Dear Akash, Have you exited from Edvenswa Enterprises…what factors triggered your exit from Edvenswa…

Posts in category Value Pickr

EFC – Entrepreneurial Facilitation Centre (19-08-2024)

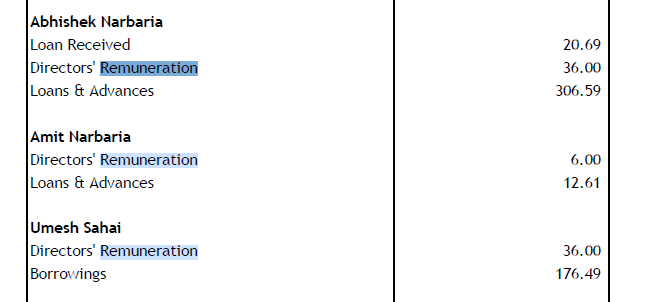

any body know what is this directors “Loans received” and loan and “advances”? apart from remuneration

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (19-08-2024)

please check praveg also, its better than kamat hotels.

its better in team, capex, margins and also in mcap 2000cr

kamat hotels has 500cr mcap only. it look risky and small, whereas praveg is bigger then kamat and in better condition rn.

Dilip Buildcon – The best-in-class execution! (19-08-2024)

Q1FY25 UPDATES

My subjective summary of the concall –

On the execution front challenges adding to debtors, mainly due to elections and lack of payment intent, should slowly pickup as govt intent payments will normalize

Target debt level 1000 cr shall be achieved soon, delayed a bit

Creating INVIT by end of FY , in touch with SEBI

Total prod of coal 7MT VS 5MT ( IN MILLIONS) , this year is 10 MT , EXPECTING 50% incremental production TO 15MT , on target to achieve full capacity in coal

DBL 2.0 , aim to achieve 0 net debt in next 2 years , slowly building towards that

Management Intent seems very high , to shape DBL into a large corp ( subjective biased analysis )

Should be able to reach guidance, have also gone into optic fiber participating in those tenders, hoping some positive flows into that business

HAM VS EPC (more aligned to EPC) 5-6K CR OF HAM (HYBRID ANNUITY)

2/3RD EPC IN ORDERBOOK

1/3RD in rest

Working capital situation improving after June, from here only looking at reduction of 1000 cr + levels till year end

Net Cash target by FY26

Full year finance cost between 350-400 cr , and on other income like dividends from INVIT units should be achieved

5500 cr revenue in next 3y to accrue in coal business, long term contracts (inflation adjusted) brings stability and adding to the painting of DBL 2.0

Management playing conservative on growth, which may lead to more positive H2 a case for positive surprise and mor info on the optical fibres as tenders are bid for , will be interesting to track the optical fibres segment in next 3 years

Tax rates around 33% for FY25 and FY26 , no change in depreciation rate , net block is reduced

Total capex for the year 150-170 cr ( 30 done in this quarter)

EBITDA this year conservative to 11-12% , longer term 12-14%

Opinion- ( biased and invested from 460 rupees price , please Take with hand of salt )

I think the transition of DBL as the management is showing strong intent to shape a structural transformation in the company is looking good , a base is seeming to be formed to create a runway of growth in next 4-5 years , only thing now is building a diversified order book in new sectors like water and optical fibres and strengthening the existing balance sheet by debt reduction and cost structures

Only major risk and thing to track remains the management execution and tracking finance costs as every quarter proceeds , and management in next two years needs to walk the talk , or might not create value for incremental shareholders

Hitesh portfolio (19-08-2024)

Dear @hitesh2710 ji,

Wondering if you have a view on IRM ENERGY. The stock hasn’t done well since its listing in Q4’23. The results have been kind of muted for the last two quarters, but the company is on a massive capex drive and plans to double its capacity by FY26. Also, they are in CGD business which kind of operates like a pseudo monopoly in my opinion (you have an exclusive right to operate in your geographical area for X number of years)…so to me that’s a big moat. From the VP thread I see some folks are concerned about the promoter not being minority shareholder friendly…and perhaps that’s the reason for not much interest in the stock. Would love to hear your views.

Thanks as always ![]()

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (19-08-2024)

On one hand I want to book my loss on this one, at the same time, the stock is at low valuations, more so after the recent fall. Technically also there is strong support at the current level. It might be worth waiting for the next quarter results but ofcourse these kind of shenanigans will limit any rerating potential even in case of good results.

Microcap momentum portfolio (19-08-2024)

Good morning sir you and @visuarchie sir both are doing fabulous job. If possible do share details of automation product, so people like me and others who are not technology expert can also invest in this strategy without making mistakes.

Thank you both of you

Hitesh portfolio (19-08-2024)

@hitesh2710

Usha martin broke the 200 dma and trading below that for the past few sessions. Technically, after the 200 DMA, where will the stocks find support. Whether there will be a consolidation, before moving up or something bad cooking up in Usha martin, that we don’t know.

Rategain – Fast Growing SaaS Leader (19-08-2024)

thanks for the headsup, will look into it soon.

Indiabulls Housing – A compounder from here? (19-08-2024)

Thanks for the detailed response. IMHO as well, legacy book issue must have been known by now for most part of it. There is no incentive for management to hide a big negative surprise until later.

As for FCCB, I think it was like 240rs. In one of previous con calls, MD mentioned that he is confident about foreign lenders converting them to equities. He put it as positive and they are confident in the business, etc etc. It was when the share was above 200rs. Lets see what happens. We will know soon.

I have not thought about leverage due to asset-light model. Don’t really know how much % percent co. will keep in its balance sheet for each of partner banks. But 1 lakh crore is indeed a decent growth number with 18% ROE.

Management ESOPs is a great motivator for sure. For all these troubles, none of senior management left the company. There must be some good incentives in play.

p.s: Invested.