Posts in category All News

High-dividend stocks: Coal India, ITC, Infosys, 8 more counters fit the bill (06-07-2024)

Bajaj Finance Limited (06-07-2024)

Sorry. I agree that book value may increase due to IPO proceeds. But business will decrease and so also profits, at least in the short term.

‘High real repo rate can have adverse effects on…’ (06-07-2024)

Why analysts are bullish about Godrej Properties (06-07-2024)

Tata Motors JLR wholesale rises 5% YoY in Q1 (06-07-2024)

Marksans Pharma- Can it be the next Pharma Biggie? (06-07-2024)

it will reflect from q1 onwards.

iam very bullish for FY26 as company said they will double US revenue from 800CR to 1600CR. so even if UK revenue grows @15% for next 2 years and adding up TEVA’s revenue target of 1000CR for FY26 then company may acheive upwards of 4000CR for FY26.

Five Star Business Finance – Financing Bharat! (06-07-2024)

Fedfina has a Mortgage AUM of roughly 6200 crores, ticket size of INR 22 lakh and yields of ~14%.

Five-star has an AUM of 9600 crores and almost 90% of the loans are sub INR 5 lakh with yields of 24%.

I presume the huge difference in yields is largely due to the nature of loans, wherein Five-star gives loans to small business owners.

However, my thought was that given the secured nature of the loans, their yields should have been much lower. At 24% yields, they are on par with microfinance companies, whose book is completely unsecured.

Infollion Research Services Ltd – Moated Microcap with Differentiated business? (06-07-2024)

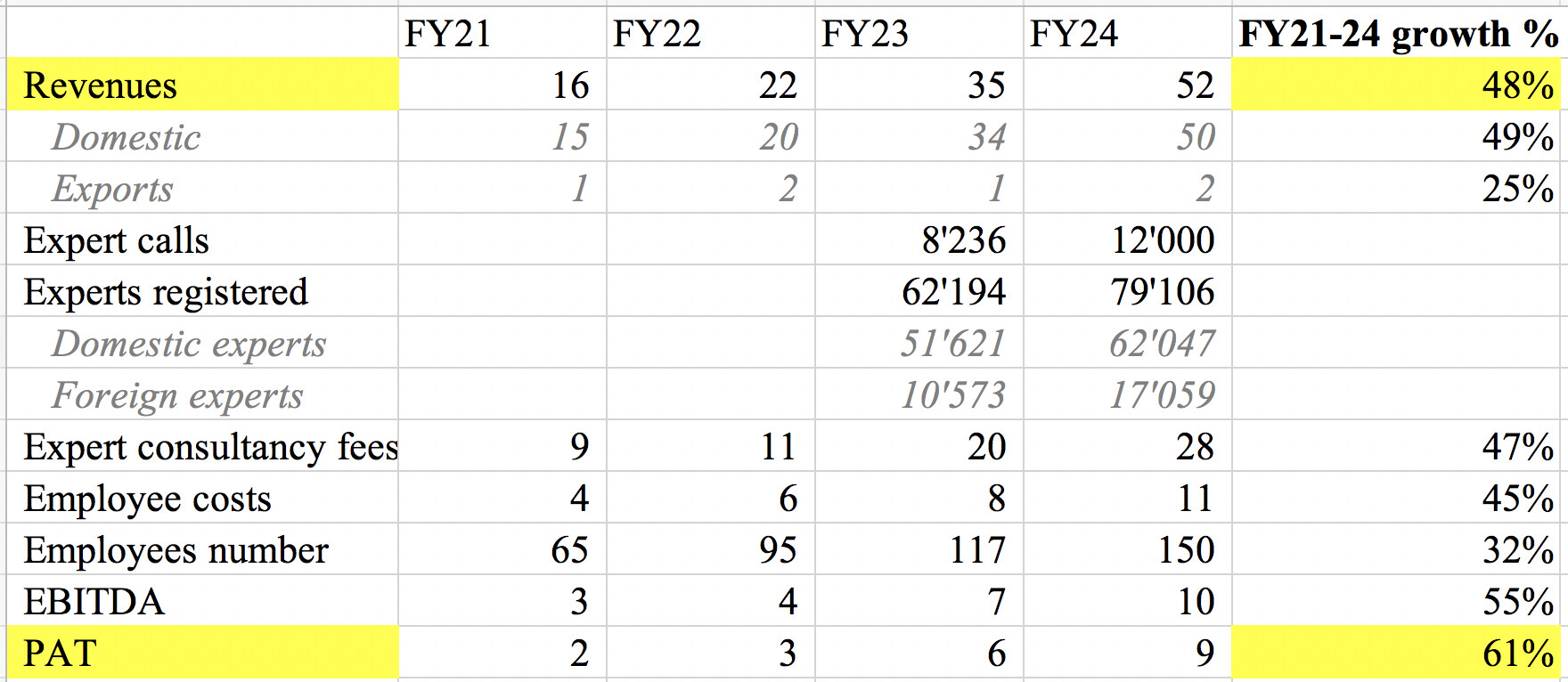

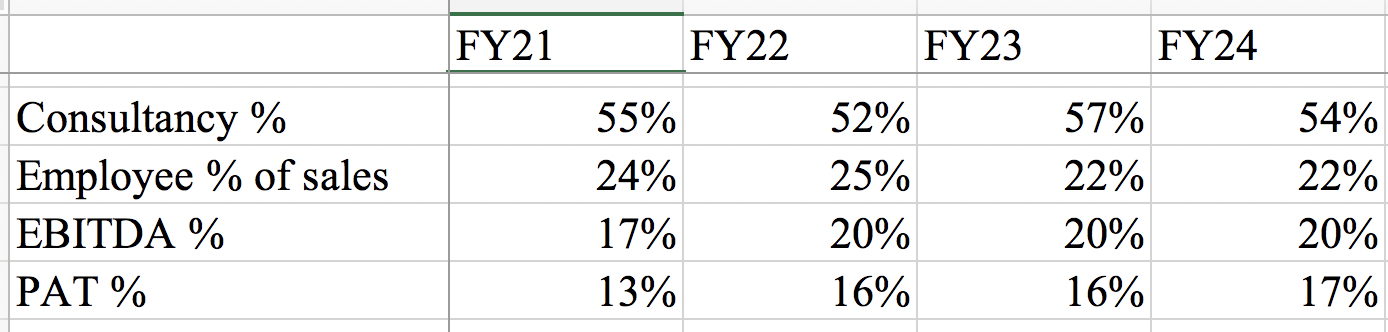

I was recently working on Infollion and found their business model quite niche with good unit economics and 40-50% CAGR growth.

Their margin structure has been stable. Their biggest cost item is consultancy (or expert calls), where they pay experts 50-55% of their revenues. They spend 20-25% on their employees and have been maintained 17-20% EBITDA margins over the past 4 years.

Additionally, there was an insightful note from Deltainvest explaining Infollion’s business model in detail. You can read the full note at the link below.

Writeup from Delta

- Incorporated in September 2009 by Gaurav Munjal (B.tech & M.tech IIT Mumbai)

- Marketplace in premium section of the gig economy, 100+ employees, 60,000 experts

- Does 400 projects/month

- IPO came at market cap of 80 cr. (IPO size ~21.45 cr., fresh issue ~18.2 cr., OFS ~3.2 cr. OFS was by Blume Ventures

- IPO done to expand business in USA & Western Europe

- Top 5 clients contribute ~80% of FY23 revenues (68% in FY22). 80-85% of their clients have been using their services for 5+ years

- Pre-Empaneled to Custom-Empaneled experts ratio: higher would imply higher gross margins

They have been scaling up their team as they keep growing, you can see how the number of employees have increased with time (scalup started happening from 2019).

- March 2017: 7

- March 2018: 6

- March 2019: 7

- March 2020: 11

- March 2021: 14

- March 2022: 35

- March 2023: 69

- March 2024: 90

They are now pivoting to the US, first to get more experts from USA and then to get customers from USA. Management has been sharing their scaleup plans at multiple avenues, I have captured these in my notes below.

AGM23

-

Adding 1000-1200 experts monthly, one-third experts are from outside India (primarily US)

-

Have a dedicated team for US

-

Most clients are Indian requesting experts from US, want to build a larger clientele in US

FY24Q2

-

Largest and oldest company in this segment in India

-

Majority business comes from consultancy businesses, targeting private equity and tier II consulting

-

Focus on engagements which are small, frequent and cross domain. Don’t engage experts with clients for longer term projects

-

Expanding into US

-

Competitors: Insights Alpha, Thirdbridge, GLG

-

Not keen on increasing gross margins but on increasing volumes

FY24Q4

-

6th or 7th year where sales growth was 40±10%

-

Added 50 employees which should benefit in FY25

-

Visual mapping tools of different industry value chains are becoming their USP now

-

Redesigned the entire tech backend which will help them expand globally

-

Expansion in US – 3 independent teams based in India (total 25-30 employees). Have been increasing expert base in US. However, most of their clients are still in India who are taking a call with an expert in US. Have not yet managed to get clients from USA

-

Trying to get into longer term engagements (Pex-panel): 2-3 months stints for existing clients offering private panels to senior executives, cohort-based/individual courses and L&D programs. Looking towards reselling expert-led courses online

-

FY24 calls: 12,000

-

Number of experts: 80,000 (adding 1,500 experts per month)

-

Client concentration: top 10 is 80-85% of revenues

-

Market size from Indian clients will be few 100 crores

-

90%+ of business comes from clients older than 2-3 years

-

Ticket size per call has not increased in last 2-3 years, don’t want to increase it, rather focus on increasing volumes

-

70-80% of their business comes from consulting industries, trying to penetrate deeper into private and public market investors

-

End-user industries: IT, Healthcare, consumer retail, BFSI

-

How they recruit experts: monitor annual reports for exits, monitor senior guys who are moving roles and get them onboard when they become independent

Disclosure: Invested (bought shares in last-30 days; <1% position size)