Hi Aditya, i agree with your analysis.

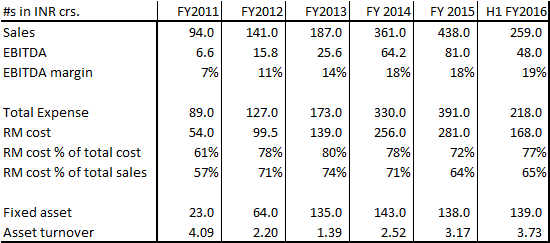

Factsheet –

Takeaways –

Sales have almost grown ~5 times over last 5 years in line with capacity expansion. There is no capex pending to come on stream now.

EBIDTA margins have also doubled. RM cost as % of total sales have declined by 6%

Probable reasons –

a. Am not sure of what are key raw materials for TCP manufacturer and how its prices have fared over last 5 years…Please help with this input if someone can

b. It might be due to increased efficiency of new plant at Dahej , asset turns have increased –> leading to improved margins

c. Also increasing share of exports might be key for EBITDA margins to double

Key open points –

a. What is key raw material (RM) for TCP manufacturer? How are the prices of this RM moving over last 5 years?

b. TCP plants generally operate at 50%-60% utilization levels – what is peak estimate of sales from current installed capacity?

| Subscribe To Our Free Newsletter |