Except for the first point, rest is already know to market. Still not able to understand why the price is still down. Also, if market falls, won’t there by risk of further downside?

Posts in category Value Pickr

The harsh portfolio! (24-08-2024)

- Amara Raja – mostly the earnings and thesis will slowly play out as they unfold the new 2.0 Amara energy thingy they decided upon this year. Warrants a re look as the stock px moved fast. Personally, i am also on the sidelines after being in the grind since 450. Technically i would have still held to it if other options were not available in the watchlist.

- Hdfc AMC should still do well. And i don’t have any good reasons for someone to exit other than opportunity cost. Absl Amc Hdfc Amc these 2 are my watchlists for sometime now.

Premier Roadlines Ltd (24-08-2024)

Company Overview:

- Premier Roadlines Ltd (PRL) is established in 2008 and PRL is an IBA approved & ISO Certified surface logistics service provider of dry cargo ranging from 1MT to 250 MT.

- Services rendered through third-party operators with Trucks, Trailers, Hydraulic Axles, etc.

- Well established PAN India network, along with growing presence in Nepal and Bhutan.

- Market cap is 314 crores as on 24-Aug-2024.

Operational Updates:

- PRL is headquartered in Delhi and has 28 branches in Ahmedabad, Bengaluru, Chennai, Guwahati, Hyderabad, Kolkata, Mumbai, Nashik, Pune, etc. On December 31, 2023, company had 204 permanent full-time employees.

- PRL collaborates with third-party providers, including small fleet owners and agents, who supply transportation equipment such as container trucks, trailers, hydraulic axles, etc., for their transportation services.

- PRL had not owned any fleet till last year. They have bought two pullers Eicher 8055 models(18 axles) and eight low-bed trailers recently.

- Company provides four services, which are project logistics, over-dimensional, overweight, contracted integrated logistics and general logistics.

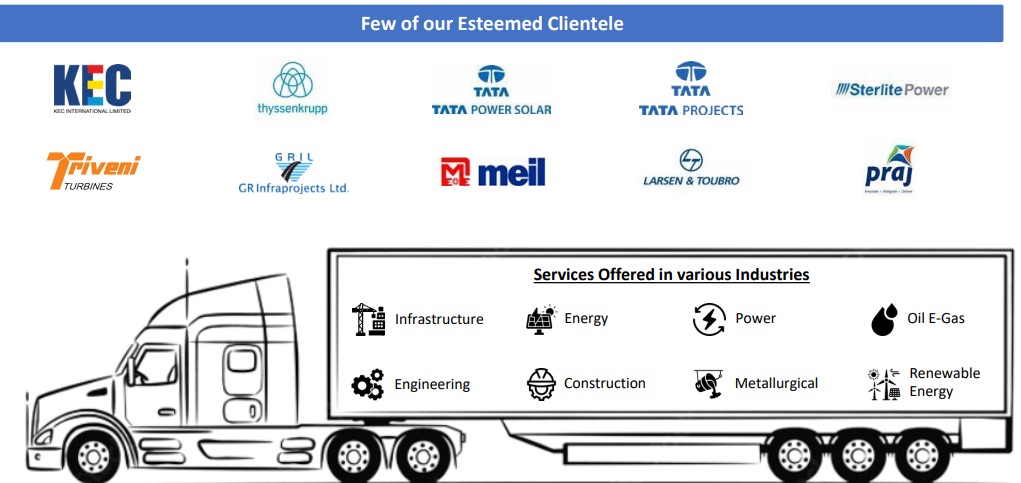

Clients:

The company serves clients across various sectors including infrastructure, energy, electricity, oil and gas, mechanical engineering, construction, metallurgy, renewable energies, etc. Some notable clients include KEC International Limited, ThyssenKrupp Industrial Solutions (India) Private Limited, Tata Project Limited, G R Infraprojects Ltd, Tata Power Solar Systems Limited, Sterlite Power Transmission Limited, etc.

Financial Highlights (FY 2024):

- The company achieved total income of Rs 229 Crores, marking a 19% year-over-year increase, with an EBITDA of Rs 21 Crores (a 61% YoY increase) and a profit after tax of Rs 13 Crores (a 75% YoY increase).

- Margins expansion of 250 bps YOY to 9.3% due to focus on higher-margin project logistics and over-dimensional cargo services.

- Last three-years CAGR for revenue is at 34% and PAT is at 101%.

- ROE is 38% and ROCE is 27% in FY 2024

Future Outlook:

- Revenue target is 30% annually for FY25 and FY26 .

- Planning to purchase own vehicles to increase goods transportation network.

- Extending services to additional industrial sectors along with expanding customer base in existing industrial sectors.

- Company is also planning to expand its tech activities to further streamline large scale activities.

Industry Overview and Tailwind:

- The Indian logistics sector, valued at USD $354 billion and contributing 18.4% to GDP, is set to reach $450 billion by 2026-2027, driven by easing FDI norms, GST implementation, globalization, e-commerce growth, and government initiatives like “Sagarmala,” “Make in India,” and “Gati Shakti.” Despite a World Bank ranking of 38th in 2023-2024, the industry’s logistics cost is dominated by the unorganized sector, which accounts for 99% of the USD $150 billion total. Reducing logistics costs from 14% to 9% of GDP could save USD $50 billion, enhancing global competitiveness and potentially boosting exports and job creation.

- India’s rapidly growing economy and infrastructure development have led to a significant increase in the demand for project logistics services, particularly for the transportation of overweight and oversized cargo as the country embarks on ambitious projects in sectors such as construction, energy, and manufacturing, the logistics industry faces the challenge of safely and efficiently moving heavy and bulky cargo across the country’s vast and diverse terrain.

Risks

- The performance of companies in the transportation industry is highly sensitive to fluctuations in company earnings and the price of transportation services. Main factors affecting company earnings include fuel costs, labor costs, demand for services, geopolitical events and government regulation.

- Oil prices are a key factor for transportation, as the commodity’s price generally has an influence on transportation expenses. Gas and fuel prices that rise will increase costs for a trucking company, eating into their profit.

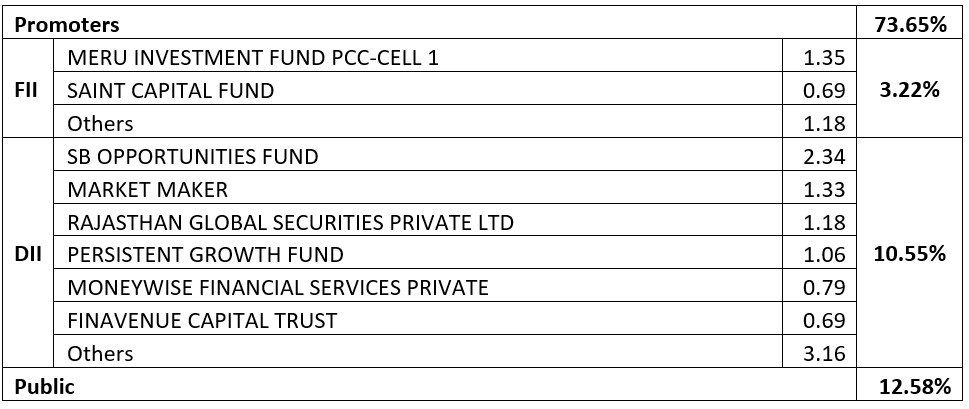

Share Holding as on 16-May- 2024

Disc: invested

Commodity and Cyclical Plays (24-08-2024)

Rain Industries: A Potential Turnaround play, might have bottomed out, reversal looks like from the next few months.

Positives and Key Considerations for Rain Industries:

- Raw Material Availability: Rain Carbon recently received approval for a higher allocation of Graphitized Petroleum Coke (GPC), a critical raw material for their Vizag and SEZ plants. This development comes after a long period of restriction and should enable the SEZ plant to operate at full capacity within 6 to 12 months. This increased capacity could significantly boost revenue and profitability, thanks to enhanced operating leverage.

- Debt Management: Although Rain Carbon’s debt is high and interest rates are elevated, the company historically took on loans at low interest rates for expansion projects. Their Return on Equity (ROE) was previously higher than the interest rates on the debt, making this a reasonable strategy. With most of the capital expenditure completed and plants coming online soon, the company is positioned to start reducing debt more aggressively as no major capex has been planned in near term. Also interest savings flow through to the bottom line, this could lead to a re-rating of the company’s stock. This can change the perception of investors looking towards this business.

- Aluminum Market Outlook: The demand for aluminum is expected to rise due to trends such as the shift toward electric vehicles, automotive and aerospace light-weighting, and the expansion of renewable energy infrastructure. Global aluminum production is projected to grow, surpassing previous highs over the next few years.

- Cost Efficiency: Rain Carbon is among the world’s lowest-cost producers of GPC and CPC Though they don’t beat their chest and say, their cost advantage is reflected in their operating margins, even during downturns, positioning them favorably compared to competitors.

Optionality and Strategic Moves:

- Anhydrous Carbon Pellets (ACP): Since 2011, Rain Carbon has been developing ACP to mitigate risks associated with the availability and quality of GPC. This patented product could provide a significant competitive moat by safeguarding margins against raw material price fluctuations.

- Shift to Value-Added Products: The company is transitioning towards value-added products in advanced carbon materials, which should stabilize margins and reduce cyclicality compared to their traditional products.

- Focus on Energy Storage Materials: Rain Carbon is making strides in the energy storage sector with the establishment of a new R&D facility in Hamilton, Ontario. This center will support the development of energy storage materials for lithium-ion batteries, solid-state batteries, sodium-ion batteries, and hydrogen fuel cells. The R&D efforts are expected to drive innovation and strengthen their position in the energy storage market.

Given Rain Carbon’s strong cash flow, low valuations, potential for debt repayment, Operating Leverage, recovering carbon product demand, and other strategic initiatives (Optionality Playing out), it appears that many of the negative factors have been addressed. Any positive developments could lead to a significant re-rating of the company’s stock, which is currently undervalued and overlooked.

DISC: Invested (Can be Biased)

Commodity and Cyclical Plays (24-08-2024)

China exporting copper to the US !

Copper price squeeze upends global trade flows – The Economic Times (indiatimes.com)

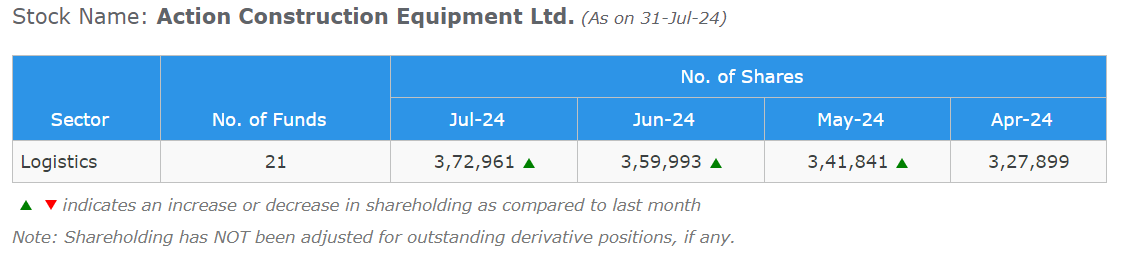

Action construction equipment ltd (24-08-2024)

Maybe not buying like crazy but there’s definite DII interest. Also FIIs have been increasing so net-net there is institutional interest.

B C C Fuba India Ltd: PCB Manufacturing Nanocap (24-08-2024)

You are right there are simple PCBs like two layers and then there are multi layer impedance controlled PCBs. Another complexity is the size of pitch(ball to ball distance) that needs to be imprint to solder complex semiconductor chips. There are various kinds of materials used in different kind of PCBs, that requires material knowledge. PCB manufacturing is also understanding, a bit of chemistry. In recent budget we saw some duty on PCBs imported that shall provide some tailwind. This would take off when component manufacturing takes off Vs assembly we are mostly doing in India.

Disclosure: Invested from much lower levels.

Action construction equipment ltd (24-08-2024)

HI Ashwind,

in the recent concall, promoter said their stake sell was for a marqee investor but is there any name visible in the shareholding.

also domestic institutions are not showing any interest inspite of some fabulous 6 years of growth and above average guidance from the management for next 5 years.

How do you look at this?

thanks

My 0.001% stock market journey (24-08-2024)

You dont have to be SEBI registered to share your portfolio \s here. You are not recomending anything to buy or sell, just sharing your portfolio. Just add that disclaimer, you will be just fine.

Delton Cables – Undervalued High growth stock? (24-08-2024)

last one year I am holding this scrip.Give me multi bagger return in my portfolio.5 times