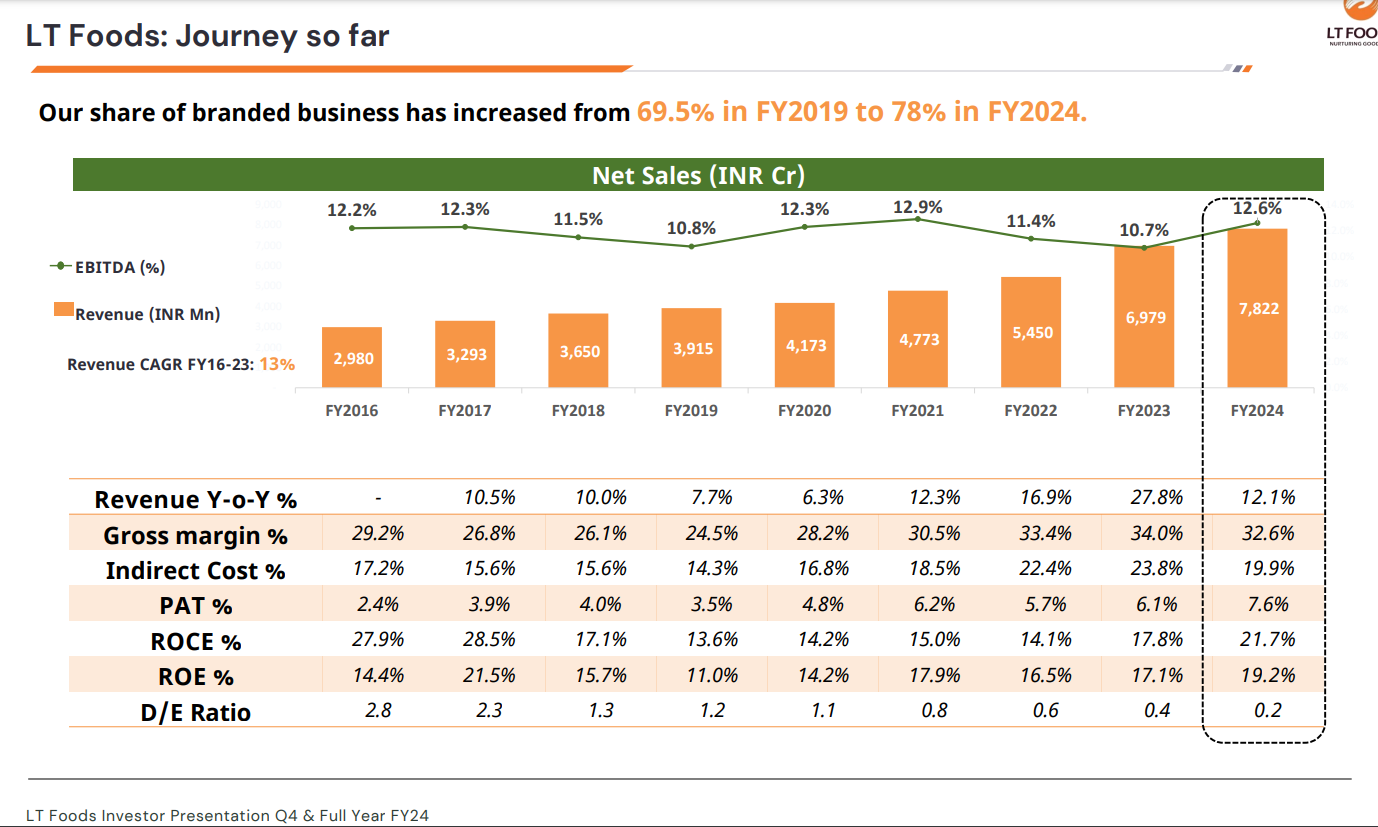

LT foods has doubled revenues in the last 5 years. They have a double engine for domestic growth: (1) increasing GDP per capita will increase overall rice consumption per capita, plus (2) as disposable income increases, more people will buy basmati rice, which is seen as a premium rice product in most of the country. Richer consumers will also chose premium / trusted brands like Daawat / Royal. Hence, if LT Foods retains its market share and “premium” branding, they should grow faster than Indian GDP growth. Exports will be the cherry on top, with increasing Indian diaspora abroad and also Indian food gaining popularity with foreigners.

So, I see a good runway ahead of growth between 8%~12%. But f you’re expecting 20%+ growth, this is probably the wrong company to invest in.

Thanks,

Sharad

OpenSourceInvestor @ Substack