They haven’t been able to penetrate the south Indian market yet. South Indians are generally brandy and rum drinkers. If they manage to capture a part of south Indian market with Camikara it will give a considerable boost to overall revenue. Tamilians generally prefer brandy and Keralites are mostly rum drinkers. Many premium Indian brands including Indri are not available in Kerala. Keralites who are into single malt buy Indri from duty free when they travel abroad. Market penetration is a big issue in states where the market is controlled by state govt owned beverage marketing corporations.

Posts in category Value Pickr

DDev Plastiks Industries – A Smallcap Gem (23-08-2024)

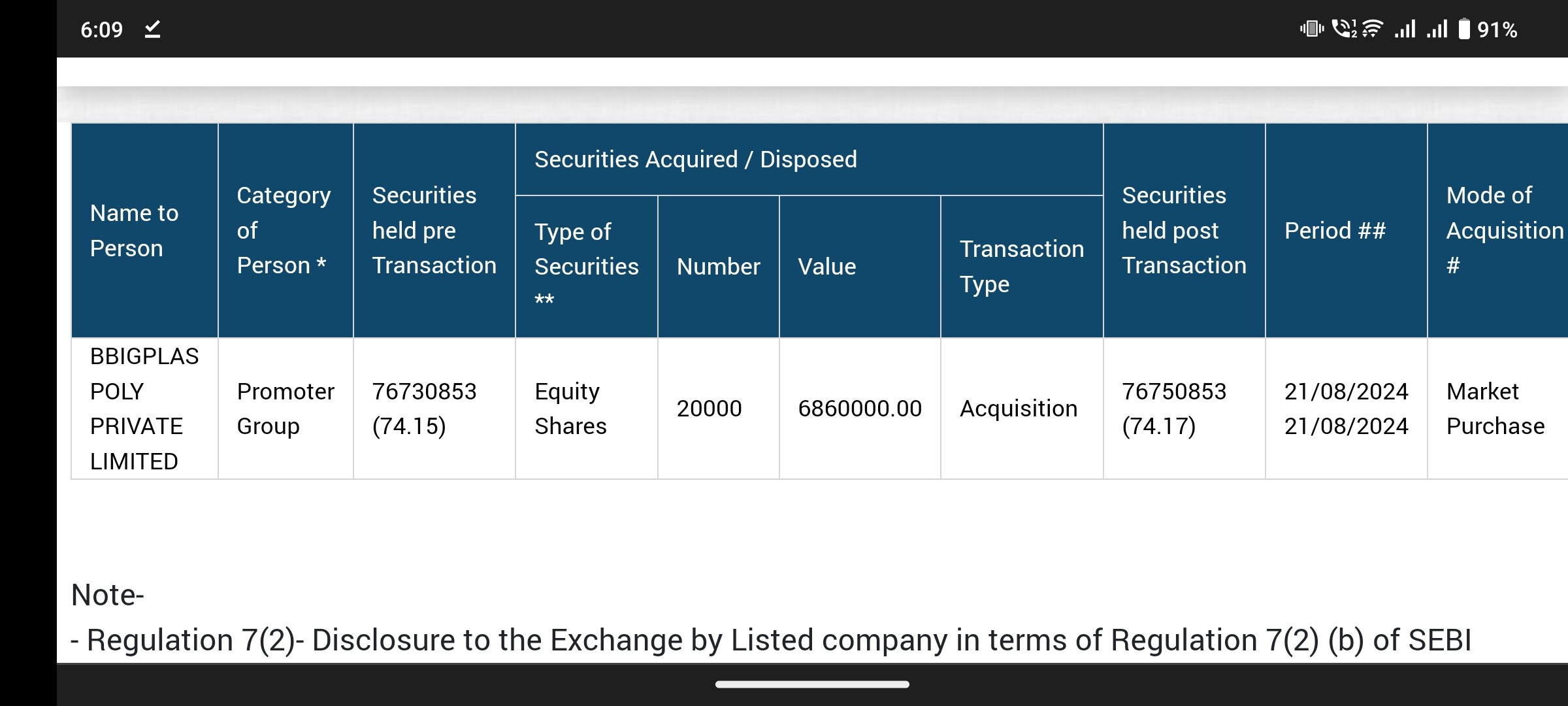

Promoter has purchased. SH now stands at 74.99%.

Mazda Ltd – Sheer Undervaluation? (23-08-2024)

Any views around revenue degrowth for the lastest 2 quarters?

Tata Consumer Products Limited (TATACONSUM) (23-08-2024)

I am trying to understand how to think about the benefit to existing stock in this Rights Issue.

If yesterday’s stock price was 1205 and the Rights issue was 818. Should we think we got a discount of 387 rupees per share?

Sula vineyards – pioneers in indian wines (23-08-2024)

Why the promoter share holding is very low in this company. Even though they are makeing huge capex and good branding

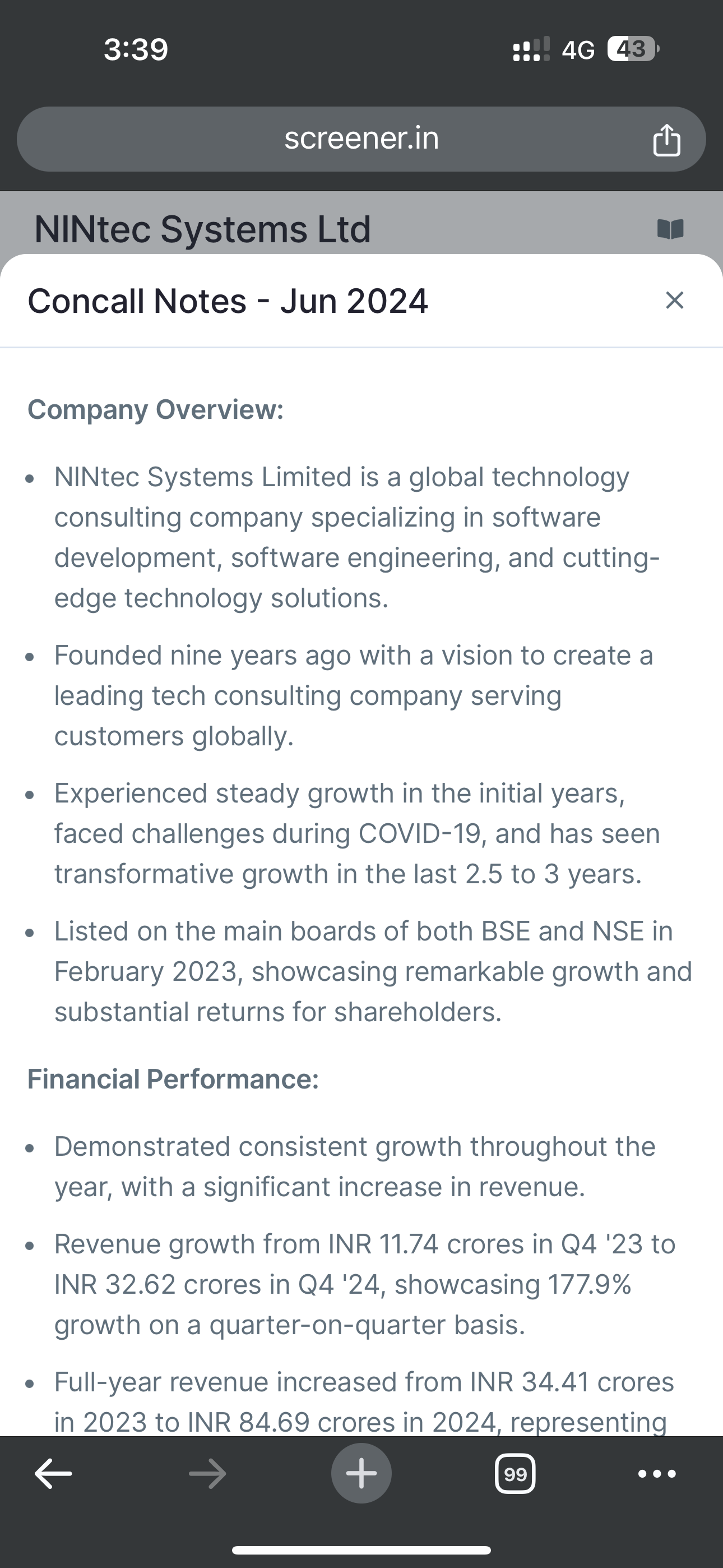

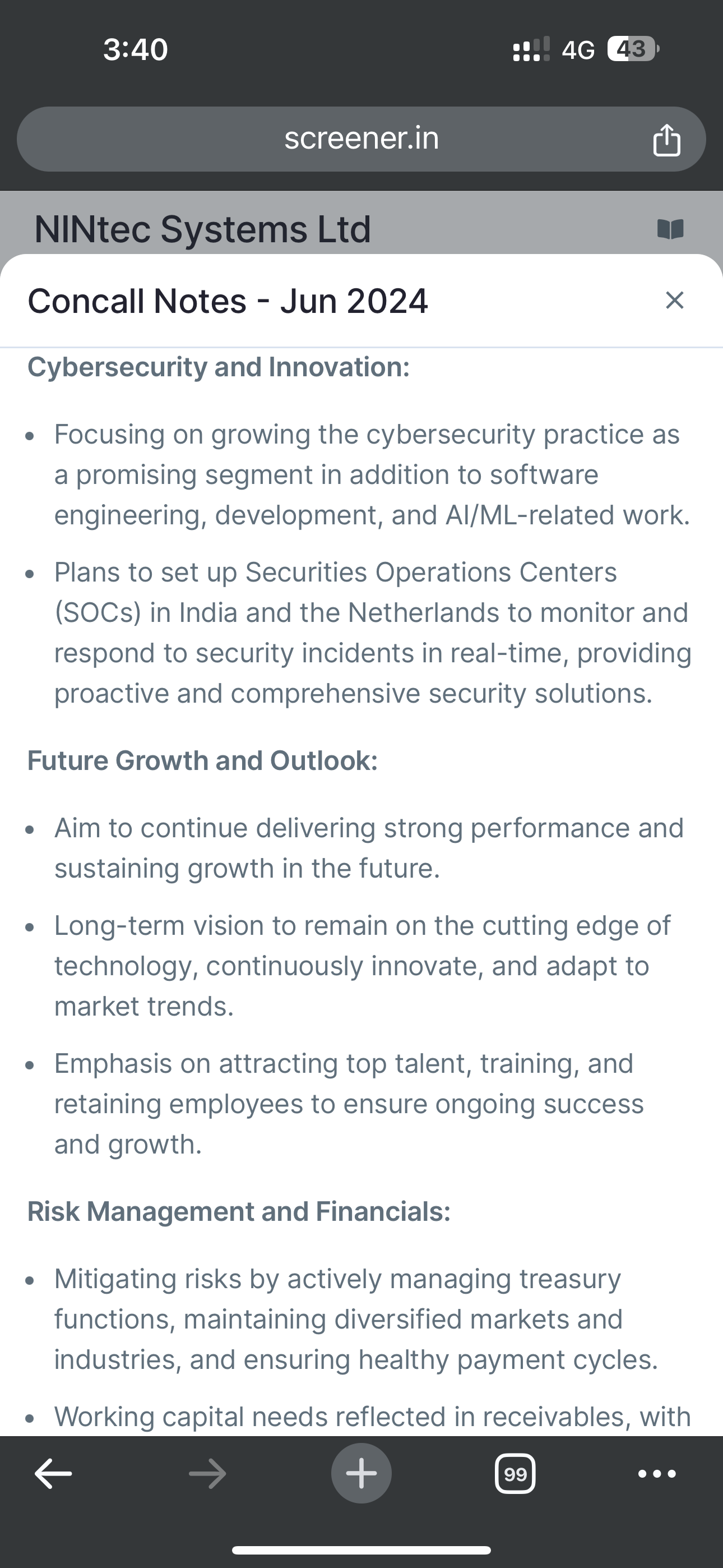

NINtec Systems Limited: A High Potential Microcap IT Company (22-08-2024)

Also attaching the concall notes by screener for reference:

NINtec Systems Limited: A High Potential Microcap IT Company (22-08-2024)

For the 2nd question, all the use cases are mentioned on their website… please refer the ‘services’ section.

For the 3rd Question, the exact structure and relationships between these companies are not entirely transparent, but here’s what is known:

- NINtec Systems Ltd. (India): This company is the core IT services provider within the group, offering a range of technology solutions including application development, cloud services, and business analytics. It primarily serves international clients, particularly in Europe and the U.S.

- NINtec B.V. (Netherlands): This entity is likely a subsidiary or sister company of NINtec Systems Ltd. and plays a critical role in managing and expanding the company’s operations in Europe. The Netherlands-based company might focus more on client engagement and delivery in the European market, leveraging the technical expertise and services developed in India.

- Gateway Digital: Gateway Digital seems to operate as a related entity within the same corporate group. It specializes in digital transformation services, which could include more strategic and consulting-oriented offerings compared to the primarily technical services of NINtec Systems. Gateway Digital likely complements NINtec’s offerings, targeting a slightly different or overlapping market segment.

The companies appear to share common ownership or management, functioning as part of a global network. This structure allows them to tap into different markets with localized offerings while maintaining a strong global presence. However, the exact ownership hierarchy (whether NINtec Systems Ltd. is the parent company or if there is a holding company structure above them) is not clearly documented in publicly available sources. I am assuming most probably they are trying to build synergistic relationships between all the sub-entities to offer wider range of services…

Let me know your thoughts too

IDFC First Bank Limited (22-08-2024)

Thanks for the clarification. Though I do find it difficult to digest that some entity can continue to be overvalued for long periods of time just on basis on this one word TRUST.

I remember even in capital first these guys were posting ROE of 6 to 8 in 2015 and always valued 3.5 to 4 price to book while Indiabulls was posting 25 return on equity and had price to book of 1.2 times.

Even then I could not understand what is going on.

Regarding credit cost they have said that more credit cost in JLG is because of “multiple factors such as general deterioration in JLG customers behaviour, Chennai floods etc. To speflcifically quote the letter in Annual report.

Quote “For FY25, we expect provisions to be more upfront in H1-FY25 due to normalisation of credit costs post COVID, impact on MFI book in recent floods in Tamil Nadu, and a reduction in center-meeting discipline in MFI, among other factors. We havecommunicated this during Analyst calls for Q4 FY24 and Q1 FY25. We will monitor performance on this portfolio and will share with the street faithfully. Except MFI, the rest of the book is performing on expected lines.

The microfinance business is crucial for us as it helps meet our PSL targets of lending 12% of the portfolio to weaker sections. Therefore, in terms of risk-reward and profitability, this business is important to us.

Overall, over the past five years, our credit performance remains within our overall internal risk frameworks and aligns with our public guidance.” Unquote

To me, one product JLG, having higher credit cost is not an issue, every microfinance company has reported this issue so looks to be consistent with the market. Indeed if they get 1.85% credit cost for the bank as a whole, it would be “normalization” to pre-COVID levels as mentioned by the management. Frankly 1.85% would be amazing considering that the NIM is 6.3%. In fact, the question is the other way round can the bank sustain credit cost at only 1.85%.

One thing stand out the credit cost of this bank post covid from FY 22 to FY24 put together is only 1.6%. So thus far they have been able to maintain low credit cost even after COVID. Sp when the chips are down they have delivered low credit cost.

Compare this to Yes bank (major cleanup of 16% in FY 21), Bandhan bank (4%-6% for 3 years after covid), Indusind bank (v high provisions during COVID, etc, this bank has low provisions to average book thus far post covid. Even post demonetisation etc it was low.

The issue is not credit cost frankly its their strength. Looks like they have a good stable model. I have been watching it from capital first time. The issue is cost to income ratio.

They have guided for higher credit cost (effectively lower PAT in Q2 25 lets see where it goes. But more importantly, lets see if they can maintain deposit growth, they have cut deposit rates to 3% upto 5 lacs. Overall it’s a bank in the making with many changes all the time. To quote you, we have to only sit in “TRUST”, humour and pun intended.