New Swift Dzire scored 5 star safety rating in GNCAP. Maruti is back with Bang. If they manage to do this with Ertiga, Fronx, Baleno. I think they’ll definitely eat into sales of Tata/Mahindra.

Posts in category Value Pickr

Samarth’s Portfolio & Learnings (12-11-2024)

Very well written Samarth

Hyundai Motor India Limited – HMIL (12-11-2024)

Hyundai Motor India, reported a 16% drop in its consolidated net profit for the quarter ended September 2024 to Rs 1,375 crore. The same stood at Rs 1,628 crore a year ago.

Revenue from operations in the reporting period, too, fell 7% year-on-year (YoY) to Rs 17,260 crore.

The company reported an EBITDA of Rs 2,205 crore in the second quarter, down 10% from Rs 2,440 crore posted in the corresponding quarter of the previous year.

Margins for the quarter too declined 30 basis points (bps) YoY to 12.8% in the reporting period.

Rategain – Fast Growing SaaS Leader (12-11-2024)

I am following the stock.

Stock correction in price due to these reasons

1.Loss of business with one Major client

2.Decrease in revenue growth projection for H2FY25 from 20%to 10-12%.

3.Normalisation of travel trend after COVID boom

4.Monitoring agency CRISIL objection about QIP .

And correction is mainly due to valuation.

However management is known for conservative in nature.

Management guided that it won a big deal but can not disclose as deal is not signed yet .

It will work towards increasing revenue

I totally like the leadership under Mr Bhanu

I hold the stock… and may be biased.

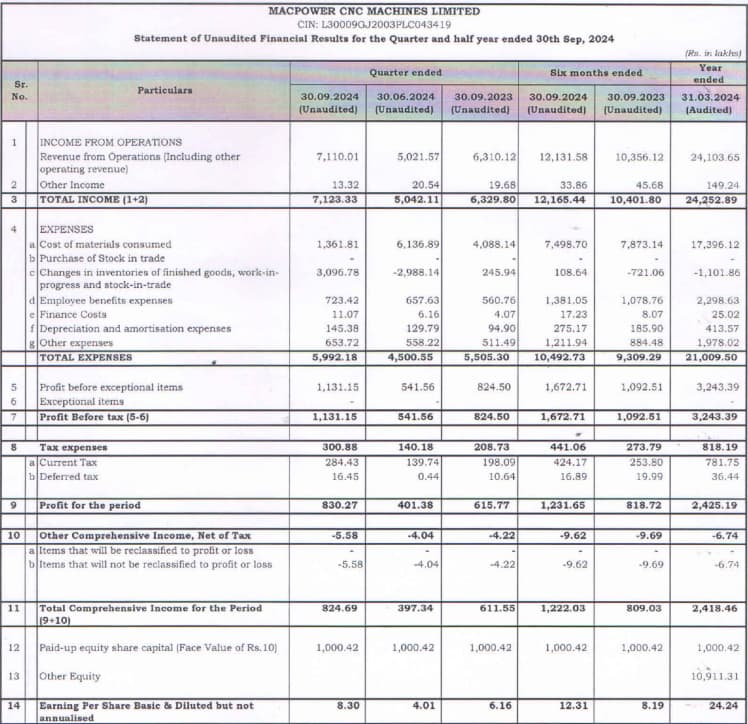

Macpower CNC Machines: Manufacturing a Strong Growth? (12-11-2024)

Good set of numbers…

Cashflow trend is not so good.

Hitesh portfolio (12-11-2024)

Hi Hitesh,

I believe OAL reacted negatively yesterday to Mangalam organics result. The revenue had 18% Degrowth & whatever profit was attributed to decreased raw material cost.

Voltamp Transformers (12-11-2024)

Yup decent observation but there is one thing lacking here both TRIL and Shilchar have renewable exposure. Shilchar has 100% focus on renewable. Voltamp is not so much into renewable maybe that is bigger contributer to less momentum. Voltamp management is seems to be very wise.

When we talk about transformer shortage it applies to all kinds of transformers i don’t know the split of non renewable to renewable transformers but that opens them to a very big risk especially Shilchar they have all thier eggs in one basket.

22 carat shines more than 24.

Danish Power Ltd (12-11-2024)

Hello Anshul…nice write up

How Danish fare when compared to product range of TARIL or supreme or shilchar ?

Although the sector from surface looks good and there have been lots of report/notes from analysts on the transmission & power sector these days.

They may look they are all in the same league when we compare them based on installed MVA capacity but i think they are different. I feel the the comparison with each of these transformer names based on clients would give crisp picture and it can give more clarity on the growth potential.

Being SME, i doubt, if many data can be collected but it would be nice if data on order book are available like others.

D-Invested at TARIL.

Tinna rubber – recycling a rubbery growth path (12-11-2024)

I recently broke down some key details of this q2 results on twitter. I feel company has solid management and roadmap ahead.

Road infra growth is inevitable along with the fact that every monsoon half of our roads are washed away.

In rubber with bitumen supply for road infra Tinna rubber is monopoly with 60% market share as mentioned in thier investor ppt even after that they are expecting more growth in this segment.

Disclaimer : Added first installment today so views maybe biased.

COSMIC CRF LIMITED – sme (12-11-2024)

Money is stuck in inventory and receivables. Has anyone here done work on cash flows? Would appreciate any views.