BOOM. Intel posts the worst results in near term memory. Reported loss.

Both client and datacenter down. Degrowth was expected but not this much. Client was a surprise for me. Not sure what is going on there.

Since our focus is datacenter, we knew intel is going to lose market share. The real news is that Saphire rapids are delayed in 2023. Some SKUs are ramping up in 2023. All the while, the message was that ramp up is late 2022. But we get to know now that some SKUs are later. Analysts had to grill the company in analyst call (https://edge.media-server.com/mmc/p/6zdpcntm) to get that out. All guidance now changes or the year t 2.3$ EPS.

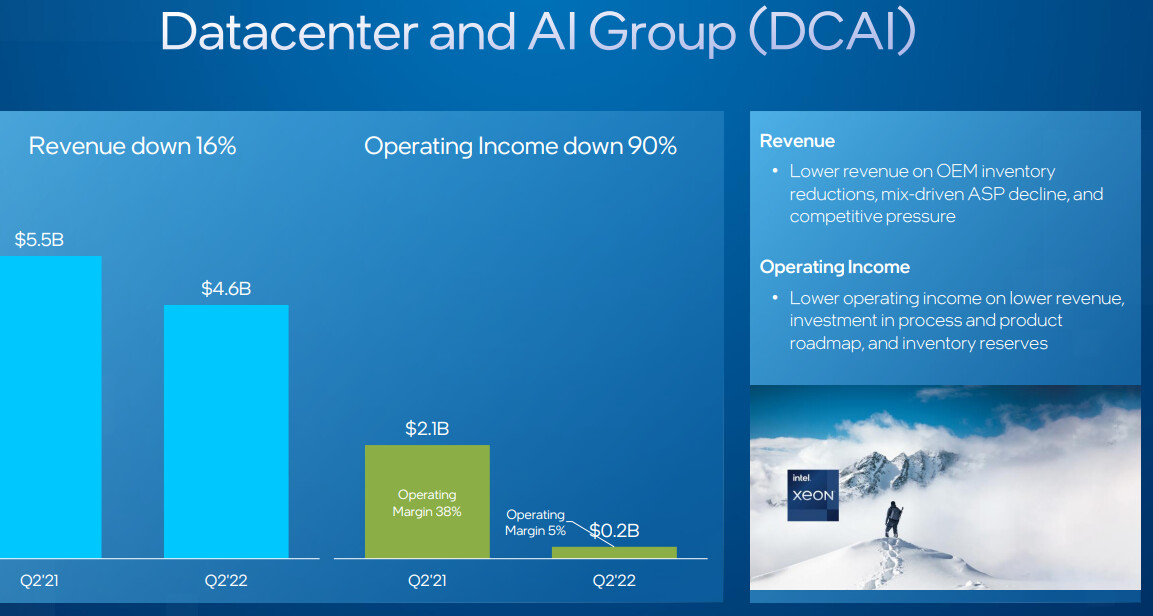

I have not seen 5% operating margin before. Need to review some old financials.

| Subscribe To Our Free Newsletter |