Company continues to impress on all fronts. As discussed by some investors above, we will start seeing the impact of export duties and resultant lower realisations from Q2FY23 because of the lag effect. Good to see they are focusing on sponge iron and other products to try and maintain good margins. Kudos to @Kumar_manas for being right about this all along. Seems fair to assume this will cushion the margin hit a lot of people were expecting next quarter to a significant extent as even though prices of pellets have corrected quite a bit, prices of sponge iron and billets are actually trading higher than they were before the export duties.

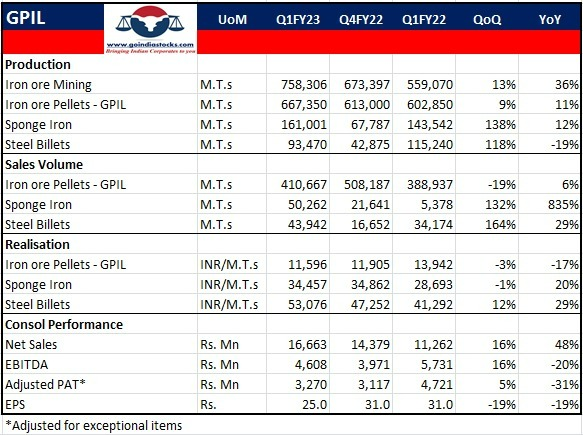

Credits to Go India Stocks for the following image that summaries the performance.

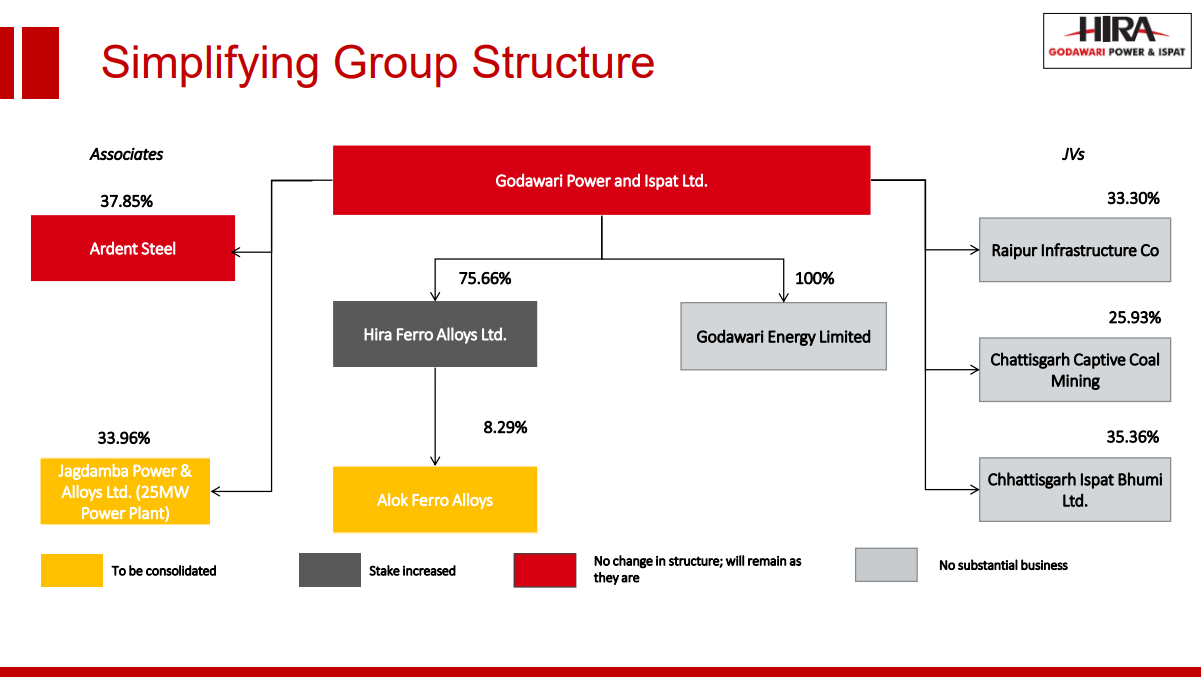

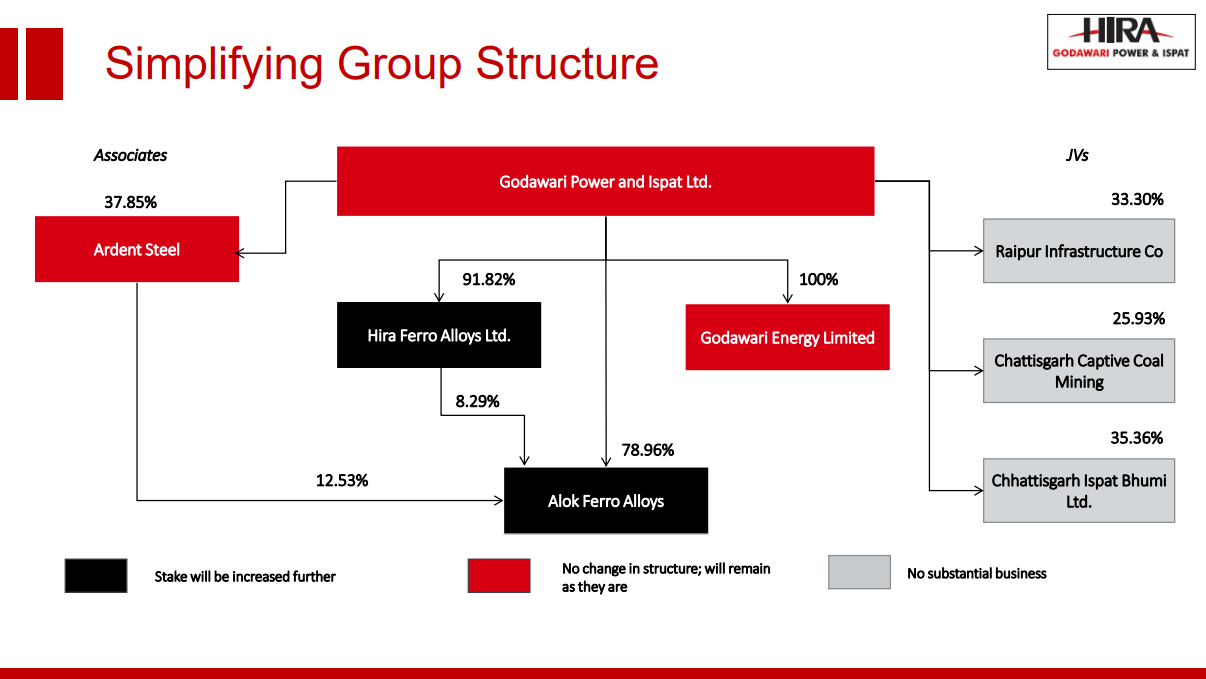

Group structure being simplified:

- Management have guided they will eventually make both HFAL and AFAL wholly owned subsidiaries.

- Acquired the 25MW Jagdamba Power Plant on slump sale basis and surrendered shares in buyback launchd by the company so that they qualify as captive producers.

Q4FY22:

Q1F23:

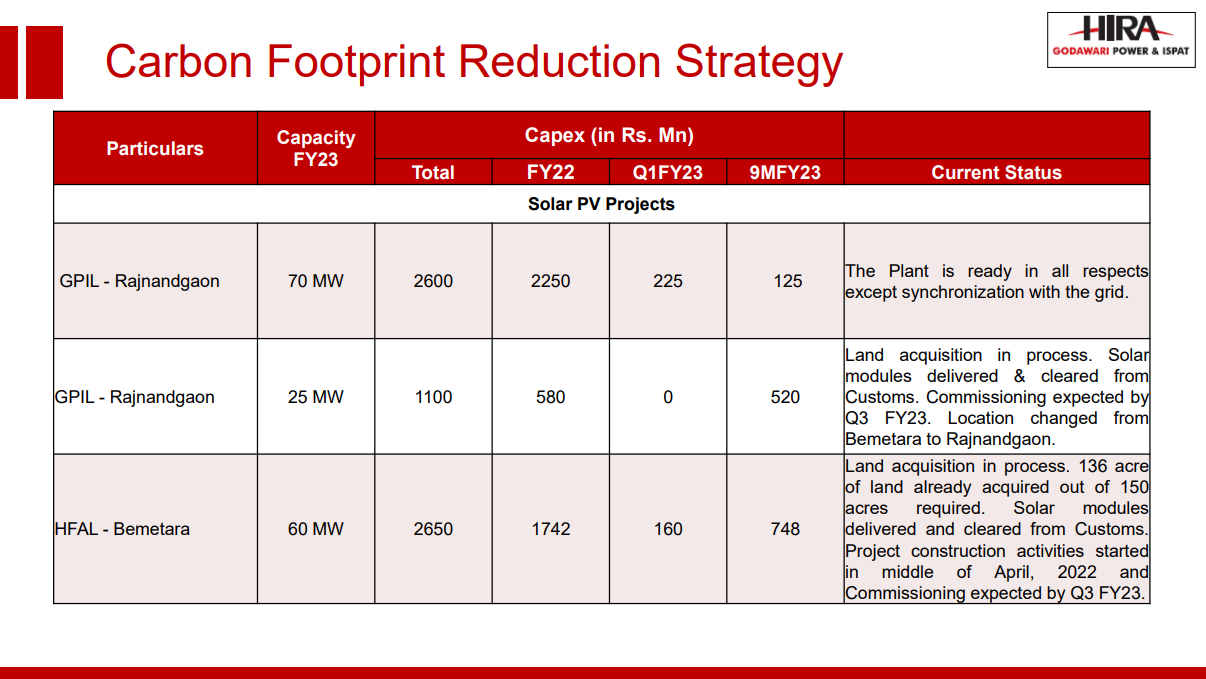

Solar Plants + Carbon Footprint Reduction + Power Cost Savings:

- Confident they will commission all solar plants – total of 155MW – within FY23.

- Once solar plants go live, existing capacities will have achieved carbon neutrality –

155MW solar + 42MW waste heat recovery + 8.5 MW biomass (HFAL) + 1.5MW windmill - Once solar plants go live, prices inclusive of interest and depreciation won’t exceed 2.25 rs/unit. Currently they are paying grid prices which amount to 6rs/unit. And the rates at the mine are 14 rs/unit.

- In an interview with CNBC TV18, Abhishek quantified these savings to around 100 cr on an annual basis.

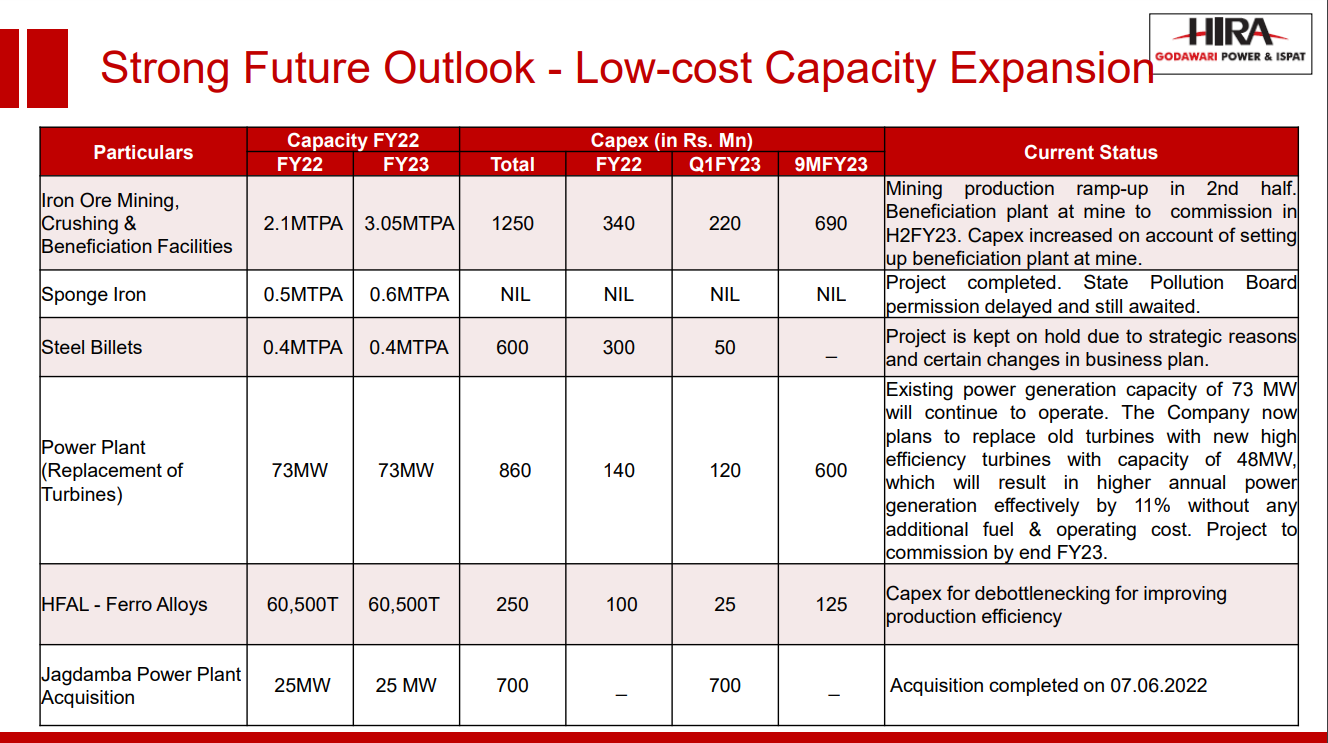

Capex + Greenfield Project Updates:

- Maintain guidance of 500 cr capex in FY23, of which 150 cr undertaken in 1QFY23.

- Greenfield capex still in planning stages. Finalising of design, size, capacity and technology yet to be done. Processes of environmental approval, land acquisition ongoing. Investments will be announced based on market conditions and cashflow of the company.

- Ore is currently transported from the mine to the complex where it is beneficiated. 20% of the ore becomes waste after this process. So beneficiating at the mine pre transit will save 20% in freight costs. Cost of beneficiation – 150rs/t.

- Beneficiation at the mine will also help them accurately pay royalties under a recent IBM rate which is based on concentrate level.

Coal:

- Had to buy thermal coal for the sponge iron plant which lead to higher expenses this quarter.

- Moved from higher grade RB1 coal to RB3 for cost reasons. Might lead to 2-5% dop in production but will be made up by lower costs.

- Trying to bid for a captive coal mine under auction in order to fulfill the long-term requirements of GPIL, HFAL and AFAL which are now dependent on linkages from Coal India. Have been unsuccessful so far because of the cost structure but should be able to acquire one once the premium is within their range band.

Iron ore costs:

- IBM royalty rates are lagging by 3 months and they are currently paying royalties as per iron ore prices in May. This should reduce by 200-300rs going ahead based on where iron ore prices are now.

- Fuel costs also contributed in the way of diesel prices. Both these factors combined have led to a 450 rs in landed cost of iron ore.

Overall, management has guided that the focus for the next few years will be bottomline as significant topline expansion can only come after the greenfield project is live. Was hoping for them to share some idea of what they have planned for growth ahead but I guess the delay is understandable given the situation post export duties. I find the company to be trading very cheap even on sustainable earnings at current capacity.

Some upside risks I see are significant cost savings (power, freight), increase of share of high-grade pellets in mix, reduction/removal of export duties, China infrastructure + realty stimulus.

Downside risks are significant fall in commodity prices globally due to recession fears, China debt contagion.

Disclosure: Invested

| Subscribe To Our Free Newsletter |