Concall Recording:

Important points from the ConCall:

- Q1 is seasonally weak quarter/ One client business portion (not fully) let go because of pricing pressure from competition-which is unsustainable, same client other area business (WhatsApp??) own/retained – This has around 3% margin impact, other one offs are – Infra upgrade -1% impact + currency fluctuation – 1% impact.

- No guidance but confident that Margins to get back to 20% in the next two quarters Q2/Q3.

- Most important point in the call – around 45 billion/month Cpaas transactions happening in India, including Government, Tanla only handling 2 billion/month, so Hugh market available for growth in India Itself. Imagine global opportunity.

- VI – wisely integration mostly done, another couple of weeks to complete. TrueCaller started also going smoothly. Both VI & TrueCaller own based on better product not on pricing, wisely is costly, but everything on one platform.

- Platform Wisely revenue will be step by step, slow and steadily it will grow in the next 4 to 6 quarters, very happy and confident how its progressing. Tanla is in no hurry.

Please consider some points I might have misunderstood or missed add if any.

Comments: Market reaction is obviously based on their past, surely over reacting, Industry itself growing by 25-30%, massive disruption, unless management goof up, massive opportunity lies a head, with nearly 1000 cr cash on Balance sheet, EV value @ Billion dollar now, let’s c how route mobile results will be, bullish on Cpaas industry.

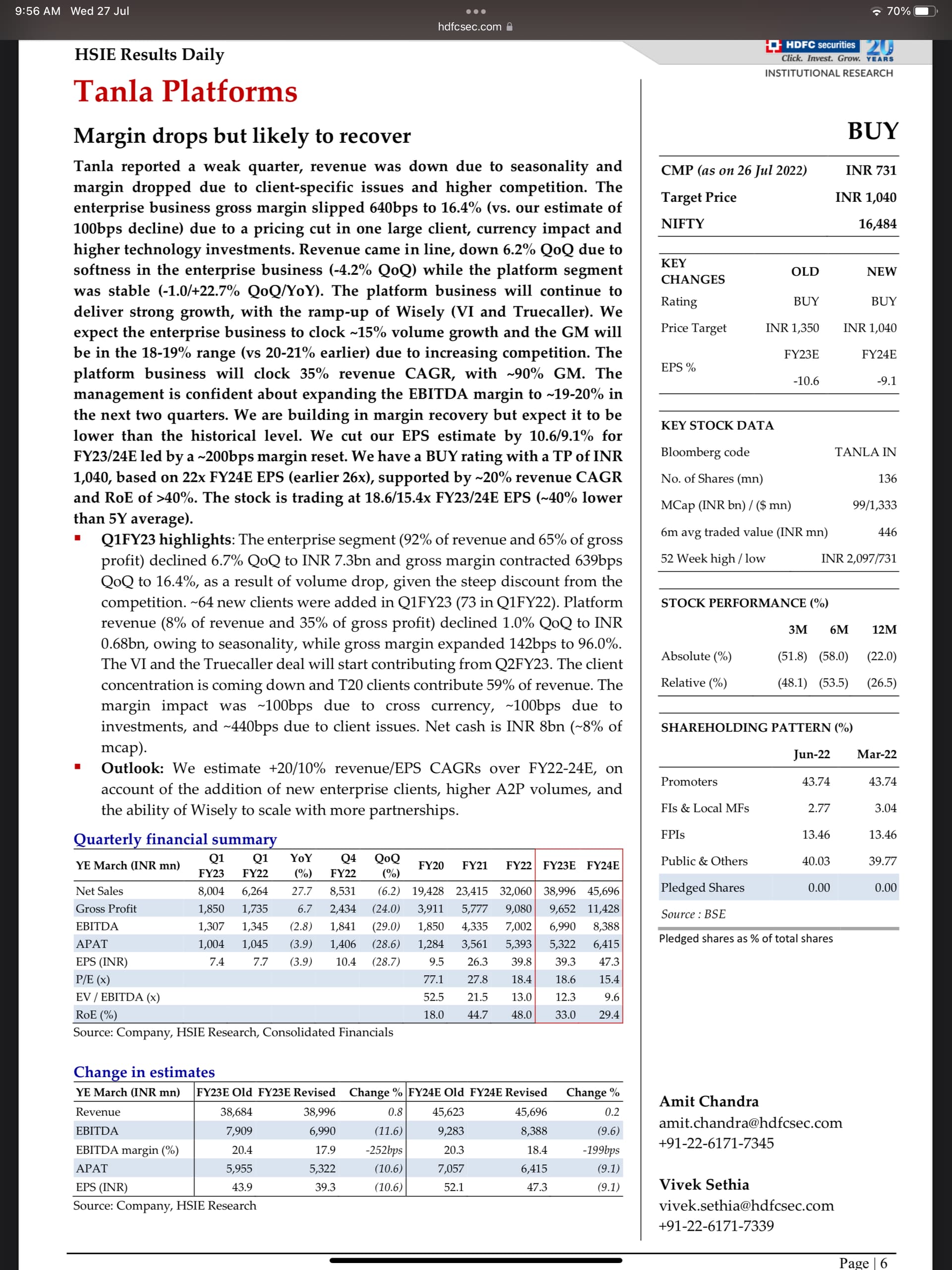

HDFC sec q1 update:

Disclosure: Invested.

| Subscribe To Our Free Newsletter |