Pls correct if my understand is wrong:

If we go for conversion; the holding period of the shares will start afresh i.e 1st Sept, irrespective of when you bought the DVR. so for someone looking to sell within the next 1 year, better to sell DVR now and pay only LTCG

However since the cost price shall also be determined as the closing price of Tata Motors on 30th August, better to go for the conversion and bring down the profit and hence tax…

Posts in category Value Pickr

Tata Motors – DVR (24-08-2024)

Ranvir’s Portfolio (24-08-2024)

Innova Captab –

Q2 FY 25 concall and results highlights –

Revenues – 294 vs 233 cr

EBITDA – 44 vs 32 cr, up 36 pc ( margins @ 16 vs 14 pc )

PAT – 29 vs 17 cr, up 67 pc

Breakup of sales in Q1 FY 25 vs Q1 FY 24 –

CMO – 57 vs 71 pc

Domestic branded sales – 17 vs 18 pc

International branded sales – 11 vs 11 pc

Sharon Bio’s sales – 15 pc vs NIL

14 out of top 15 domestic Pharma companies are company’s clients

Company’s manufacturing units –

02 @ Baddi – can make – tablets, capsules, ointments, syrups, dry powder injections, liquid orals. Capacity utilisation @ 50 pc

01 @ Dehradun – tablets, capsules

01 @ Taloja – APIs

Both Dehradun and Taloja units are acquired units of Sharon Bio. Capacity utilisation at both these units is around 60 pc

New Greenfield unit coming up at Jammu – Multiple products. Likely to go live in Q2 FY 25. Full capacities to ramp up over a period of 2-3 yrs. Its a formulations plant mainly focussed on – Cephalosporins, Penicillin, Carbapenems product families. To make dosage forms like – tablets, capsules, dry powder injectables, dry syrup and respiratory respuels

Jammu facility has a peak revenue potential of > 1500 cr / yr. Likely to be achieved within 5 yrs. Expect to do > 300 cr sales from this plant in FY 26. Should be able to ramp up sales to 900 cr from this plant by FY 28

Company has 01 R&D center at Baddi. Setting up another one @ Panchkula

API prices continue to be soft – both for acute and chronic APIs. At present, company is procuring 70-80 pc of its API requirements from domestic sources. As PLI schemes for the API sector show full effects, company’s domestic sourcing may even go higher going fwd

Company’s margins in domestic + international branded business are > CMO business. However, company has no plans to dramatically change its business mix. They aim to keep growing all their businesses at healthy rates

As the Jammu plant ramps up, company expects to double its revenues and profits in next 3 yrs

Company’s domestic branded formulations are sold under the brand umbrella – ” Univentis Medicare “

As the GoI keeps imposing / being strict on implementation of GMP guidelines iro various Pharma manufacturing units, the organised + compliant players stand to benefit. Its a natural tailwind for the company

In FY 26, if Jammu plant clocks 300 cr sales and company’s base business grows by early teens ( say 13 – 15 pc )- as guided by the management, the total business may grow by > 35 pc !!!

For FY 25, growth should be > 15 pc with similar margins as last FY

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation

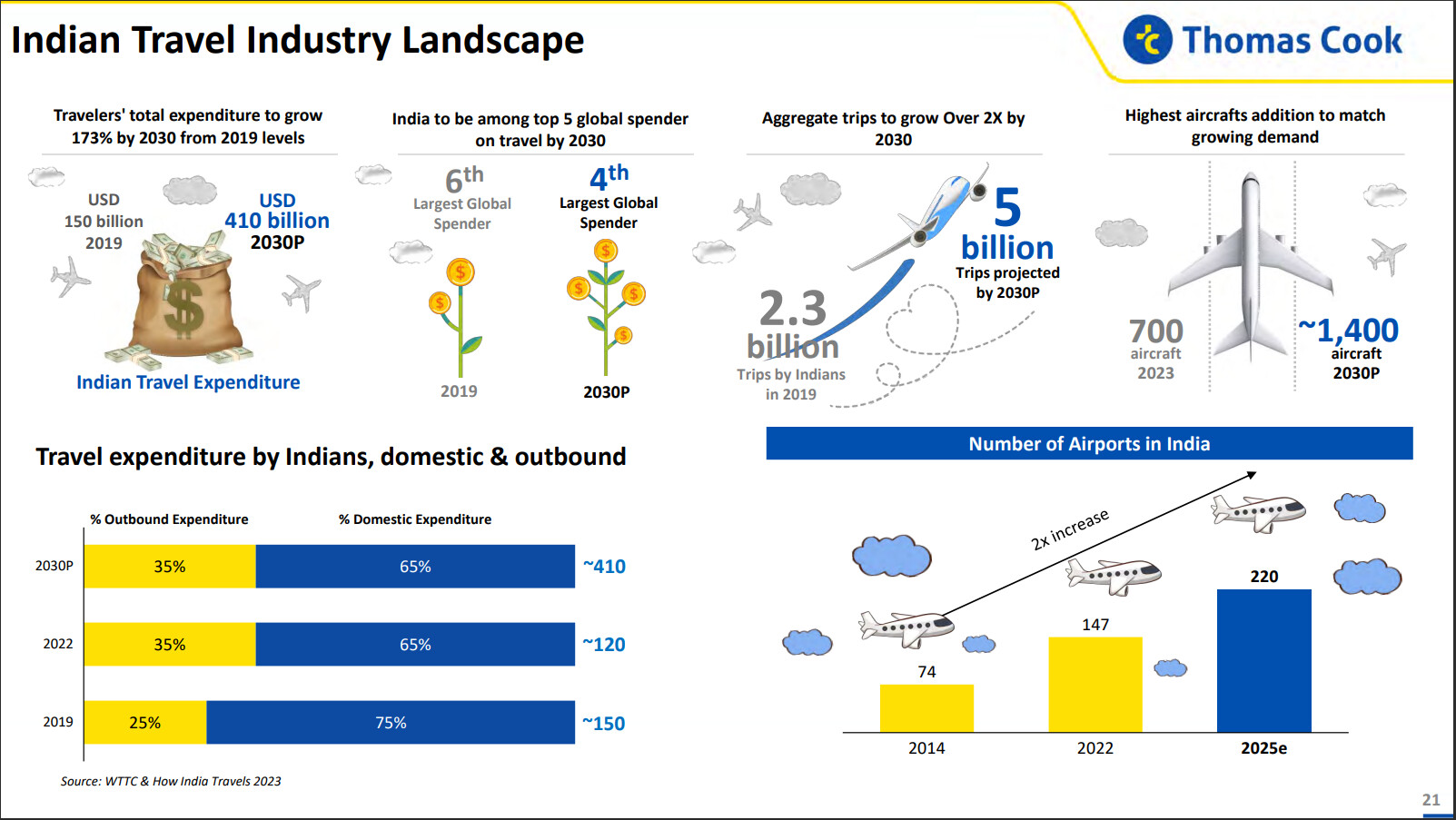

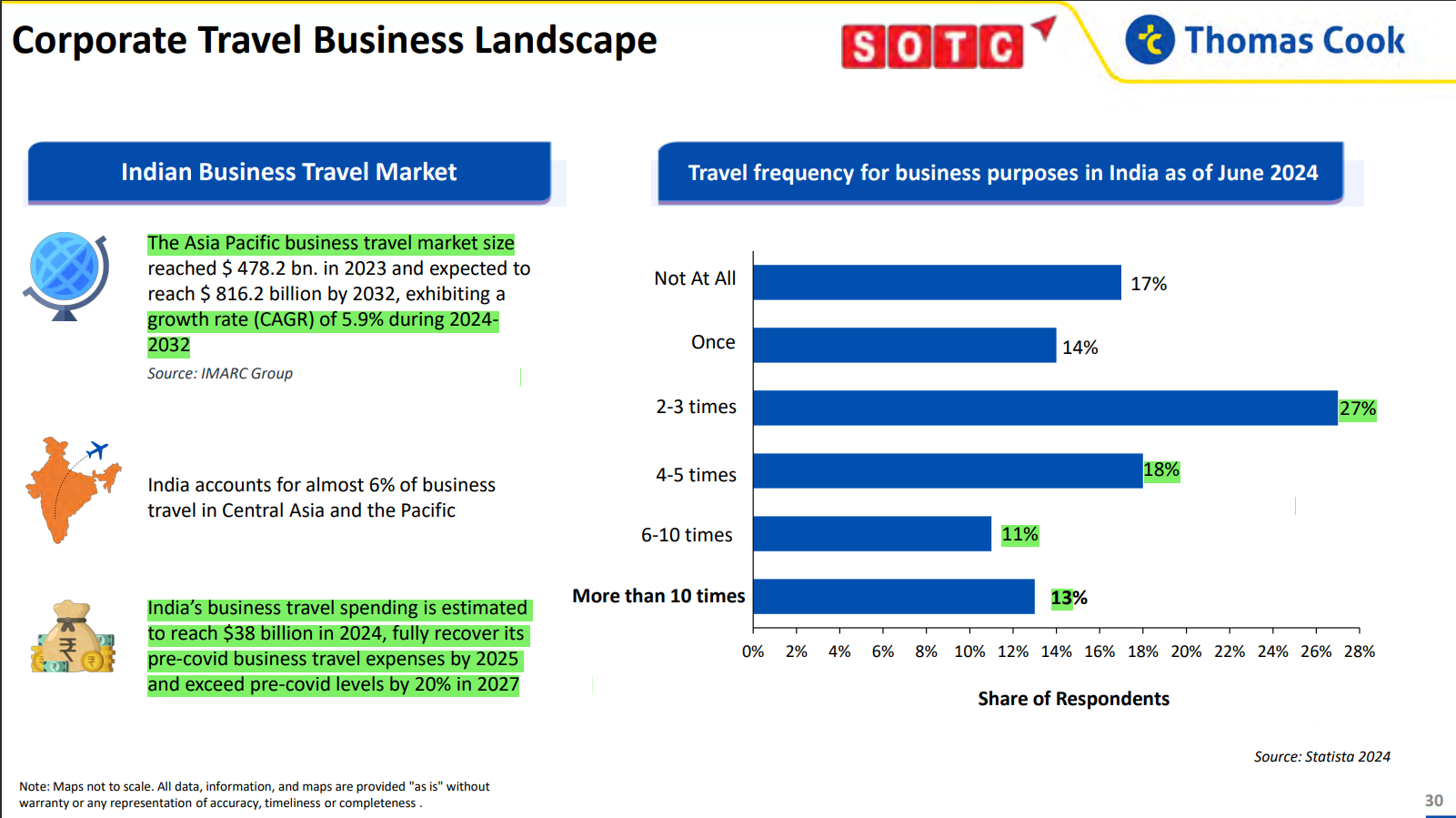

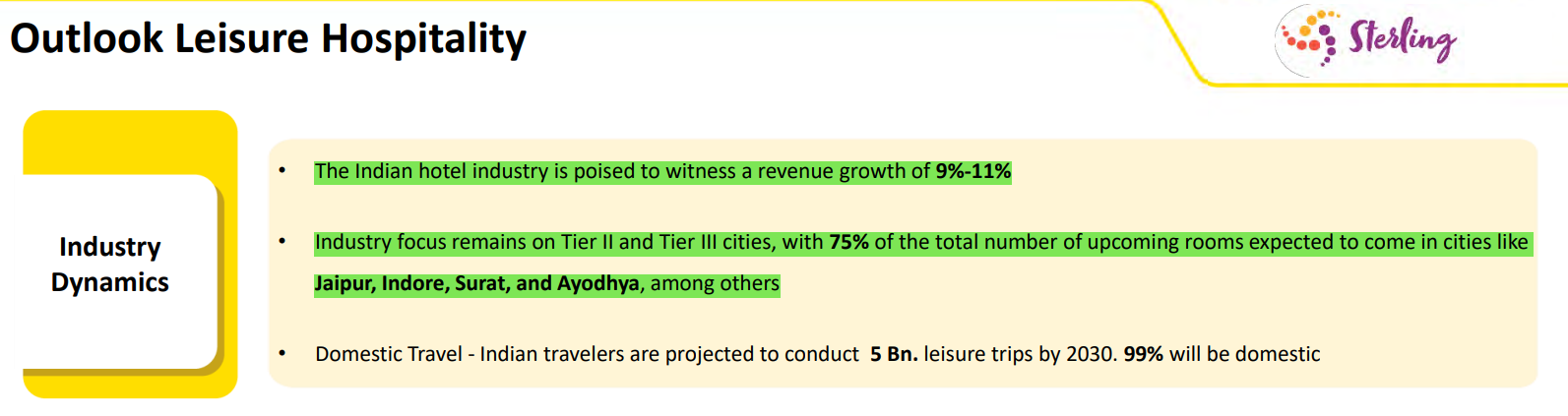

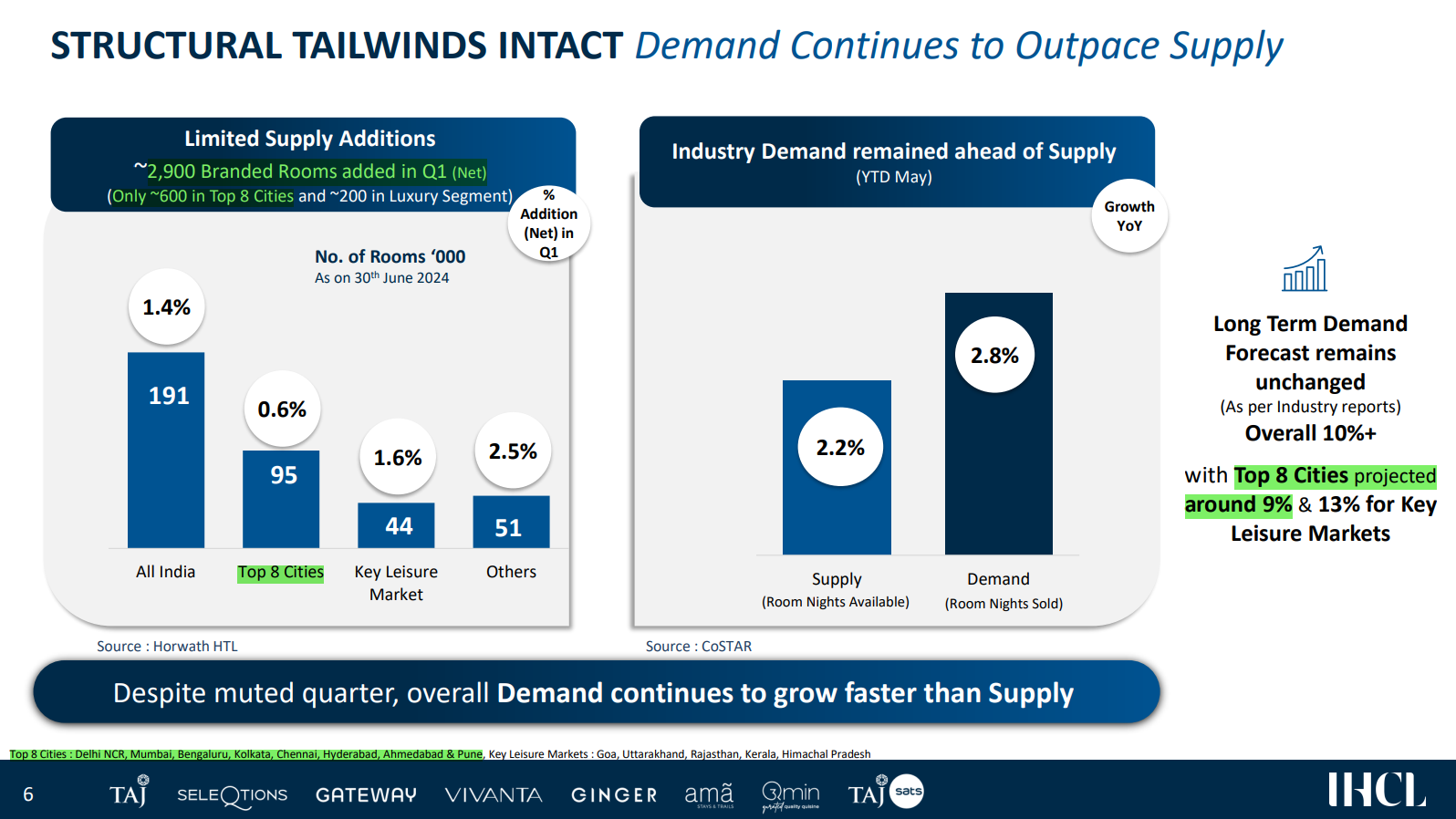

Samhi Hotels – Turnaround with Tailwinds (24-08-2024)

India’s business travel spending is estimated to fully recover its pre-covid by 2025 & exceed pre-covid levels by 20% in 2027 with ~70% respondent saying they would travel at least 2-3 times for business.

In the Hotel Industry 75% of room addition is coming up in Tier II & III cities, means only 25% room addition in Tier I metro cities.

As per IHCL, out of 2900 branded keys added in Q1 only ~20% were added in Top 8 cities (i.e. Delhi, Mumbai, Bangalore, Kolkata, Hyderabad, Pune, Chennai, Ahmedabad). Also, while Demand is projected to grow at around 9% in top 8 cities, supply is lagging at 0.6% net addition in Q1.

Src: Thomas Cook PPT, Aug 2024 & IHCL PPT July 2024

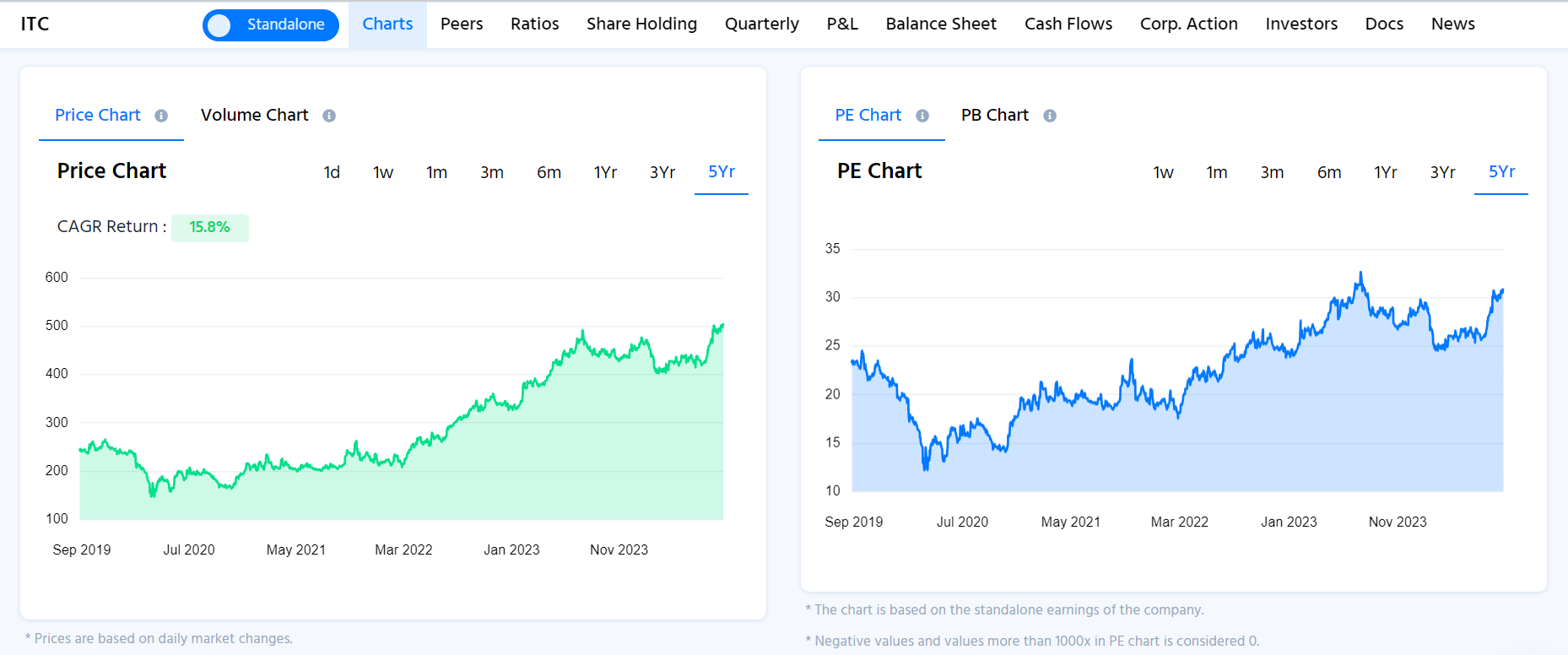

ITC: “Will”(s) “Gold Flake” assist “Ashirwad” to win “Bingo!”? (24-08-2024)

The Valuation of ITC is at its peak.

As we can see from the below image, the PE is reaching the top it made in 2023.

(Image source: Finology Ticker)

It is correlated with the price too.

The company gave 15.8% CAGR returns in the past 5 years.

Going forward, some of its Strengths are

-

Market Leader: ITC boasts dominant market positions in cigarettes (Gold Flake, Classic), branded atta (Aashirvaad), biscuits (Sunfeast), snacks (Bingo!), and stationery (Classmate). This diverse portfolio provides stability and resilience during economic downturns.

-

Integrated Model: The company’s leadership in paperboards, paper, and packaging supports its FMCG ventures, creating a strong operational synergy.

-

Defensive Stock: As evident from the provided chart, ITC’s stock price has exhibited relatively stable growth, even during the 2020 market crash. This stability makes it an attractive option for investors seeking defensive plays in the FMCG sector.

-

Brand Power: ITC’s extensive brand portfolio, including household names like Aashirvaad and Sunfeast, fosters strong brand loyalty and consistent revenue streams.

-

Index Inclusion: The company’s presence in 39 indices signifies its significant market impact and potential for passive investment exposure.

Recent Performance:

While ITC’s Q1FY25 results showed a slight dip in net profit, its total income experienced marginal growth. It’s crucial to monitor future quarters to assess the sustainability of this trend.

Investment Thesis:

ITC presents itself as a compelling investment opportunity due to Stable growth, Diversification, Brand Power & potential for growth.

However, some factors require consideration:

-

Slowdown in Cigarette Sales: The rising awareness of health concerns might lead to a gradual decline in cigarette sales, impacting a significant portion of ITC’s revenue.

-

Regulatory Risks: The government’s policies regarding tobacco and FMCG products can affect ITC’s profitability.

Overall, ITC remains a solid long-term investment option for those seeking stability and potential for moderate growth. However, conducting further research and staying updated on the company’s performance and industry trends is crucial before making any investment decisions.

Let’s discuss!

- What are your thoughts on ITC’s future prospects?

- Are there any other factors we should consider before investing in ITC?

- How does ITC compare to other FMCG giants in India?

Screener Specter – Companion for screener.in (24-08-2024)

Thank you for the feedback! Sector-specific ratios are indeed an important consideration, and future versions of Screener Specter will explore incorporating this aspect to provide even more tailored insights.

Aditya Birla Fashion and Retail Ltd (24-08-2024)

Thanks @tanayshah1103 for sharing this. The plans seem great. However, I don’t know abt the profitability. Like if we see, all major retail clothing brands are under aditya birla fashion and retail. But the company still finds it hard to make the business profitable. I guess company is not very good in managing the Unit Economics of stores. But I think that’s the problem with all MNCs… profits of Good businesses go into loss making businesses. So yes, I think even if aditya birla reaches the revenue target, the profitability will still be in question.

Is China investible? (24-08-2024)

After sitting on the sidelines & observing for quite some time, I entered China via Mirae Asset Hang Seng TECH ETF based on fundamentals with Half position size & will deploy fully once technicals start improving.

The story is always woven to fit the price narrative…Everyone is bearish on China and going by basics You have to be greedy when others are fearful…Of course, you have to ensure fundamentals are in place.

Once it crosses 30 EMA & 9 EMA crosses 30 EMA on a weekly timeframe, momentum will follow

Some of the smart money is moving already

Michael Burry portfolio 2024

I explain more in detail in this video ![]()

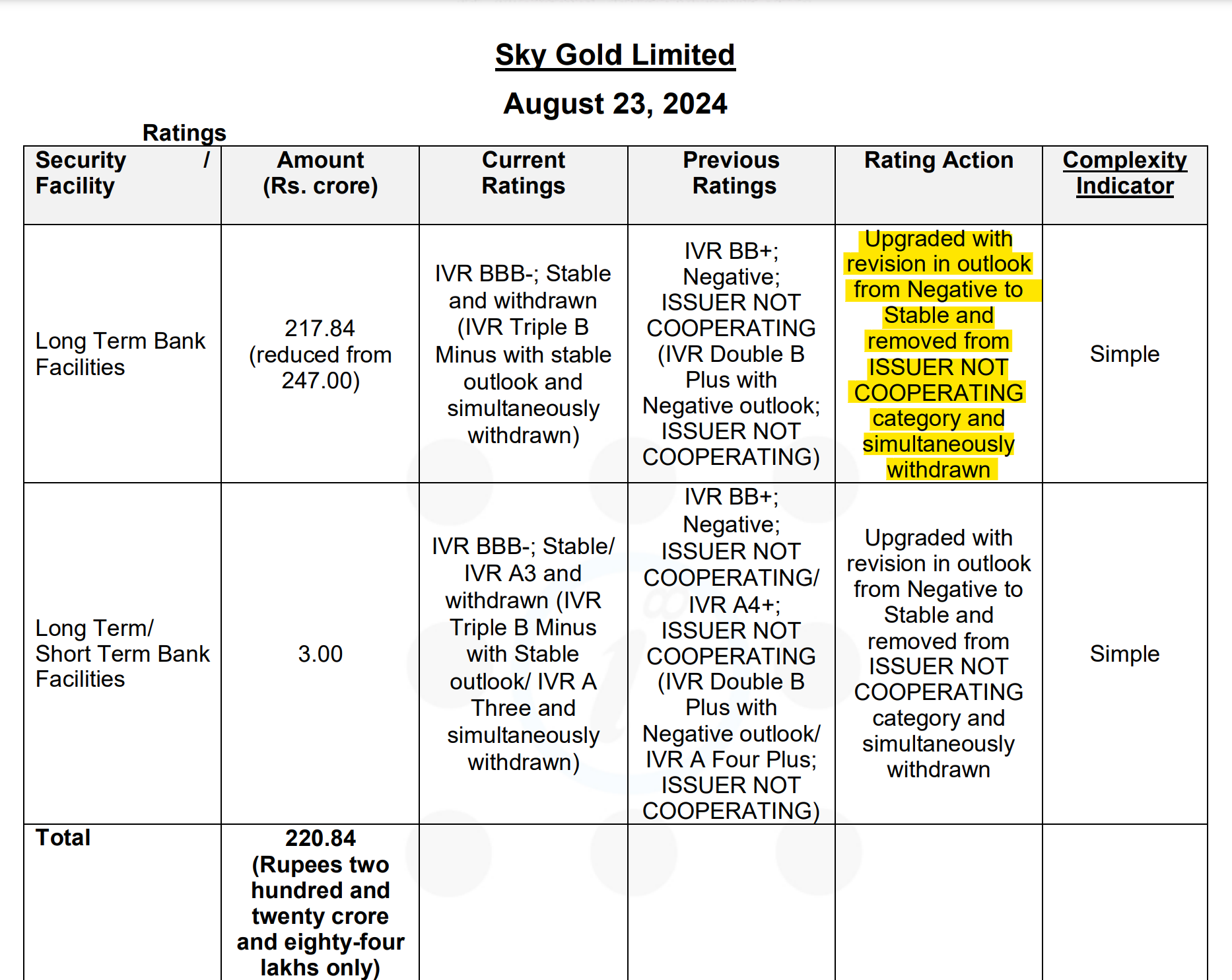

Sky Gold ltd. – Will it reach the sky? (24-08-2024)

Positive Development.

Kirloskar Electric – A Turnaround Bet? (24-08-2024)

From AR 2023-24

Dear Shareholders,

I am pleased to present 77th Annual Report of Kirloskar Electric Company Ltd for financial year 2023-24 on behalf of our Board of Directors. Despite a challenging operating environment, we have delivered positive financial results and continued to create value for all Stakeholders. As the Chairman of your Company, it is my privilege to reflect on our achievements, challenges and the path forward in this dynamic industry.

Similar to numerous other sectors, our industry is also undergoing a swift progression and novelty in technology. Throughout the year, even in the face of uncertain economic conditions we have overcome obstacles with tenacity and flexibility. The dynamic landscape of digitalization presents us with opportunities and challenges, encouraging us to adapt and advance. We upgrade the technology for our products from time to time to meet the market requirements and to keep our standing in the industry.

Three main pillars were at the center of these efforts: (1) enhanced capacity utilization; (2) cost optimization; and (3) stepping up our export focus. These pillars shaped our decisions and actions over the course of FY 2023–24. This year, we have improved capacity utilization and drastically optimized production costs for motors, transformers and switchgear.

One of our key achievements this year has been the successful supply of various transformers through EPCs for Bihar Water Supply Schemes and Punjab Water Supply Schemes, under Government of India’s prestigious initiative viz, ‘Jaljeevan Mission’. Besides this, we have successfully conducted short circuits tests in CPRI, on various transformers including 40MVA, 33/11.5kV, 16MVA, 11/3.45kV and supplied to various power projects including IOCL, NTPC, SAIL, Sikkim Power etc. Our notable achievements also include, the supply of our various products in association with leading EPCs, OEMs and OEAs catering to diverse applications and customer requirements strengthening our market position and driving sustained growth.

This year, we anticipate a dynamic growth trajectory fuelled by a number of key strategic considerations. Above all, our strong and robust order book for both customized product orders and standard products order establishes a solid groundwork for long-term expansion. These tailored solutions secure a consistent revenue stream, create long-lasting relationships and match our customers’ needs.

Our product reach in the mobility sector is wide and constantly expanding. India’s emphasis on domestic manufacturing and technological innovation offers us chances to expand and support the global mobility revolution. India’s EV market has experienced a sharp increase in business this year. As the demand for EVs increase, there is a great opportunity for our business to grow and for us to contribute to the success of the EV ecosystem in India. Your Company is in a perfect position to take advantage of the revolutionary changes occurring globally and ride the waves. Your Company’s proven manufacturing capabilities and preparedness for market competition put it in a strong position to take advantage of energy transition opportunities as they present themselves.

Establishing a work environment that fosters individual development, inclusivity and diversity is our goal as we strive to be the one of the best place to work for people who share our enthusiasm and values.

As we look ahead, our vision directs us and pushes us to achieve new standards of excellence, our objective keeps us grounded in providing all of our stakeholders with sincere and committed services, while our vision guides us forward by encouraging us to achieve even greater heights of excellence. Together, we will overcome obstacles, take advantage of chances and leave a lasting impression to ensure our success and prosperity on this life-changing journey.

I would like to conclude by sincerely thanking all of our stakeholders, including our esteemed bankers, suppliers, customers, dealers, channel partners, service providers, shareholders, employees and board members for their unwavering support, faith, and belief in our business. With our combined efforts, I have no doubt that we will keep breaking records, surpassing goals and leaving an enduring legacy.

Again, I want to thank you for your support and confidence.

Vijay R. Kirloskar

Executive Chairman

Kirloskar Electric – A Turnaround Bet? (24-08-2024)

(post deleted by author)