Posts in category All News

BSE (Bombay Stock Exchange)- Bet on Financialization? (01-07-2024)

Quick snap shot of BSE’s performance during the quarter(Q1 2025):

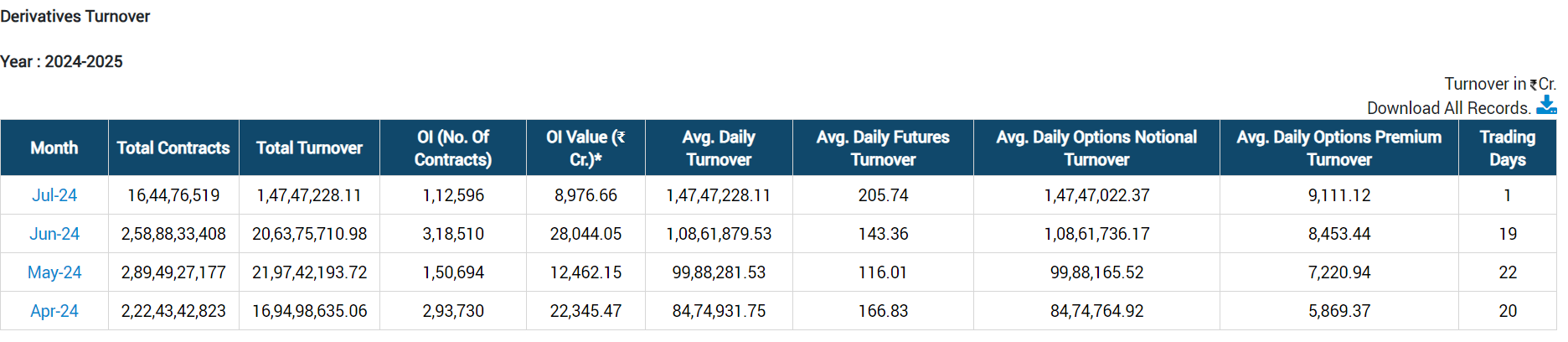

Derivatives:

The derivatives volume in general has been showing growth month over month during the current quarter - average daily premium turnover has moved steadily to above 8000 Crore during the month of June. The growth in premium turn over coupled with significant increase in price will lead to an exponential growth in revenue from this segment during the quarter. I expect the revenue from this segment to be at least 50% higher as compared to March quarter - the profit from the segment would be a positive surprise when the results are declared.

Star Mutual Fund: Robustness in growth continues with the total number of subscription and redemption orders showing a growth in excess of 25% and 40% respectively as compared to Q4 2024. Expect the segment revenue and profits to grow by at least 25% as compared to Q4 2024.

Cash Segment: The numbers seems to have slightly dipped as compared to Q4 2024. Expect the results to be slightly lower as compared to last quarter.

Currency and commodity markets are not showing any sign of improvement.

Overall, the results are expected to be blockbuster for Q1 2025. Looking forward to managements commentary on the new single stock futures product that is being introduced from July 1st.

AJ

Disclosure: Remain invested in BSE.

Nuvama Wealth Management: Proxy to Affluent India (01-07-2024)

Hey! Great questions let me try answering them

-

One major component is Loan advances. around 1300 crores is in loan advances. Remove that and it’s already positive. Secondly, If I am not wrong, You need to park cash as requirements in different segments of business. This goes under wc items. I would say compare this with 360 ONE WAM as these are the most similar. Also in the earning calls, you can notice analysts and promoters discussing dividend policy because they generate a lot of cash. Its not a point of worry(according to me)

-

Dividend policy is set to come by next quarter. they have mentioned that in their earnings call. However, the thing is Nuvama is investing and guiding for the Highest growth of all. they are aiming to double RMs in 3-5 years and AMC 5x in 4-5 years( low base so easy to do this but good growth rates) So honestly I would rather prefer cashing going into these growth engines rather than dividends.Personal opinion though so it won’t change anything and dividend policy will be announced soon.

-

NIMs is 5-5.2% in general but was 4.7% in Q4. Most of the loans are to existing clients and it is given on the collateral of the assets that their clients have under AUM of Nuvama so its 100% protected.

They haven’t commented on the gearing ratio, however 360 ONE said they are fine till 4x. That could give a potential idea -

Two answers to this. First, Nuvama aims to be a one stop solution so a client need not go anywhere. A promoters lists it business via Nuvama’s IB and then gives the proceeds as an HNI or UHNI for wealth management. When cash is needed, they use these assets against collateral and get that. Holistically, it’s a good model. even they mentioned they dont chase growth or anything but its an added service as a full circle kind of a thing

However, AMC and wealth management are the high ROE ones and the least cyclical of all. so they are aiming to focus on that and if you observe their share of profit has continuously increase and will continue doing so! their growth rates far exceed other segments

hope this helps, if you have doubts or if I got something wrong, let me know and I will try delving deeper.

Moreover, I am working on an article covering the wealth management space so I will cover these ideas in detail.

I will share the article here later for business analysis

Uttar Pradesh CM Yogi Adityanath slams Rahul Gandhi over ‘not Hindus’ remark (01-07-2024)

GST collection rises 8% to Rs 1.74 lakh cr in Jun (01-07-2024)

Microcap momentum portfolio (01-07-2024)

Thanks @visuarchie . Now my list is matching with yours