Bharat Rasayan Ltd

Disclosure: Not Invested

CMP Rs 987 (11 Dec 2015), MCap Rs 426 crore

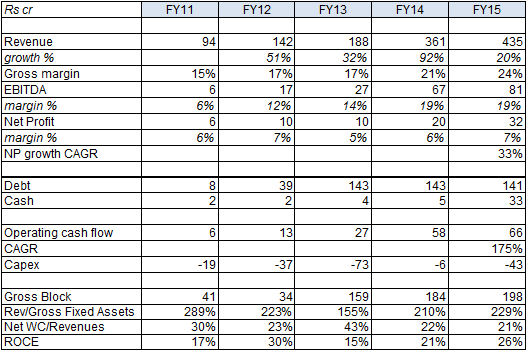

FY15 Debt Rs 141 crore, of which 52% is working capital debt. Equity Rs 113 crore

Cash and bank balance Rs 33 crore.

Book Value Rs 266

Face value Rs 10

Promoter holding 75%, has been stable for past five quarters. Remaining held by retail and others. No shares are pledged.

Highlight of the company has been steadily improving financial performance. This has been driven by an increase in Gross Block as well as improving gross margins. The company has added significant economic value by growing while generating increasing ROCE.

About 25% of revenue comes from exports. The company has no forex debt. Raw material is the largest cost component comprising 69% of total costs. Thus fixed cost component is low at 10%.

Effective tax rate has been 33-34%. Dividend payout ratio used to be 10-15% but has dropped sharply to almost nil in last two years.

The company is rated AA-/A1+ by CARE Ratings. Market has rewarded the company by increasing both PBV and PE ratio, the latter increasing from 6.1 times in FY13. However, it seems the strong cash flows and future growth is still not priced in the stock (PE of 13 times), which trades cheap compared to its historical EBITDA growth.

Later posts will focus on company’s products and quarterly analysis.

To be continued…

| Subscribe To Our Free Newsletter |