Hi @harsh.beria93 , I have been following your posts quite regularly and very impressed with your picks and analysis. Haven’t seen you selling much. Is your selling on timetechno a portfolio rebalancing act or you see froth in this scrip?

Posts in category Value Pickr

Globus Spirits (20-08-2024)

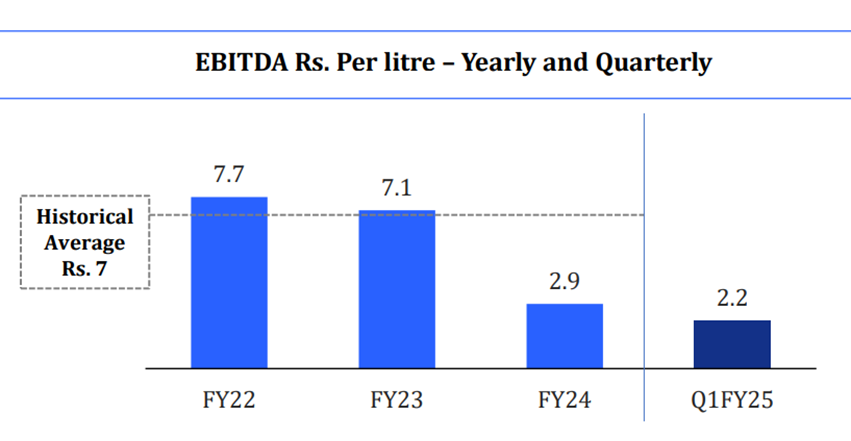

After a lot of quarters of declining margin globus showed an increase in the margin for the first time. Even though, the margin increased only slightly its still good to see positive developments.

The company completed expansion of Jharkand and West Bengal facilities but couldn’t reach the same amount of volume as rice was replaced by Maize. The reduction in volumes is because the amount of maize that can be processed is lower than raize. The company is trying to increase this efficiency and may take a couple of quarters.

The company expects the margin currently to be at lower end and doesn’t expect the margins to go any lower. And expects the margin to trend upwards with the Kharif season harvest (end of Q3).

As for the consumer business, Rajasthan remains strong with 29% market share in country liquor and 68% market share in RML with a cumulative share of 35.5%.

Entered UP in the regular and other segments. UP is a very large market in terms of country liquor and for IMFL. As per management good traction to sales in UP.

Bottling unit in UP commenced production. Entire production for state is from the Unit. Started construction of an 80 KL distillery in UP at a capex of 120 crores. Can be run on either grain or molasses. Expected to be completed in 12 to 16 months.

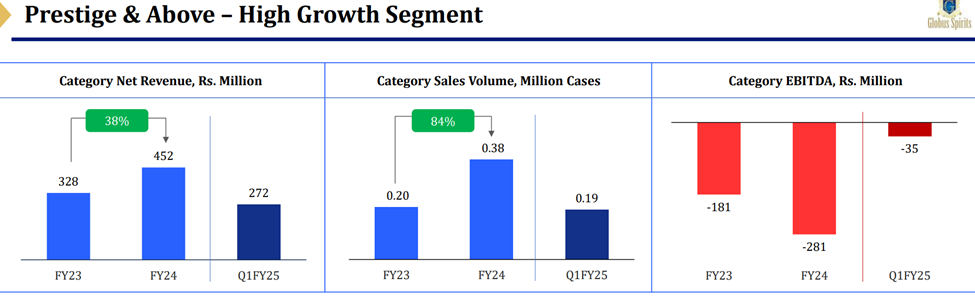

Management expects loss for the P& Above division to be within 15 crores this year. Its launched in 7 states now, no additional state this year. Hoping for 2 out of 5 states where P& A was launched initially to break even this year.

Launching new products in the P& A division. Snoski and Mountain Oak was well received. Another Gin seems to be planned.

Not Out was launched in delhi.

Expected launch of Carib beer to be in Q1’26. Production to be outsourced.

Planning to improve byproduct recovery by producing corn oil and biodiesel expected to be completed by end of year.

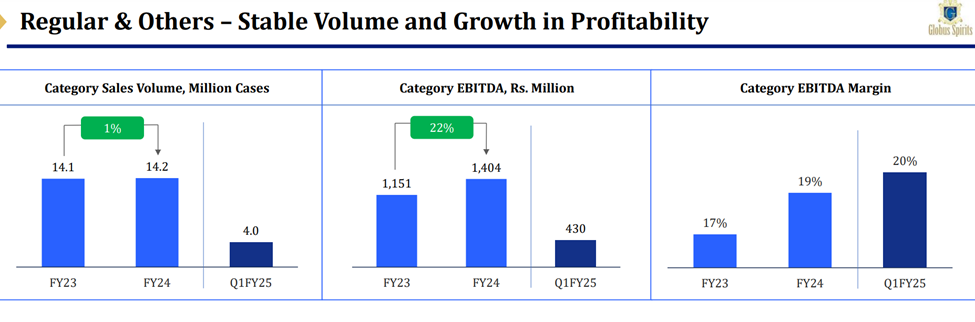

Regular and others

As per management bottling costs reduced by Rs.0.17 per bottle effective August.

Discl: Have purchases in last 30 days. biased

Quess Corp – Human Resources Company (20-08-2024)

Yes, it has an IT business under it whose revenue and net profits should be valued at much higher multiples than workforce management business

Responsive Industries: Luxury Flooring Brand? (20-08-2024)

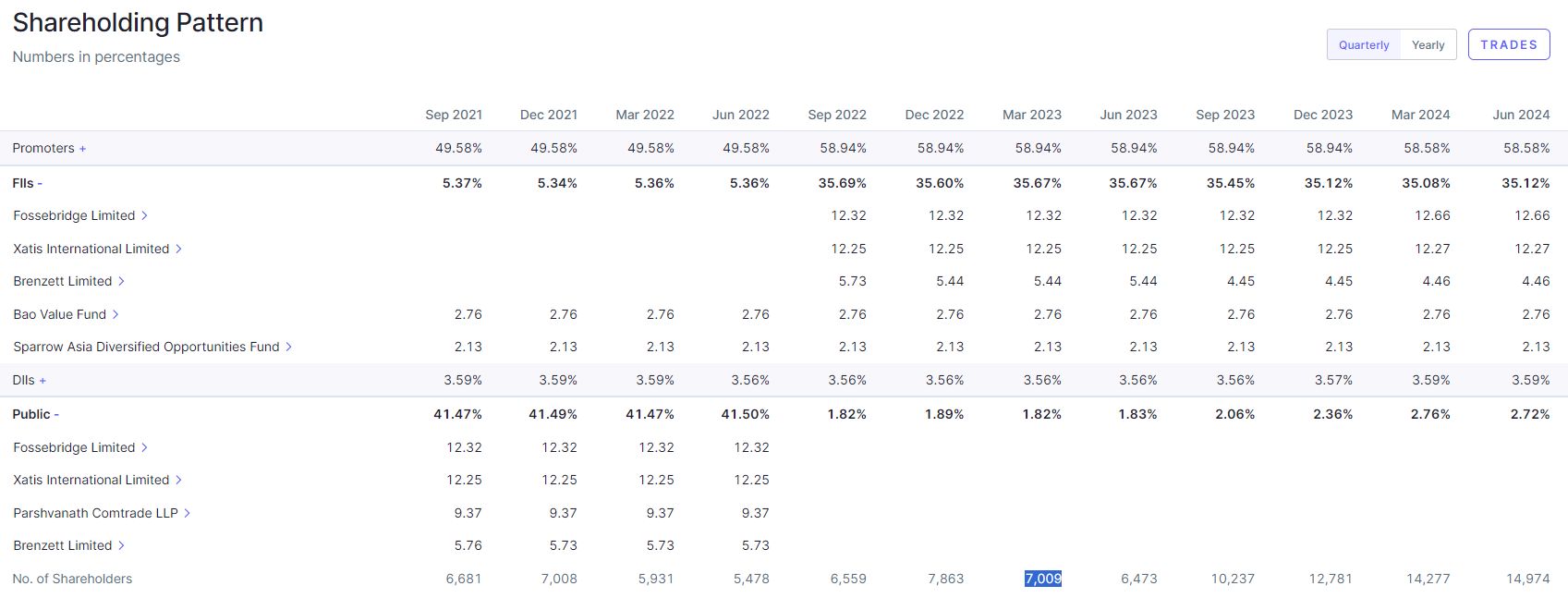

I have looked at the holding breakdown. I would let the regulators do their work and not worry about it until something negative is officially announced by the regulator. It’s just me and how I process these kind of items – which might not be the right approach for someone else.

The entities you have mentioned have been holding the stake for last many years now. Public shareholding has gone up by ~1% since March of 2023 which has been supplied by FII and Promoters. Available float is just 2%-3%. 150cr-200cr max given current market cap.

Two things can happen when float is so low, in my view. Either these entities might offload more which can act as overhang on the price and one can get an idea that “smart money” and insiders are cashing out. Or there can be crazy momentum on the upside, if the demand from new investors starts to roll in as business execution continues. So one would have to keep a close eye on no of shareholders and future shareholding breakdown.

Awfis Space Solutions: Flexing its Muscles in the Market (20-08-2024)

Awfis in its quarterly call mentions EFC India as their competition in the listed space.Do watch out for that company aswell if you are following this space

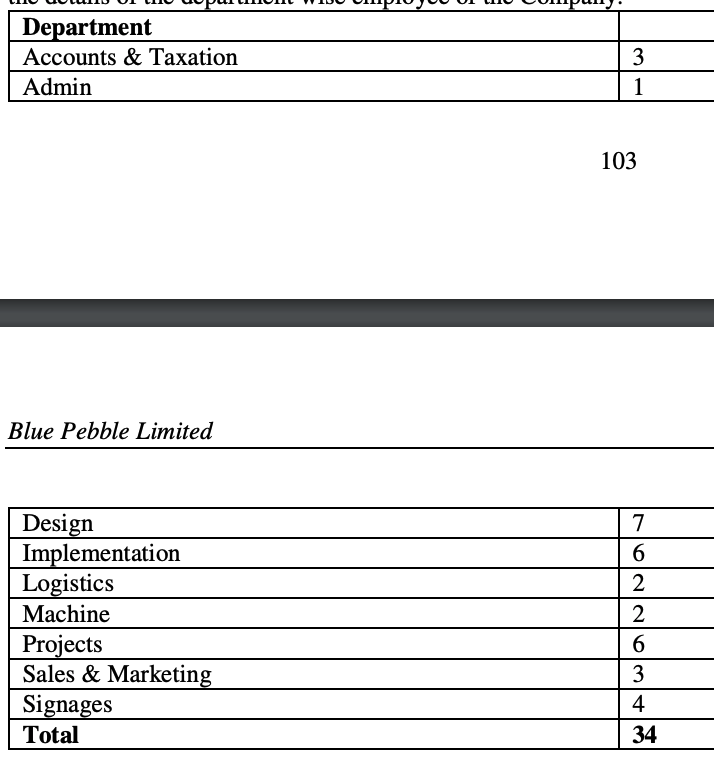

BLUE PEBBLE- The next high growth SME? (20-08-2024)

Employee Count across departments (Source:RHP)

For me, biggest risk would be non-scalability. As their current teams are pretty small, it would be interesting to see how they scale up their team as they grow.

Another concern is customer concentration. Top 10 customers account for roughly 80% of current revenue.

Time technoplast (20-08-2024)

Another solid set of nos, with sales growing by 14% and EPS by 41%. They are very confident of maintaining 15%+ sales growth and becoming debt free in next 3 years. Concall notes below

FY25Q1

-

Revenue growth of 14% in Q1 (12% in established + 19% in value-added), volume growth of 16%. Targeting 15% growth in next 3-years

-

Capex: 39 cr. (18 cr. in established + 21 cr. in value added). Will be ~150 cr./year for next 3-years totaling 450 cr.

-

Debt reduced by 38 cr. in Q1. Will become debt-free in 3-years

-

Working capital reduced to 100 days and should further reduce to 85-100 days in 3-years

-

Middle east divestment proceeds will be realized in 60 days

-

Non-core divestment: Realized ~30 cr. and targeting to realize ~60 cr. by end of FY25 totaling to 90 cr. in FY25

-

Import: on CIF basis, 60% RMs are imported (mostly from Middle east) and 40% are domestically procured

-

Export: only exports LPG composite cylinders, contributes ~2% of overall sales

-

International business: manufacturing is mostly done in the respective countries (30% MENA, 50% Southeast Asia, 20% USA)

-

MENA: plants in Sharjah, Bahrain, Saudi and Egypt

-

Southeast Asia: plants in Thailand, Malaysia, Indonesia, Vietnam and Taiwan

-

USA: 3-4 plants in Chicago, Austin, IOWA

-

-

Expecting 450 cr. CNG in FY25 (vs 308 cr. in FY24)

-

LPG is operating at 90-95% utilization, can do revenues of 230-240 cr. at current state (210 cr. done in FY24)

-

CNG cylinders for OEMs: will focus on commercial vehicles, it’s a 2-3 year process

-

EBITDA margins in LPG and CNG segments are ~18%

-

Solar contributing 10% of their energy which should increase to 30% by FY25 end

-

Pipe plants: 4 manufacturing plants, 1 in Silvassa for western region, 2 in South India (one in Hyderabad and second in Gummidipoondi), 1 in Kolkata for east. Business done through 10-15 EPC contractors (e.g. L&T, Indian Home Pipe Voltas, JSW)

-

92% business is B2B and 8% is B2C

-

NED Energy (based out of Hyderabad) is developing Transparent Container Batteries (TBS; used in railway). Have invested 65 cr. and hoping to reach revenues of 250-300 cr. in 3-years

Disclosure: Invested (sold shares in last-30 days)

Sheetal Cool Products Limited (19-08-2024)

Company domain has been suspended, I am not sure since how long ago.

Seems like big red flag.

Disclaimer: Not holding, under study.

Macpower CNC Machines: Manufacturing a Strong Growth? (19-08-2024)

Some insights from the Q1 Con-call.

- In answering the first question Mr. Rupesh Bhai Mehta said the average realisation will increase to 25 lakhs at the end of the year.

I hear = 22 lakhs per machine x 1605 machines ( 80% utilization ) = 353 crs of revenue

- In answering the second question Mr. Rupesh Bhai Mehta said margin can improve to 27%

I hear 19% Op margins for the entire year = 67 cr

Other income 1 and depreciation as 6 take my PBT to = 62 cr

And PAT to = 46.5 ie. Another doubler of PAT for 2 connective years without diluting equity and without taking debt = High ROCE/ROE

- FY 25 = 24 lakhs per machine x 2300 machines ( 85% capacity utilisation ) = 552 cr

With 24% operating margins = 132 cr

Other income 2 and depreciation 8 take my PBT to = 123

PAT for FY 25 = 92 cr = another possible doubler in FY 25 before the new plant comes up for 2000 machines and doubles the PAT again for the following year but with newer tech available from the new Japanese JV partner and exports markets get accessed through their network.

Reminder, 8% GST return and 200% of research expenses return in the new facility will flow straight to PAT and increasing PAT Margins closer to 20%+. Lately Unheard in the manufacturing space.

Long-Term Vision: I plan to reassess my investment only after the new facility starts production in two years. This decision is grounded in confidence in the company’s strong capital allocation strategy within a supply-side dominant sector. The focus will be on assessing the execution of capital allocation, the associated ROCE/ROE, and, most critically, the management’s commitment to securing superior technology through the JV—ensuring no compromise on technology quality, which is currently unavailable in India.

For further learning we must understand that, The five most important players in the Japan Machine Tool Builders’ Association (JMTBA) based on their global influence, market share, and technological advancements are:

- Fanuc Corporation

- DMG Mori Co., Ltd.

- Yamazaki Mazak Corporation (Mazak)

- Okuma Corporation

- Makino Milling Machine Co., Ltd.

Ranking by Network Size:

- Fanuc Corporation – Largest worldwide network, extensive in over 100 countries.

- DMG Mori Co., Ltd. – Strong global presence in more than 80 countries.

- Yamazaki Mazak Corporation (Mazak) – Extensive manufacturing and technical center network.

- Okuma Corporation – Broad international presence but less extensive than Fanuc, DMG Mori, and Mazak.

- Makino Milling Machine Co., Ltd. – Focused global network, especially in key markets.

This ranking is based on the global footprint of these companies, considering factors like the number of international offices, subsidiaries, distribution channels, and service centers. Fanuc leads due to its unmatched global reach and extensive presence across various regions.

Responsive Industries: Luxury Flooring Brand? (19-08-2024)

If you look at the shareholding, in September 2022, there’s no actual increase in FII shareholding, earlier there were three companies in public shareholding data- Fossebridge limied, Xatis international, and Brenzett limited and these 3 companies were shifted to FII shareholding from public shareholding(I don’t know why). All 3 are registered in British Virgin Island and their beneficial owners are Baidyanath Mahto, Kalpana Kole and Meera Ghosh. Also these 3 companies holds only Responsive Industries shares.

The promters are also not indviduals but different companies registered with the same directors or owners . The increase in promoter % also is a transfer of entire stake from Prashavnath comrade llp to Fairpoint tradecomp llp.