance issues? company is doing well financially.

I have tried to summarize key points based on what I have seen in the hospital sector. These are broad points which includes some softer aspect to give insights:

1.First established multispecialty hospital in a city will have significant moat in attracting patients. Main reason being the trust of that particular hospital gained over decades of service and is difficult for the new competitor to replace it. Many patients and relatives keep coming to the particular hospital because someone known to them was treated and recovered in that hospital even if it’s more than a decade back. This happens despite the same specialty being available in some other hospital near to them which was not existent earlier. Even for the same level of service and specialty doctor the existing one is preferred even at slightly higher cost. The feeling that someone known to them recovered in a particular hospital and trust has an ever lasting impact on people and probably the greatest moat.

Longer the hospital is functioning, the better will be its revenue and margins as they can keep on expanding their capabilities like , oncology, higher radiology services, specific surgical capabilties like organ transplants, robotic surgeries etc. As the hospital expands these superspeciality services, the revenue per patients and margins improve with limited additional investment.

Mix of patients in terms of paying: Best is to have a private insurance patients pool as the money is guaranteed on time and there are standard payment terms with the insured. Also standard hospital rates are defined and the patient knows what will be their share in paying. Hospital charges are highest for cash patients but the problem is at least 5% of cash patients do not pay the full amount and the hospital has to let go a reasonable amount for such cases under various circumstances like death/influential calls from local leaders/politicians.

Mix of surgical vs medical patients. In general higher the number of surgical mix better the profitability of hospitals. As cost of operation and associated charges like OT charges, radiology imaging before surgery etc… are much higher per bed compared to patients undergoing only medical treatment. If the occupancy of such a hospital improves the operating leverage is significantly higher as fixed cost of operation theater/pre and post op care is better absorbed.

Typically hospitals agree for most of the Govt schemes like ECHS,CGHS etc in the beginning as it helps them to cover certain basic costs. It also helps to gain good will among patients over the years as the family members/friends of such scheme patients will start availing the particular hospital services and increasing occupancy. Govt schemes come with their own risk of increasing receivables, significantly less consultation fee/operation fee impacting margins. As occupancy of a particular hospital reaches around 70%, typically hospitals will start to withdraw from Govt schemes. This helps in freeing up sufficient beds for other patients and increases average revenue per patient. The consultation fee and other charges for a private patient is 10-20 times higher compared to Govt schemes. This may lead to some drop in occupancy for particular hospitals in the short term but the ARPOB are much much higher for a pvt patient compared to Govt scheme. It also helps in reducing receivables, reduction in manpower employed in Govt insurance desk, lesser requirement of healthcare workers as overall no of patients comes down but with much better profitability.

Hospital with optimum ALOS. In general the maximum billing for any patient happens during the first few days of hospital admission. Initial evaluation including lab tests, radiology investigations and critical therapeutic intervention happens during the first 1-4 days. After that it’s generally the ongoing maintenance therapy of the initial plan and revenue per patient per day drops after 3-4 days. It’s better to look for hospitals with ALOS of 3-4 days. It also indicates how efficient the hospital system is in terms of quick admission, evaluation, treatment and discharge process and dealing with insurance companies for quick discharge. Reducing ALOS less than 3 days in multispecialty hospitals is practically impossible as the number of sicker patients, superspeciality, and complex surgical treatment increases.

Presence of long serving doctors who can get more patients to hospitals on their own. Impact of it is more in particular surgeons/gynecologists. Obviously patients do prefer to go under knife with the same surgeon who has done it successfully in the past for them or relatives.

One of the key things to look at is retention of consultants by hospitals. If the same consultant remains to work with the same hospital for a longer time of more than 5/10yrs it brings a lot of repeat patients. The time and efforts required spent in evaluating known patients with readily available past history is lesser than a new case. Probably this is one of the key but ignored question to ask in company concalls.

Presence of DrNB educational program in hospital.It makes the particular medical fraternity of the hospital to be updated about ongoing changes in the medical field and improve the care of patients. It also gives the hospital administration adequate junior level doctors to work during their training period. Generally if some of the junior doctors are good during their training period will be absorbed into the unit as they complete the degree.

International patient mix; Higher mix of international patients bring higher revenue and better profitability. Generally international patients come to India for superspeciality care like Oncosurgery, Organ transplantation etc… The cost of the same is higher by ~25% compared to domestic patients helping in better revenue and margins for hospitals.

Disc: currently not invested in hospital stocks.

In the recent Q1 call, there are certain red flags. Please see below from the recent transcript. There are serious mistakes pointed out by analysts in the presentation. There is lot of confusion on order book and Bid book. I think this business seems risky as 80% of the order book is from Saudi Arabia and looking at current political situation in middle east, I find this business quite risky.

Transcript portions

Dhavan Shah: Sir, this is Dhavan Shah from Alfacurate Advisors. So, my question is on the projected capacity

by FY26. So, in this presentation, I think we have shown that by FY26, we will be having

2,25,000 capacity of ERW versus the last quarter presentation it was showing roughly 2,75,000

tons, so why there is a reduction of roughly 50,000 tons in ERW?

Nikhil Mansukhani: 5,000 tons in ERW?

Dhavan Shah: This quarter presentation is showing 2,25,000 tons of ERW capacity by FY26 and in the last

quarter presentation, it was showing roughly 2,75,000 tons?

Nikhil Mansukhani: So, Dhavan, there might be some clerical error. We will get back to you on that

Pradeep Rawat: Sir, my first question is regarding our ERW CAPEX, so we are planning to expand 100,000 tons

per annum capacity for ERW. So, what would be the CAPEX for this expansion and when could

we assume this plant to be commissioned?

Nikhil Mansukhani: The ERW CAPEX, Pradeep has already been completed and it is under operation.

Pradeep Rawat: So, I am talking about the expansion that we have shown in our presentation. So, currently, we

have a capacity of 1,75,000 tons per annum and we are expecting this capacity to be 2,75,000.

So, I was just asking for that additional capacity?

Nikhil Mansukhani: Pradeep, we will get back to you that. I think there has been some clerical error on that. So, we

will get back to you on that like we said in the first thing, we will get back on that particular

thing.

Dhavan Shah: And when this Saudi Arabia plant would commission?

Nikhil Mansukhani: 12 months.

Dhavan Shah: So, it would be in FY26 only?

Nikhil Mansukhani: Yes.

Dhavan Shah: And so I think in the presentation, we have to update that thing also, right?

Nikhil Mansukhani: Correct. We will send the updated one.

Darshil Pandya: So, just one question from my end, regarding the 10% EBITDA margin guidance that you have

given. So, if we could know that is it because of the order book that we have right now has a

higher margin or how will we achieve that margin in this full year?

Nikhil Mansukhani: The order book which we have now is on the exports are more on the higher margins. So, we

are confident to achieve the yearly guidance which we are giving.

After reading the Q1 Transcript, My confidence level is low and I am thinking of booking profits to be on safer side. Views of more knowledgeable members are requested on my assessment.

Disclosure- I bought at 138-140 level, I am not a SEBI registered advisor and my views are biased and are based on my little understanding of the business. Please make your own assessment for any decision you take.

Q1Fy25 PPT of GPIL

Adding two cents to this, it seemed that in this particular call, a lot of undertones were there pointing towards that perhaps Rupesh sir is looking beyond 20-25% growth which is a given now as his guidance. Some of the indicators:

The ever expanding order book, the expansion of the dealer model for base machines.

The JV being an attempt to grow further with the current growth a given even without JV

The aggressive hiring of the sales team.

The closing note that don’t exit basis Q1 results in this industry.

**I feel the promotor pedigree is unmatched here and his operational skills are par excellence **

Personally for me highest allocation in portfolio and hence can be biased

For that will need to see subsidiary’s annual reports on the company’s website