I have recently come accross a stock named Spenta International which is a textile stock operating on a relatively niche area like Socks. Below are the analysis I have made.

Sales Growth :-

As we can see the company is

making a sales growth CAGR of 16% over last 10 years hence this is a

commendable job and mostly inline with management expectation of making 20% CAGR

for coming 2-3 years but the considering individual years the growth they are

mostly fluctuating which is a cause of concern from strategic point of view of

the management.

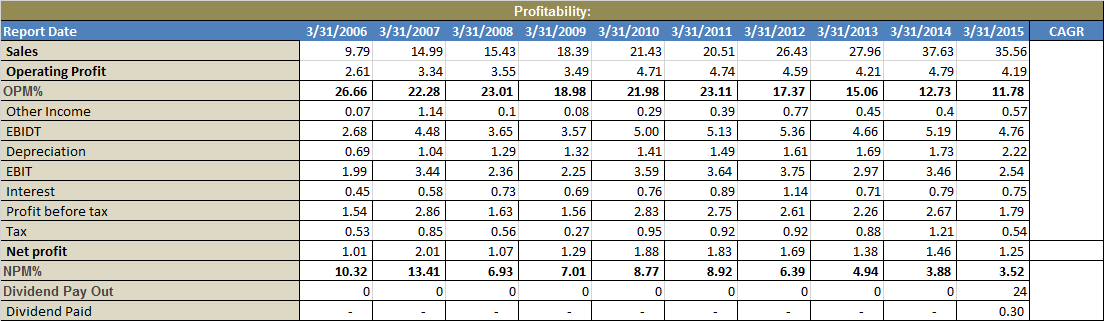

Profit Margin :-

The profit margin both OPM and NPM

is not very satisfactory and mainly on the decreasing side hence it will

clearly show they do not have a bargaining power over it’s consumer. Though

they have recently felt the urgency to create their own brand and increasing

export hence this might be a good step in increasing the Profit Margin but only

time will tell.

Value Creation :-

Over the years it is not well

known for creating any value for the share holder but this year it really does

it also from above you can see they have started to giving dividend so the

focus has changed and could have been a very good value investment opportunity.

Tax Payment :-

Tax payment is at per with corporate

tax [30-34%]rate hence not a problem with that but there is a ongoing dispute

with the IT of 48Laks.

Interest Coverage :-

Interest coverage is 5-6% always

hence a very good cover they have on their debt.

Debt :-

Debt is mostly very low and they

have have significantly reduce it in last three years also DE ration is under

control of 0.14-0.16 level.

Current Ratio :-

Current ratio is good hence we can

conclude there is ample amount of liquidity in the business.

Cash Flow :-

Cash flow is really good which is a

commendable job by the management and show there conservative mentality also

collection of cash remain stable and consistent.

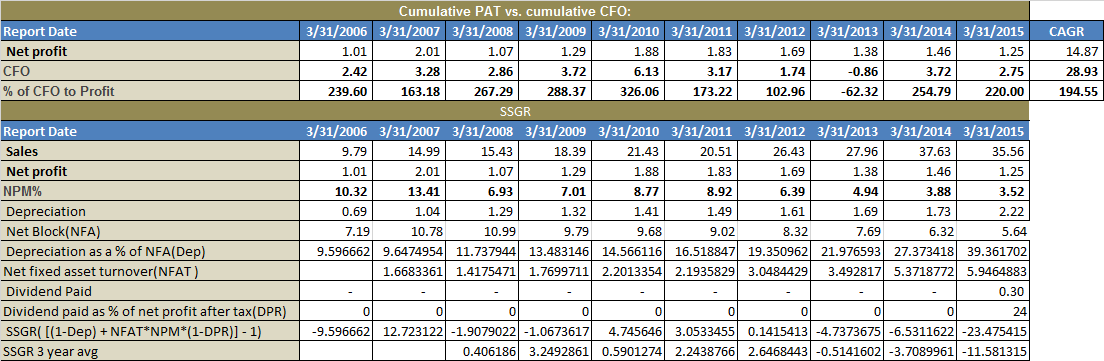

Self Sustainable Growth Rate :-

This is the parameter by which we

can judge weather a company is able to survive in future from it’s internal

operation without a much requirement of cash inflow into the business.

Generally an average of 30-40% SSGR is good and stable.

The company does not have a good

track record of SSGR and mostly on the -ve side hence the future capital

requirement for the company is on the card if they will plan for expansion. As

we have earlier discussed that margin has suffered for the company so this is a

prime reason for -ve SSGR coupled with high depreciation rate of it’s asset

which means they are in a requirement of continuous replacement of their

asset and also they have started paying dividend from this year which is

a good sign for the shareholder but will cost the business. So if the company

wants expand capacity or global footprint they will be requiring cash inflow

outside of their internal business operation though the CFO and free cash flow

is good and the company have ample cash in hand but this will again affect the

Dividend payout plan of the company. So the way I see it if they will be able

to increase Profit Margin this ratio will automatically improve and might not

be a cause of concern.

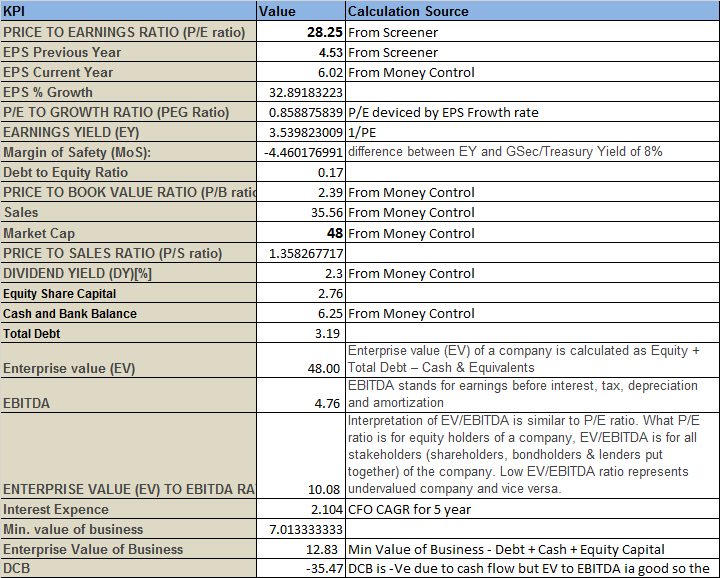

Valuation :-

Before taking an investment decision

we have to check couple of point :-

-

PE is at 28 hence on the higher

side and we have no margin of safety. -

PEG stands at 0.9 i.e. under one

which shows there is a ample amount of growth left as the market cap is only

48Cr. -

PB ratio is at 2.8 and PS ratio

is at 1.3 which are really good investment rationale. -

EV to EBITDA ratio is at 10.8

hence a good bargain. -

DCB is -ve and mainly due to same

reason for SSGR though here we are interested in CFO instead of PAT but as the

company is good at collecting cash so both are having the same explanation. We

have to have a Hawk eye on NPM and Sales CAGR.

Any help in this stock will be very helpful for me as I am relatively new in this domain. So if anybody has any information please share your view in this stock.

many thanks,

Krishnendu

| Subscribe To Our Free Newsletter |