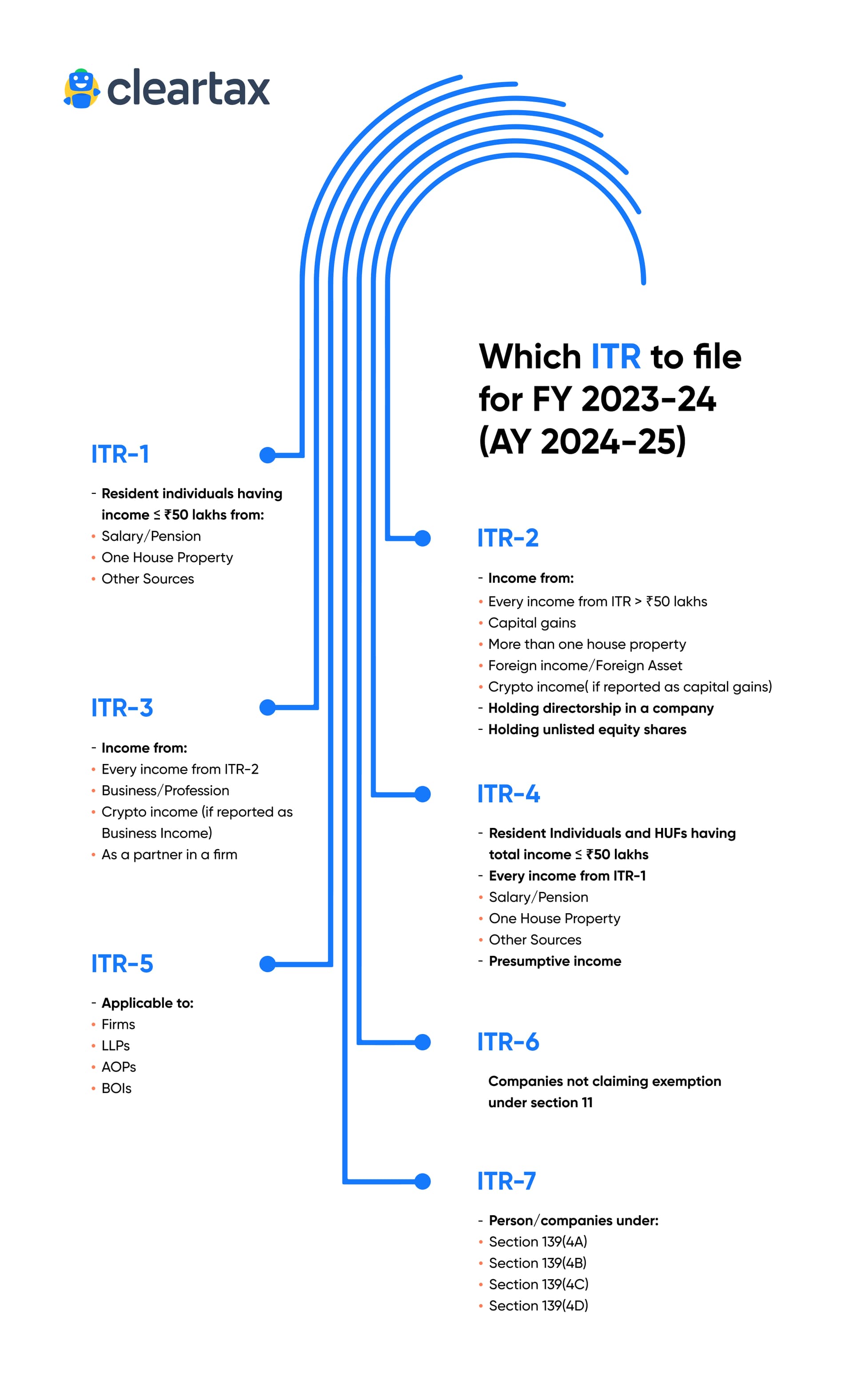

Tax filing season is on and this infographic beautifully captures all the different ITRs.

Source

Tax filing season is on and this infographic beautifully captures all the different ITRs.

Source

Thankyou for the pointers. I went through the details. I could not find why the promoters did not subscribe fully to the rights issue, but the pointers were really helpful to understand the business better. May be not a good business, but to develop and understanding, below are my assessments.

I no more hold this company but I am curious about understanding a business, their balance sheet, cash flow etc and this is now just one company that I am trying to understand as a part of my learning.

Krishca Strapping- a breakout after a long time, with strong volumes confirming the shift in the trend.

The new unit which is to sell higher margins straps is commercialized. They have doubled the capacity with this unit, taking the revenue potential to 300cr at peak utilisation. This yr they plan to do 40-50% utilisation, and will fully utilise it over 4yrs (although i expect it to be a lot earlier)

The peak revenue of 300cr, is excluding the packaging segment which can do a lot more then strapping segment once they get more approvals

They have also introduced another segment of products, primary packaging, which again is expected to be higher margin.

Have opened up their khaata with SAIL with 2 orders. Its very difficult to get into PSUs, SAIL has given them their smallest plant for now, SAIL has a lot many more plants, huge opportunity opens now.

Only 3 companies compete here, the new fourth one is krishca.

Mid East plan is still on, to setup a unit there, this can be very huge, as they will be the only one with a unit here and will be able to source rm from cheap asian countries, hence can compete even with china

Export sales is growing very rapidly, to do 30cr+ this yr and 100cr in the next 5yrs, i feel it can be done sooner.

Focusing on several new countries and already getting repeat orders, although smaller orders

The biggest risk here was a small TAM, but now they are getting into other prods (ofc a natural diversification and nothing else), these are higher margin then straps.

Also recently the company has given an intimation of a potential fund raise, which i assume will be used for this new expansion and the Mid East expansion.

there is detailed thread on this company, if needed

invested and biased