These vessels will have catamaran hull design and be built with aluminum and Fiber Reinforced Polymer or FRP. The hybrid electric propulsion systems will be powered by batteries as well as diesel generators. The hybrid system will offer greater flexibility to the operator to switch from one mode to the other as per requirement, allowing for greater safety. The use of batteries will reduce pollution substantially.

Posts in category All News

SME IPO: Sebi mulls doubling application size up to Rs 4 lakh, floats consultation paper (19-11-2024)

SME IPO: The Securities and exchange board of India (Sebi) on Tuesday released a consultation paper and sought public feedback on suggestions made by the stock exchanges and merchant bankers to increase the application size.

Agro Tech Foods – A small cap MNC foods FMCG (19-11-2024)

Del monte valuation seems to be at 2.3 price to sales( 550 crore sales, 1300 crore deal size )

ATFL valuation is around 2.5 sales considering 800 crore yearly revenue for last 3 years (approx)

Combined entity sales – 1300 crore. Price to sales of 2.3= 3200 crore and based on p/s 2.5 is 3500 crore rupees

combined entity Macap based on share issuance 2.4( existing share count) + 1.3(new share count)=3.7 crore share* 900= 3500 crore rupees. ( unless market decides to bring share price down )

So it seems like based on 2.3 to 2.5 p/s valuation is between 3200 to 3500 crore .

Any valuation below P/s of 2 should be a good opportunity ? As per ChatGPT fmcg companies valuations range between P/s of 2 to 11 from bad to great companies. So this seems like fair valuation ?( at this point , I don’t know earnings of delmonte so p/s seems like good ratio to consider for now )

Delmonte has come on share price of 975 rupees , and they are now 35 % shareholders of new company , so they make money only above 975.

Samara cap deal with agro tech was less than 1.5 sales ( really good deal)

I am still figuring out the details, any calculations above may have inaccuracies, happy to take feedback.

If anyone was able to get hold of management / have nuanced views, would be great to discuss

Disclosures- existing shareholder

Puneet

Annapurna Swadisht Ltd – A Swadisht FMCG investment? (19-11-2024)

Annapurna has posted great numbers.

The company can see astronomical* growth in the next 5 years if their execution matches their strategy.

*T&C applied, of course.

Larger balanced advantage funds remain low on equities, shows data (19-11-2024)

The equity market corrected substantially in October after logging gains for consecutive months. The Nifty 50 index ended the month down 6.2 per cent

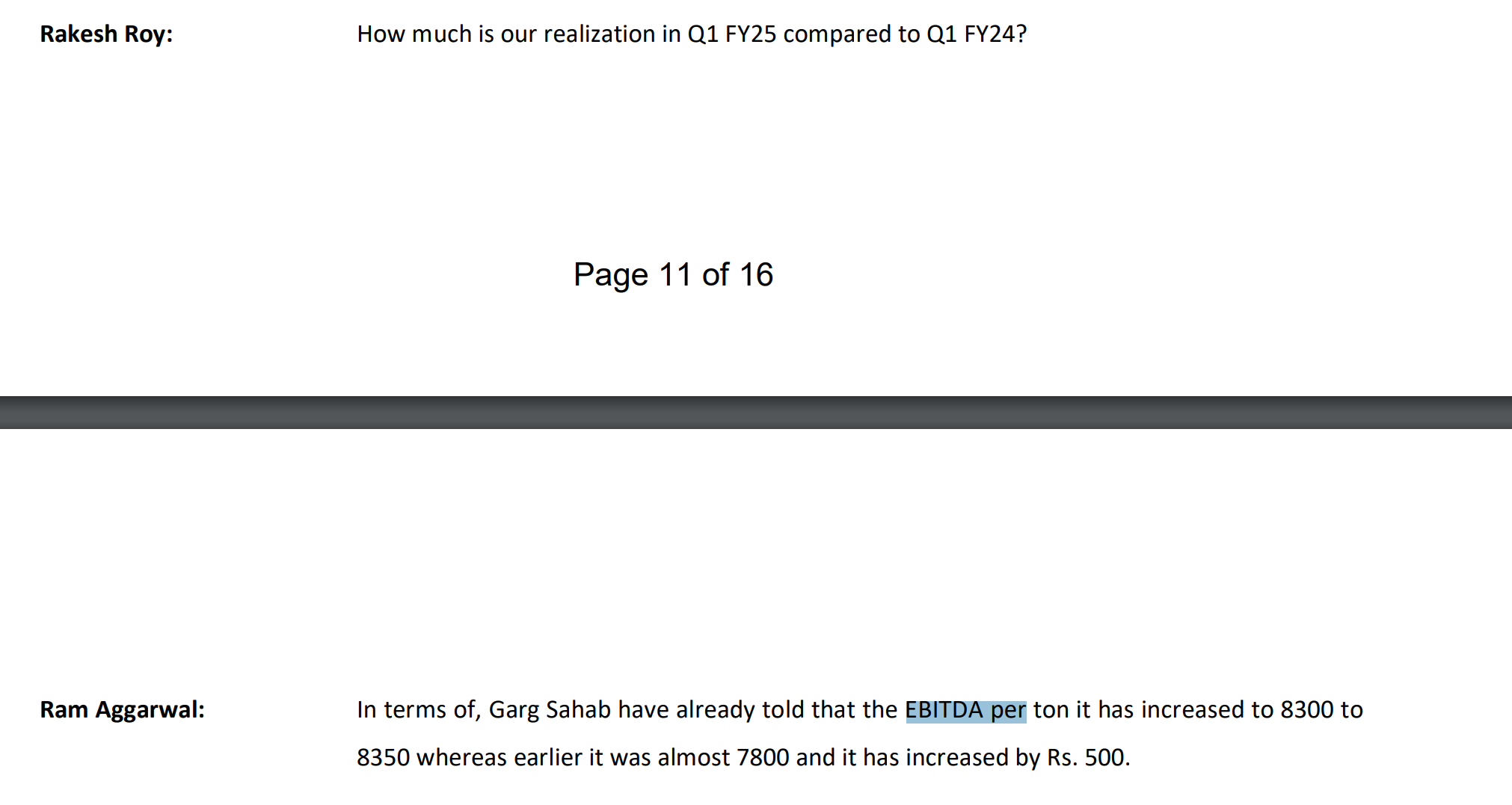

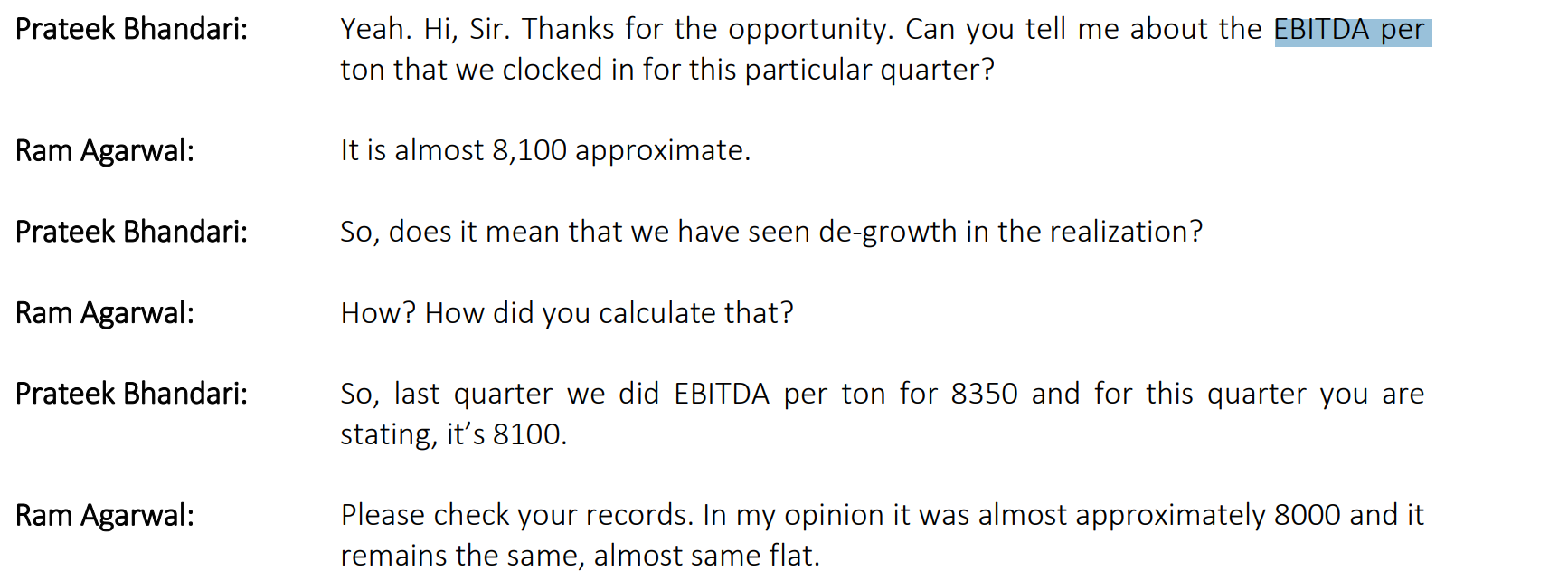

Goodluck India Ltd (19-11-2024)

One small doubt on ebitda per ton

Last Quarter management commented that the ebitda per ton is 8350 up from 7800. Kind of 500 per ton increase

When the same was asked in this quarter they are saying current quarter has 8100 per ton and his flat from previous quarter which is 8000 per ton

Any issue with this? As the both statements contradict each other

Glenmark – Will Innovation Pay? (19-11-2024)

Appreciate your updates on Glenmark.

But Glenmark hasn’t had much success in out licensing till date. I don’t think management calling their own asset as transformational or once in a lifetime in itself has as much significance. Although Ichnos has been discussed in every concall since a number of years, there hasn’t yet been anything concrete. Even if we agree that these things take time, if the assets were truly valuable, there could atleast have been some progress on raising money at Ichnos.

Views invited as to if/when Ichnos will actually amount to something.

Thanks.

These 8 stocks hit 52-week high, rallied up to 18% in a month (19-11-2024)

Eight BSE 500 stocks hit their 52-week highs, indicating strong performance. A 52-week high is a significant milestone, offering insights into a stock’s value and potential future performance.

Salzer Electronics (19-11-2024)

Some quick notes from the concall:

- H2 steady growth expected

- smart grid, IOT devices, customised switch gears are growing

- smart grid requires advanced switch gear fuelling demand

- First order of 5cr for smart meters. Small step forward.

- 200cr worth of order which was earlier expected within smart meters this year does not look like a possibility this year. Next year confident for 700 cr though.

- Targeting margin of 11% by FY 26.

- DC fast charging and smart meters in the future to add significantly in the coming years.

- Other income includes shares of KC industry sold partly considering good valuation. Still holding 70% of the business.

- Expecting 12% margins for smart meters

- FY 26 Guidance – 1600 cr rev from switch gear, wire and cable and building. Plus 700 cr from smart meters with a blended margin of 11%.

- Fy 25 – 20 – 23% growth.

- Smart meter capacity is of 1000cr looking at the market 700 cr looks like realistic revenue target for next year.

- AMSPs have built big order books but the second line order from AMSPs to players like us is still in process.

- Building segment negative EBITDA for the qtr.

- capacity for set up for 100 chargers a month.

- total transformer business approx 250 / 300 cr. We are not into ditribution transformer. Low voltage segment. 690 V max. Application: building, equipments etc. Growth is good as It grew 30% plus.

If they meet their guidance of 2300 cr with 11% margin as per my rough calculation they can do about 125/130 cr of PAT which is about 14 times forward. Let’s see if the management can walk the talk.

Market regulator Sebi notifies pro-rata distribution norms for AIFs (19-11-2024)

AIFs are niche investment vehicles for affluent investors with high entry barriers. These investments are drawn and deployed in tranches based on the investment opportunity