Audio recording of Q2 Concall:

Shree Ganesh Remedies Ltd. | Q2FY25 | Earnings Conference Call | #earningcall #concall #shreeganesh

Audio recording of Q2 Concall:

Shree Ganesh Remedies Ltd. | Q2FY25 | Earnings Conference Call | #earningcall #concall #shreeganesh

These look for the sugar division mostly… you can see the significant bump in sugar division assets in Q2 vs Q1

Hmm

That’s interesting Abhay.

The rationale behind my thesis is based on the guidance given by the management.

What I have observed from reading past 3-4years con calls and watching multiple interviews of the management is that they are quite conservative whenever they give any future guidance.

They have been saying since past year that Industry can become 12-15k crores in next 3-4 years so I get my numbers of sales and PAT from there.

Also I feel the growth rates and PAT margins that you have used in your model is too conservative.

Provided the growth potential the whole industry has.

But I feel that’s what makes investing interesting every investor has/her own opinions.

Lets see wait and watch what happens with TIPS in the coming years.

I am fully invested though and will keep adding till on dips till the momentum in the stock continues.

Yatharth is trading at comforting valuations. Given significant growth opportunities in local market & its pledge to increase revenue without sacrificing return ratios, there's a clear sign that gap in valuation from peers is likely to wane. TP ₹790 (30%)

Yatharth is trading at comforting valuations. Buy for TP ₹790 (30%)

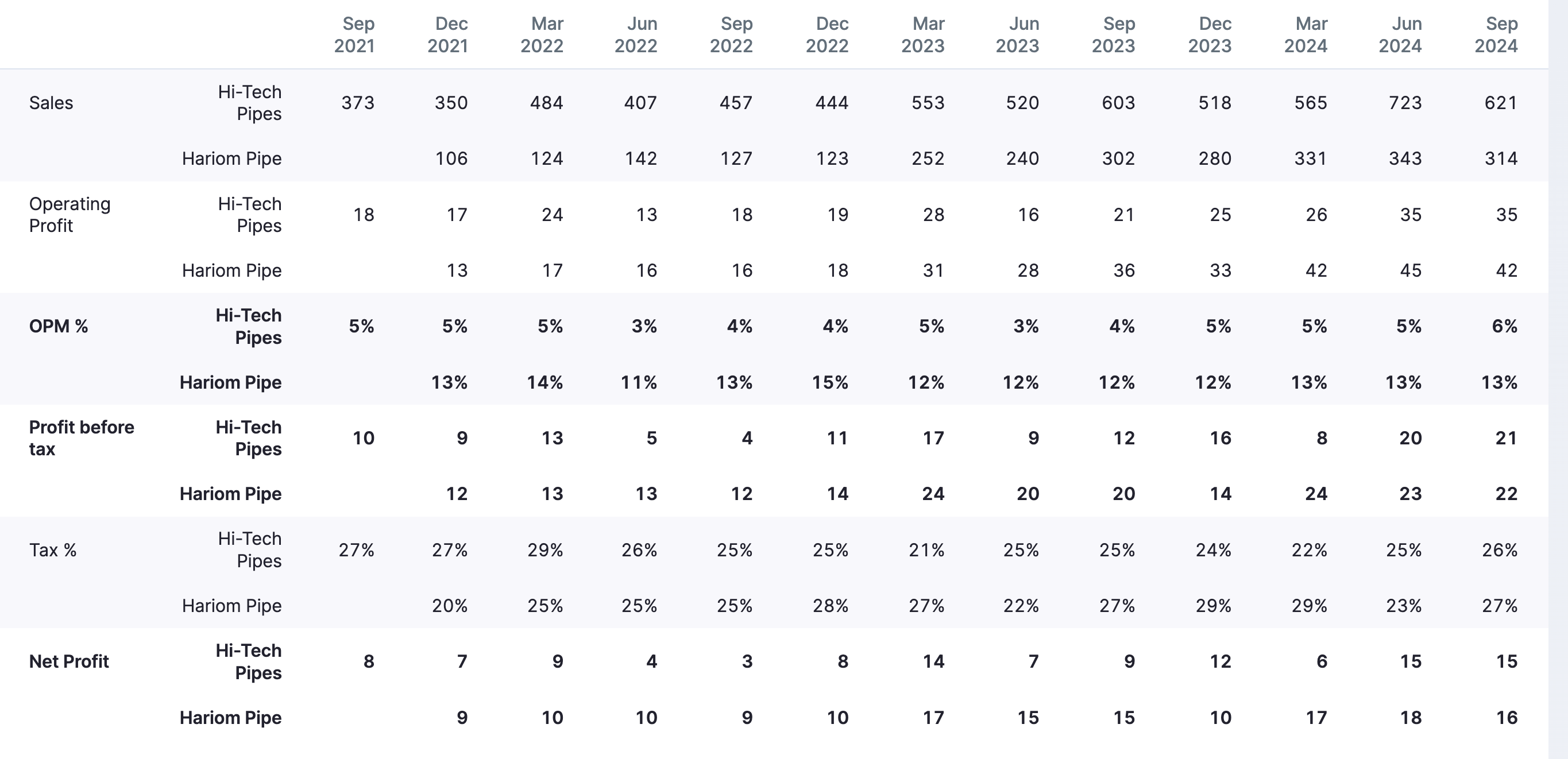

Any idea why Hi Tech pipes has a higher valuation multiple v/s Hariom despite Hariom having slightly levels of absolute PAT/EBITDA ? DII+FII ownership in Hitech is ~30% vs 10% for Hariom.

Here comes another player, where founders have fire for growth in belly and wallet support from

Some fiscal hawks worry that Trump’s policies would increase the deficit and fuel inflation.

In Pune, Union Minister Kiren Rijiju criticized Congress leader Rahul Gandhi, calling him “immature” and accusing him of undermining India abroad. Rijiju asserted that the BJP-led Mahayuti alliance would secure victory in the upcoming Maharashtra polls, dismissing the Congress-led opposition’s claims as “fake narratives.

Dahnuka Agritech –

Q2 FY 25 results and concall highlights –

Revenues – 654 vs 618 cr, up 6 pc

Gross Margins @ 42 vs 40 pc

EBITDA – 160 vs 142 cr, up 12 pc ( margins @ 24.3 vs 22.9 pc )

PAT – 118 vs 102 cr, up 16 pc

Guidance for FY 25 – revenue growth of aprox 15-16 pc over FY 24. EBITDA margin improvement of 100 bps ( 1 pc ) over FY 24. Earlier they had guided for a 20 pc topline growth for FY 25 – basically have made a downward revision to their projections

Continuous / Excess rainfall in Aug/Sep resulted in farmers skipping sprays in many crops ( specially insecticides ). Sales return from Q1 also had an adverse effect on the topline growth

There was a continued pricing pressure on product prices ( to the tune of 4-5 pc ) resulting in lower topline growth

Three of company’s newly launched products – Purge ( Japanese herbicide for Groundnut and Soybean ), Lanevo ( insecticide for horticulture crops ) and Myco Super ( biologic – for soil health ) – are doing exceedingly well in the marketplace and exceeding even the company’s expectations. Both Purge and Lanevo are in-licensed from Nissan ( Japan )

Product wise sales breakup in Q2 –

Insecticides – 43 pc

Fungicides – 21 pc

Herbicides – 17 pc

Others – 19 pc

Region wise sales breakup in Q2 –

North – 29 pc

South – 31 pc

East – 12 pc

West – 28 pc

The patented products ( that the company in-licesnces ) from Innovators – contribute to aprox 600 cr of company’s topline at present. Have tie-ups with 10 leading agrochemical companies across the world in order to tap into in-licensing opportunities

Company is currently serving aprox 1 cr farmers through a network of 41 warehouses, 6500 distributors, 80k + retailers

High water levels in reservoirs should support a strong Rabi season this FY – augurs well for the company

Company did not share their launch pipeline for next FY

Company new AI plant at Dahej generated revenues of Rs 8 cr in Q2. Did operate at negative EBITDA levels { aprox (-) 4 cr }

Sales return in Q2 were due to late onset of monsoons and excessive rains. Sales returns were aprox – 100 cr, mostly in the herbicides category ( general levels of sales returns in Q2 are around 50-60 cr )

Volume growth for Q2 was 10 pc. Price growth was (-) 4 pc

Not expecting any significant sales returns in Q3

High inventory build up at the end of Q2 is also due to increased sales returns. Company expects the same to normalise by end of FY 25

Company has been able to hold onto and improve their gross margins is because of good / great performance from their in-licensed speciality portfolio. Price erosion in generic products has been much higher

Zanet ( another in-licensed product launched LY – fungicide used on Potato, Tomato crops ) is also doing very well

All 4 products – Zanet, Lanevo, Myco Super and Purge are exclusively with Dhanuka. The same is likely to continue for medium term

At present – company derives 33 pc of its revenues from In-Licensed products

Company makes 10-15 pc extra gross margins on these exclusive – inlicensed products. Generally, company starts with 3-5 yrs exclusivity agreements with the innovators. The same is extendable after that

Looking for Contract manufacturing opportunities from the Dahej plant. Nothing has fructified as of now. Aim to do a 250 cr revenues from the Dahej plant by end of FY 27

Other big brands from company’s stable include – Targa Super ( herbicide ), Caldan ( insecticide ), Sempra ( herbicide ), Mortar ( insecticide ) and Decide ( insecticide ). However, the company did not specify these product’s annual sales except that Targa is the only > 100 cr brand among these. Others have the potential to reach that milestone in medium term

Should start to break even from Dahej once revenues from the facility cross 150 cr

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation

Karnataka Chief Minister Siddaramaiah has accused Prime Minister Narendra Modi of showing favoritism towards Gujarat by diverting major investments from states like Karnataka. He criticized Karnataka’s BJP MPs for not challenging this alleged bias and called for fairness and equal opportunities for all southern states.