On the demand from Defence, dont see any prospects. I have some idea on how it works.

Posts in category Value Pickr

E2E Networks Ltd – Listed small Cloud computing player (20-08-2024)

Any thoughts on the valuation?

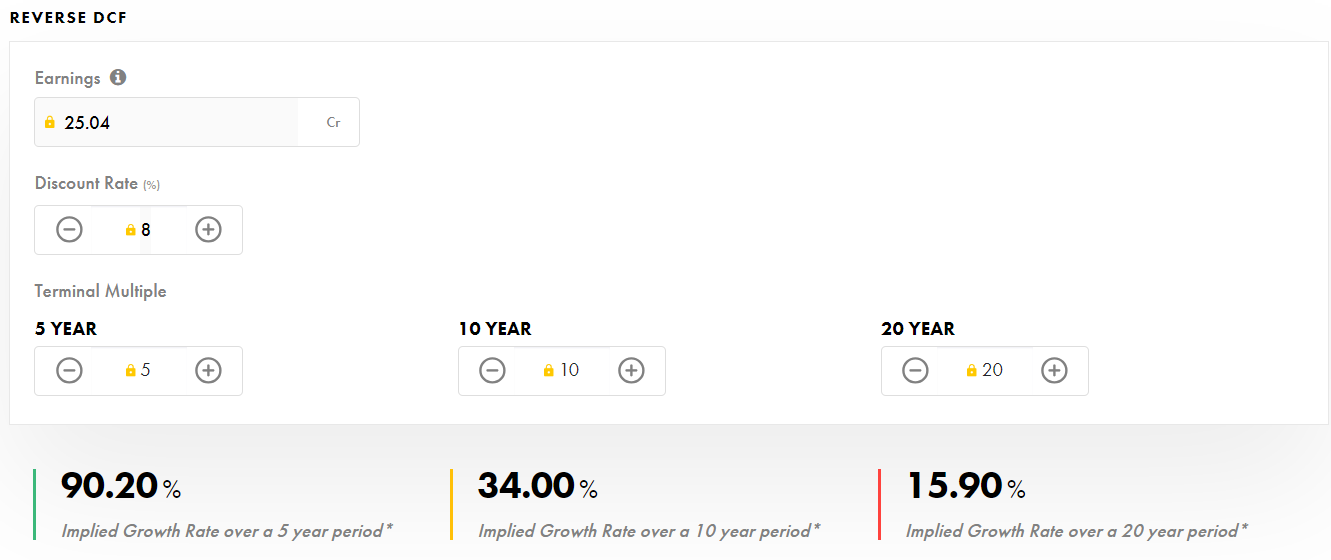

A quick look at reverse DCF (to ponder over the growth assumptions built into the price) per Tijori yields the following:

90% growth required over the next 5 years per to justify this valuation! ![]() In tech where the obsolescence cycle is very short, looking beyond 5 years does not make sense, IMHO.

In tech where the obsolescence cycle is very short, looking beyond 5 years does not make sense, IMHO.

AllCargo Logistics – Are good time ahead? (20-08-2024)

- Consolidated revenue for Q1 FY25 was Rs. 3,813 crores, up from Rs. 3,271 crores in Q1 FY24

- EBITDA for Q1 FY25 was Rs. 133 crores, down 5% YoY but up 34% QoQ

- Reported PAT of Rs. 4 crores compared to a loss of Rs. 12 crores in Q4 FY24

- Consolidated net debt stood at Rs. 434 crores as of June 30, 2024

- International supply chain business saw 6% QoQ growth in LCL volumes and 9% YoY growth in FCL volumes

- Express business EBITDA up 33% QoQ on improved operational efficiencies

- Contract logistics revenue up 13% QoQ and 22% YoY

- Focus on standardizing operations and outsourcing to reduce costs

- Driving automation to maintain costs against inflationary pressures

- Expanding in underrepresented markets like Argentina, Uruguay and Paraguay

- Launching new products and trade lanes to drive revenue growth

- Seeing sequential improvements across all businesses

- Trade environment has been buoyant with demand exceeding expectations

- Expecting sustained recovery in trade volumes until end of year

- Freight rates expected to remain stable or range-bound in near term

- Supply chain issues like Red Sea crisis and US port congestion creating container shortages

- European economies remain subdued, but growth seen in Asia, US and South America

- Expect European demand to potentially pick up in 2025

- Expect continued positive trend in volumes and profitability for coming quarters

- Focus on expanding market share and outgrowing the market in LCL and FCL businesses

- Anticipate improvements in utilization and operating leverage to drive profitability

- Business seeing recovery after challenging 12 months

- Well-positioned to benefit from revival in global trade volumes

- Unique LCL consolidation model provides competitive advantage

- Focus on digital initiatives and automation to drive efficiencies

Management did not provide specific guidance on profit margins. However, they indicated some factors that could positively impact margins going forward:

- Improved utilization: LCL volumes increased 6% QoQ and FCL volumes grew 9% YoY. Better utilization typically leads to improved margins.

- Operating leverage: There is significant operating leverage in the business, meaning incremental revenue growth should disproportionately benefit profits.

- Cost containment: The company has implemented cost reduction initiatives, outsourcing, and automation to keep SG&A costs in check despite inflationary pressures.

- Mix improvement: Increased usage of 40-foot containers (up 9%) which are more operationally efficient.

- Volume growth expectations:Continued volume growth for the remainder of the year, which should help spread fixed costs.

- Yield improvements: LCL yield (gross profit per cubic meter) to improve beyond previous levels as volumes grow.

Mazagon Dock: aptly called “Ship Builder to the Nation” (20-08-2024)

may I know on which Drone stock you bet on ?

Dynamatic Technologies – Can it be Dynamite (20-08-2024)

A very Interesting interview. Must Watch

Inside The Indian Company That Supplies To Boeing, Dassault Aviation & More

Strong bounce from EMA 200

All E Technologies, making businesses ready for AI (20-08-2024)

You might find this video helpful.

How To Find Intrinsic Value Using Reverse DCF On Tijori Finance?

SWELECT ENERGY SYSTEMS LTD – some information from Annual report (20-08-2024)

Solar panel is a volatile business and premium will go sharply down, its a commodity play now, too many players, untill results are swelect will keep following down trend.

SWELECT ENERGY SYSTEMS LTD – some information from Annual report (20-08-2024)

Recently, I observed prices correcting sharply and I’m scratching my head, what went wrong with this business. I could not find any positive or negative news since the last communication from the management. There is limited information available and no con call from the management to know what’s happening here. If possible, can anyone update with latest information.

Poonawalla Fincorp formerly Magma Fincorp (20-08-2024)

As per my understanding the fall in share price is because the perception of the street changed as the earlier management guided for low OPEX and no expansion in branches for next 4-5 years. And the new management is emphasizing on more branches which will increase their OPEX cost. I think the Pedigree of the new management is much better if not same than the earlier management and as they walk their talk the market will again rerate this stock. I am very confident that this stock should start performing from here as the Interest rate cut is around the corner. If one is looking to play the NBFC theme this is one stock to look out for!

Sheetal Cool Products Limited (20-08-2024)

now its working, pls chk !