I initially thought the investments business to be 20% of the whole pie and attributed around 200 cr mcap to Oriental Carbon & Chemicals Limited and around 600 cr to OCCL Limited. The proportion provided by the company has come as a surprise to me. If we take the 800 cr mcap as a base (before 1 July 2024), and current mcap of Oriental Carbon & Chemicals Limited of around 270 cr, OCCL Limited should be roughly worth 530 cr map translating into a per share price of around Rs. 110.

Posts in category Value Pickr

Ranvir’s Portfolio (19-08-2024)

Shakti Pumps –

Q1 FY 25 concall highlights –

Shakti pumps is a leading integrated player manufacturing – fabrication technology based solar / electricity operated submersible pumps in India

One of the few players to make solar + submersible pumps and motors in house

One of the biggest beneficiary of PM KUSUM scheme and holds 25 pc Mkt share

Exporting to 100 + countries

Company has 03 integrated manufacturing facilities – all located at Pithampur, MP –

Unit -1 – ( main unit spread across 16 acres ) –

Capacity to manufacture 3.5 lakh pumps / yr ( including both submersible and industrial pumps )

4’‘, 6’‘, 8’’ & 10’’ motor manufacturing plant

Capacity to make – solar structures

Unit – 2 – export oriented unit ( 3.15 acres ) –

Capacity to make 1.5 lakh pumps / yr ( all stainless steel submersible pumps )

Unit -3 –

Capacity to make 2 lakh Variable frequency drives and solar inverters / yr

Customer / Revenue Mix –

State Govts – Via PM KUSUM – 69 pc

Export customers – 21 pc

Other customers – 10 pc

FY 24 revenue break up –

Govt projects – 945 cr

Exports – 286 cr ( export segment has the highest margins )

Others ( including Industrial, OEM, Retail ) – 139 cr

New opportunities –

Incorporated a fully owned subsidiary – Shakti EV mobility – to manufacture EV motors, charging stations, BMS, electric control panels , VFDs and other items. Have sanctioned an investment of 115 cr for the same

PM KUSUM –

Total mkt size of solar pumps under PM KUSUM scheme ( @ Rs 3 lakh / pump ) = 1.47 lakh cr ( for installation of 49 lakh solar pumps )

Out of these, 4 lakh pumps have already been installed. So the remaining opportunity is for 45 lakh pumps to be executed over the next few years

Q1 outcomes –

Revenues – 568 vs 113 cr

EBITDA – 136 vs 8 cr ( margins @ 24 vs 7 pc ). Margin expansion due operating leverage and reduced RM prices

PAT – 93 vs 1 cr

Likely to execute orders worth Rs 2000 cr ( orders in hand ) in next 5 Qtrs

Guiding for a topline of 1700 cr + for FY 25 ( this despite the upcoming state elections in Maharashtra and Haryana – 02 major states where the company is currently supplying )

Company expects the orders Under component C of PM KUSUM scheme to start flowing in about 6 months time

Avg lifecycle to these solar pumps is about 10 yrs

According to the management, the opportunities in the Industry give them hope of being able to grow @ around 25 pc CAGR for next 2-3 yrs as well

Long term EBITDA margin guidance given by the company is in the band of 15-16 pc ( 20 pc plus margins seen in last 2 Qtrs may not be sustainable )

Company continues to spend aggressively on R&D – management believes, this is their company’s lifeline

Company’s existing capacity can generate a max revenue of 2500 cr. Company can keep de-bottlenecking this capacity to meet business requirements. In addition, company has raised 200 cr via QIP to be used to fund doubling of existing facility. The same shall materialise by FY 27

Disc: holding, biased, not SEBI registered

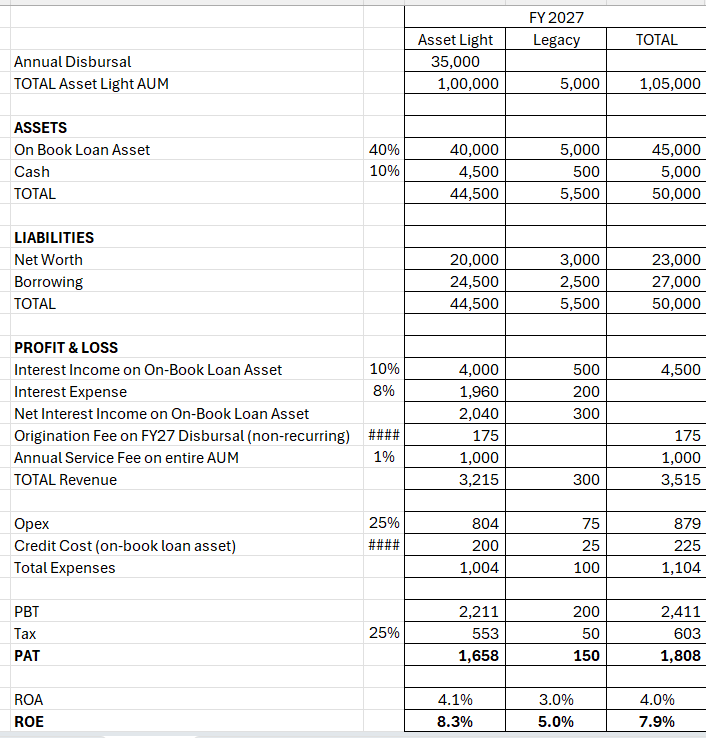

Indiabulls Housing – A compounder from here? (19-08-2024)

Hi,

Here is a rough calculation of how the FY2027 numbers will look like taking management’s word. In my view, without accounting for write-back of provisions, the company can’t have anywhere close to Rs 4000 Cr PAT. Further, without considering substantial leverage (much higher than the 2x gearing the company is guiding for), 18% ROE from ongoing business cannot be generated.

Comments and critique invited

Excel Attached

Sammaan FY2027.xlsx (12.2 KB)

Oriental Carbon and Chemicals Ltd (19-08-2024)

Yes, the split percentage of cost will be as per the proportion provided by the company.

Prevest Denpro Limited (19-08-2024)

Pls have a look at the latest investor presentation.

TCI Express – Logistics Sector niche player (19-08-2024)

I believe the sales are somewhat tracking the number of branches. So according to management they have increased number of branches by 90% in 8 years and sales have grown by 70% percentage.

In the same period they have expanded their customer base by 70% which tells me that their average revenue per customer has remained flat which is part of the problem. It’s an industry wide phenomenon. Logistics is a very competitive sector with very limited pricing power for the existing players. Plus cost of operations has been edging up due to inflation (labor, transport etc).

So in such an industry, the ability of a company to deliver better returns to their shareholders will depend on market share expansion while reducing cost of delivery which will then flow into their operating margins and bottom line.

TCI Express management has continuously reiterated that they will be focused on both market share gain (through high quality services) and cost optimization (through automation). They are also exploring tactical opportunities for high margin businesses. Based on the results in the last 2 years, I am yet to see the upside from these actions but results haven’t been disappointing either. They have surely been outperforming many of their listed peers in the last few quarters of the sector slowdown.

I only wish that the management tempered their keenness to give guidance to the analysts which they can’t deliver on quarter after quarter.

All said, one thing I’m quite convinced on is that if there were any revival in the fortune of domestic logistics sector, TCI would be my top bet given their sound business model, healthy balance sheet and comfortable valuations.

Disc- Not invested but keenly tracking the stock and the sector for last 3-4 quarters.

P.E. Analytics Ltd (PROPEQUITY) – Another Data Analytics Platform for Real Estate Players (19-08-2024)

to peope who track prop equity closely, is there a seasonlity in the business of valuations? is q1 relatively weaker?

can use q1 update by comapny as a reference.

Disc- Invested

Akash Portfolio (19-08-2024)

I sold out quickly due to corporate governance issues.