Margins of education segment of Q2FY25 looks lowest in last 8 quarters. Can someone help how to read this?

Margins of education segment of Q2FY25 looks lowest in last 8 quarters. Can someone help how to read this?

With the US filing civil and criminal charges against billionaire Gautam Adani and seven others over a multi-million-dollar bribery scheme, a prominent attorney here has said that the case could escalate significantly, potentially leading to arrest warrants and even extradition attempts. Adani, India’s second-richest man, and seven others, including his nephew Sagar Adani, have been charged by the US Department of Justice with paying bribes to unidentified officials of state governments in Andhra Pradesh and Odisha to buy expensive solar power, potentially earning more than $2 billion in profit over 20 years.

I tried to do DCF analysis for this company,

Please let me know what do you guys think!

Thanks

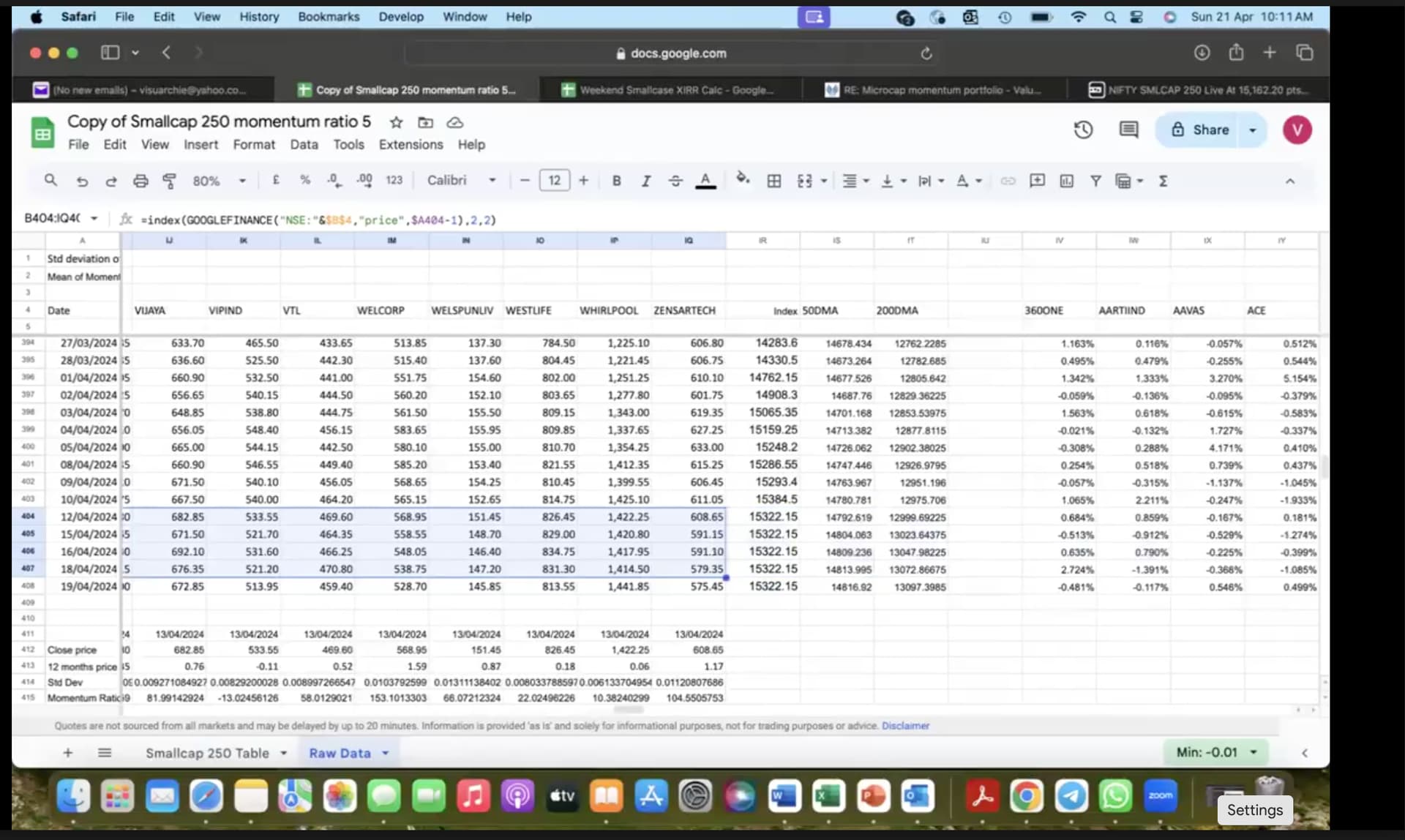

How do you retrieve daily index values? Is it a manual process? In the video, there didn’t appear to be a formula for the index column. Instead, it seems you simply extended the last week’s Friday value, as shown in the screenshot.

Also, can you take my update on this week (lookback dates 01/12/23 and 24/05/2024)

Based on Ranking:

Based on A → Z:

AMIORG*

AVALON*

BANCOINDIA*

CHOICEIN

GANESHHOUC

GRWRHITECH

IIFLSEC

INOXGREEN

KIRLPNU

MARKSANS

NAVA

NEULANDLAB

OPTIEMUS

ORCHPHARMA*

PGEL

PRUDENT

SANSERA

SHILPAMED

STAR

SUPRIYA

TIPSMUSIC

VMART

WABAG

WOCKPHARMA

ZENTEC

Exits: KESORAMIND and SARDAEN exit. GRAVITAS & LTFOOD stay within the top 30 and hence stay.

Entries: AMIORG & AVALON enter. ORCHPHARMA and BANCOINDIA cannot enter as there is no vacancy.

They gradually reached 10 Cr per month in sales, but you have to understand that it wasn’t at the start of FY. Think it more like 5+6+7+8+9+10 = 45 (Consolidated Numbers which they published)

Overall, while Mallcom has delivered fair (yoy) top-line growth in Q2 FY25, the decline in EBITDA margin has to be closely watched in coming quarters, although management tried to justify it as aggressive investments in branding, promotion, and expansions. Got to see how these translate into sustained revenue and margin improvements in next few quarters.

Few interesting developments are the launch of website new e-Commerce site that can now cater to both B2C and B2B orders/deliveries, along with revamped e-brochures – domestic and the export brochure (private label). I tried to order few products to my home town in Kerala and the delivery is within in 10 days and has all payment gateway options.

Also, seeing some increased number of expo participations and promotions of product launches in their multiple social media handles, like a recent one on ‘INFERNO’ – flame resistant work wear! Hope these efforts will turn to numbers in medium term. Below are few takeaways from latest Investor presentation and conference calls.

| Metric | Q2 FY25 (INR Mn) | YoY Growth | Margin (%) |

|---|---|---|---|

| Operating Revenue | 1,291 | 19.2% | N/A |

| Total Expenses | 1,133 | 22.0% | N/A |

| EBITDA | 158 | 3.0% | 12.24% |

| Depreciation | 23 | (23.3)% | N/A |

| Finance Cost | 101 | 10.0% | N/A |

| Other Income | 21 | N/A | N/A |

| Profit Before Tax (PBT) | 145 | 16.9% | N/A |

| Tax | 44 | 37.5% | N/A |

| Profit After Tax (PAT) | 101 | 9.8% | 7.82% |

| Diluted EPS (INR) | 16.19 | 10.4% | N/A |

Insights on Earnings Quality:

Management’s commentary suggests a confident outlook for the future, supported by strong demand in both domestic and international markets.

The company is actively investing in expansion, new product development, and branding to capture this demand and achieve its ambitious growth targets.

Management acknowledges the challenges posed by supply chain disruptions and rising costs, but remains committed to maintaining a healthy margin profile.

As usual Management tried to paint a picture poised for continued growth. The company’s focus on expanding its product portfolio, strengthening its distribution network, and capitalizing on emerging market opportunities positions it well for the future.

Disclaimer: Invested and Biased. Less than 3% of PF, No transactions in last 30 days. Post purely for study purposes. Consult your advisor before any investment decisions.

In the alpha SME presentation by the promoter, he said that 10 cr per month is possible and already achieved. Wonder why sales is just 40Cr instead of 60 Cr.

Supply of stock at higher rates is a major overhang, as i stated earlier, Samhi is a right candidate for takeover or merger. 230-250 can be achieved easily, we may see large block deals post that rate, let the events unfold in coming future.

Thanks for sharing this information.