Alchemy is backed by Jhunjhunwalas. Fund manager (Hiren Ved) has the freedom to decide the strategy.

Posts in category Value Pickr

Shivalik Bimetal Controls Ltd (SBCL) (21-08-2024)

I don’t have any reading. My point was limited to Econ 101. If you lower prices, you will sell more quantity. Also note that my point has nothing to say on margins. It’s just a simple relationship between price and volumes. To repeat, if you lower prices you will sell more quantity.

So you can’t call that an achievement; whatever words may be used to describe it, as the CFO did – “strategic focus” / “resilient demand (really!!)” .

Everything else; like ‘we sold more in domestic’, ‘we sold more shunt / less bimetal’ etc etc are explanations for the outcome. I don’t have much to say except that we should be very careful not to mix up cause and affect / stimulus and response. For instance if my employee comes and tells me that he sold more in domestic and less as exports; then was selling more in domestic which fetches less, a stimulus (i.e. did we purposely do it to make less money? wouldn’t that be dumb) or was it a response (export demand was weak so we responded by selling more domestic to keep utilisation going). He may cloud his reasoning as well as ours by saying – “I sold more domestic because demand was high”, “this is my strategic focus” etc etc; but the real reason is that he could not sell in the export market.

Commodity and Cyclical Plays (21-08-2024)

From Bloomberg, originally:

Welcome to the end of the biggest commodity boom – The Economic Times (indiatimes.com)

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (21-08-2024)

Disc: invested

Piccadily Agro Industries Ltd (21-08-2024)

Rekha Jhunjhunwala picked up stake in Piccadily in preferential allotment.

JK Lakshmi Cement (21-08-2024)

not invested opinion other comments are welcome fact check it correct

- Merger Overview:

- Udaipur Co. is merging with JK Lakshmi Cement. JK Lakshmi will issue 4 equity shares with a face value of ₹5 each for every 100 equity shares of ₹4 each held in Udaipur Co., excluding the shares already owned by JK Lakshmi.

- Ownership and Shares:

- Udaipur Co. has 224 crore shares, 75% of which are owned by JK Lakshmi. JK Lakshmi Cement currently has 59 crore shares outstanding. The share prices are ₹34 for Udaipur Co. and ₹779 for JK Lakshmi.

- Dilution Calculation:

- The merger leads to the issuance of 2.24 crore shares to Udaipur Co.’s minority shareholders, resulting in a 3.66% dilution for JK Lakshmi Cement’s shareholders.

- Benefit to JK Lakshmi:

- JK Lakshmi benefits because it doesn’t issue new shares for the 75% of Udaipur Co. it already owns. This minimizes dilution and concentrates the benefits for JK Lakshmi’s existing shareholders.

- Impact on Udaipur Co.’s Minority Shareholders:

- Udaipur Co.’s minority shareholders might perceive the deal as less favorable. Their stake in the merged entity is smaller, and they lose direct control over Udaipur Co., potentially feeling that their shares are undervalued.

The overall takeaway is that while the merger is beneficial for JK Lakshmi Cement, it may not be as favorable for Udaipur Co.’s minority shareholders due to the concentrated dilution and loss of control.

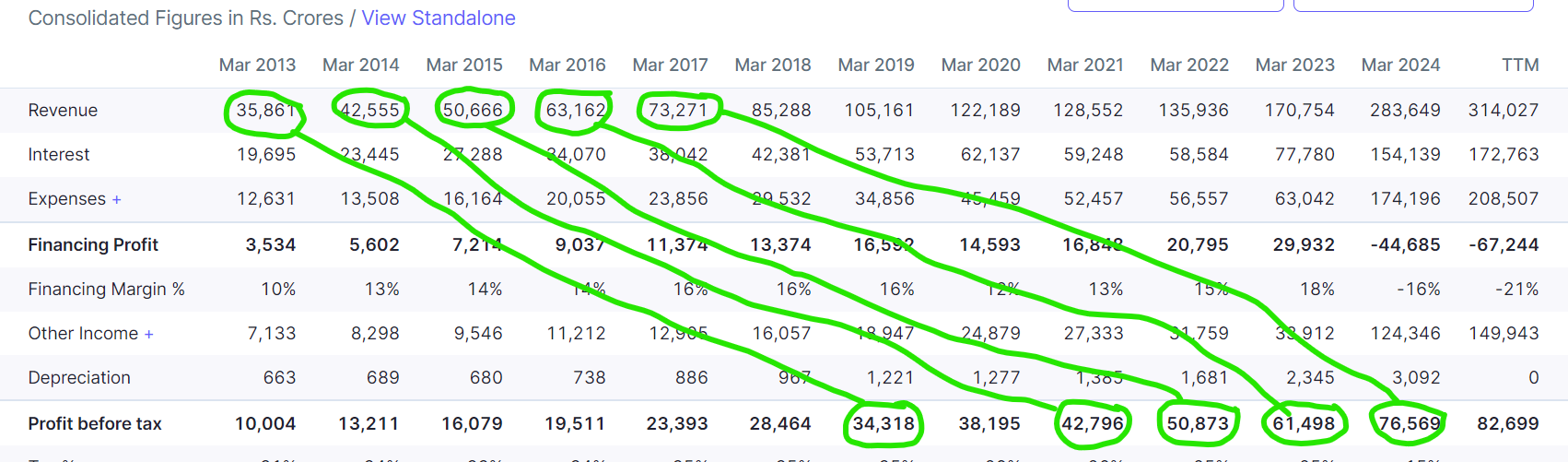

HDFC Bank- we understand your world (21-08-2024)

Interesting Revenue-PBT Pattern with a lag of 6-7 years.

Can this be repeated in future? Disc-Invested.

Oct-2019, Raamdeo Agrawal : One of the things is that credit intensity in the economy which is about 70 percent of the gross domestic product (GDP) – so Rs 200 lakh crore of our GDP, the outstanding credit must be about Rs 140-150 lakh crore. But world over what happens is the next $3 trillion will have a significantly higher credit intensity. So if the credit flow is not there, there is no GDP.

You can make it minus 100 percent and there is no GDP growth. That kind of thing. It is just one-to-one correlation. So it is a tower of credit. So my sense is that we will go to $3 trillion, we wrote about this trillion dollar economy in 2008. So we are watching it for the last ten years, it will go to $6 trillion and it will go to $12 trillion also, but let us talk about this $6 trillion and this will happen by 2026-2027.

When this happens, you will need about Rs 200-250 lakh crore of credit to be underwritten in next six-seven years.

E2E Networks Ltd – Listed small Cloud computing player (21-08-2024)

This is a race of multiple factors: software, hardware and price. All the industry players–Alphabet, Amazon, Apple, Microsoft, Digital Ocean, and so on—are in the race. If E2E has slightly less efficient chip, it does not imply that their whole business would become obsolete. In many cases, they would have the time and money to play catch up.

E2E is depreciating computing assets assuming lifespan of around 5 years. They will have to transition to the better chip as it becomes available. There are two risks here: such chip may not be available to them, and such transition may not be feasible in their existing data centers. We will need to watch out.

Even if Apple Cloud becomes a dominant player in Cloud Computing (yet another hyper-scaler) using its own chips, the enormity of the market size will allow the likes of E2E to keep growing.

Lower price of E2E is an attraction. How well their software offerings of cater to particular industries compared to the other offerings? This question will influence the demand.

Spotting a Reverse merger – Shell(Holding company ) Merging with healthy profitable private company (21-08-2024)

801533fb-41a4-4cc6-b3eb-36085d37fc29.pdf (222.9 KB)

Spotting a Reverse merger – Shell(Holding company ) Merging with healthy profitable private company (21-08-2024)

Hi does pref allotment indicate a move