Q1FY23 Result:

Positives: Very big jump on PAT on QOQ as well as YOY basis, along with AUM growth.

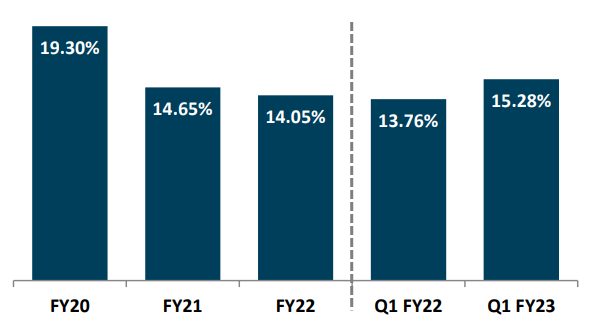

QOQ ROE improvement to 15.28 vs 14.47 previous quarter vs 13.76 in Q1FY22. Co used to do 19% ROE precovid

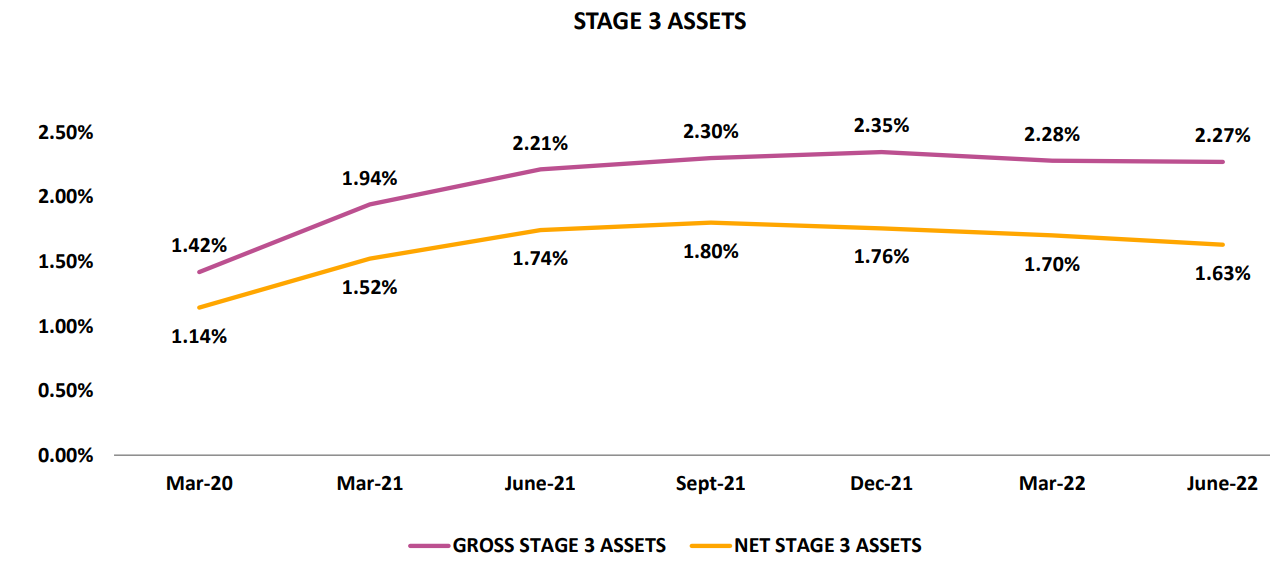

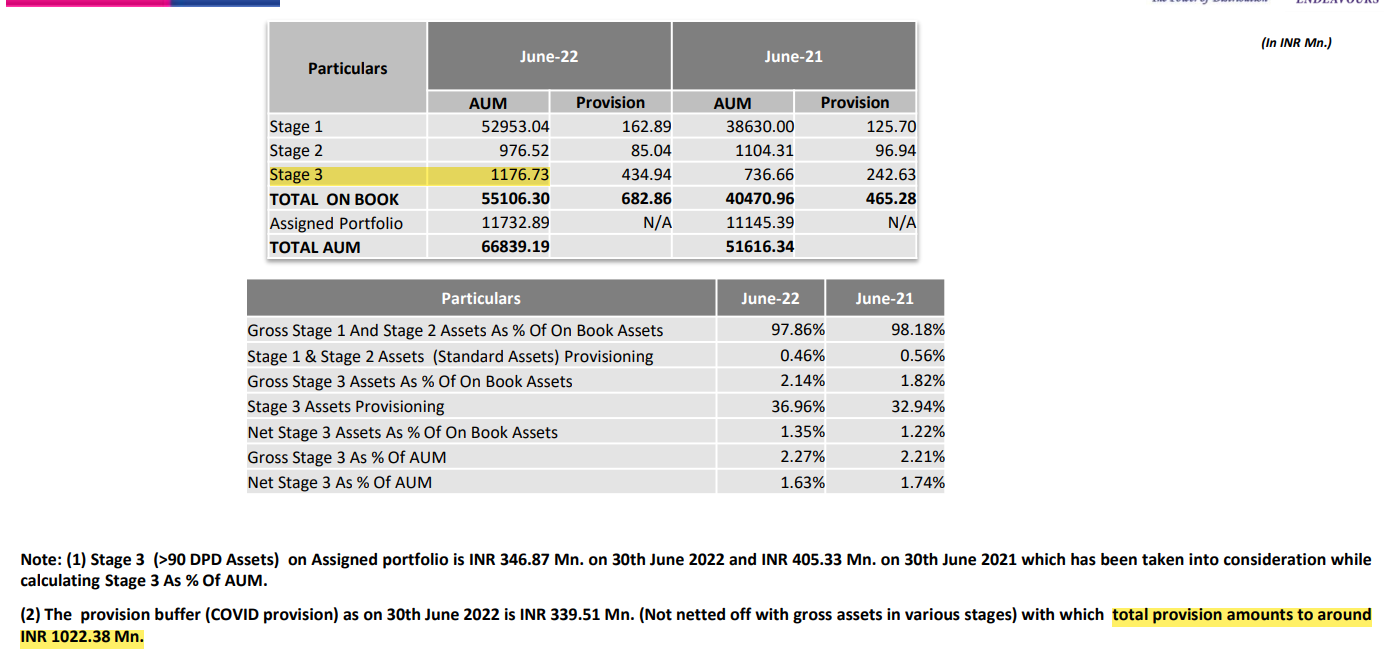

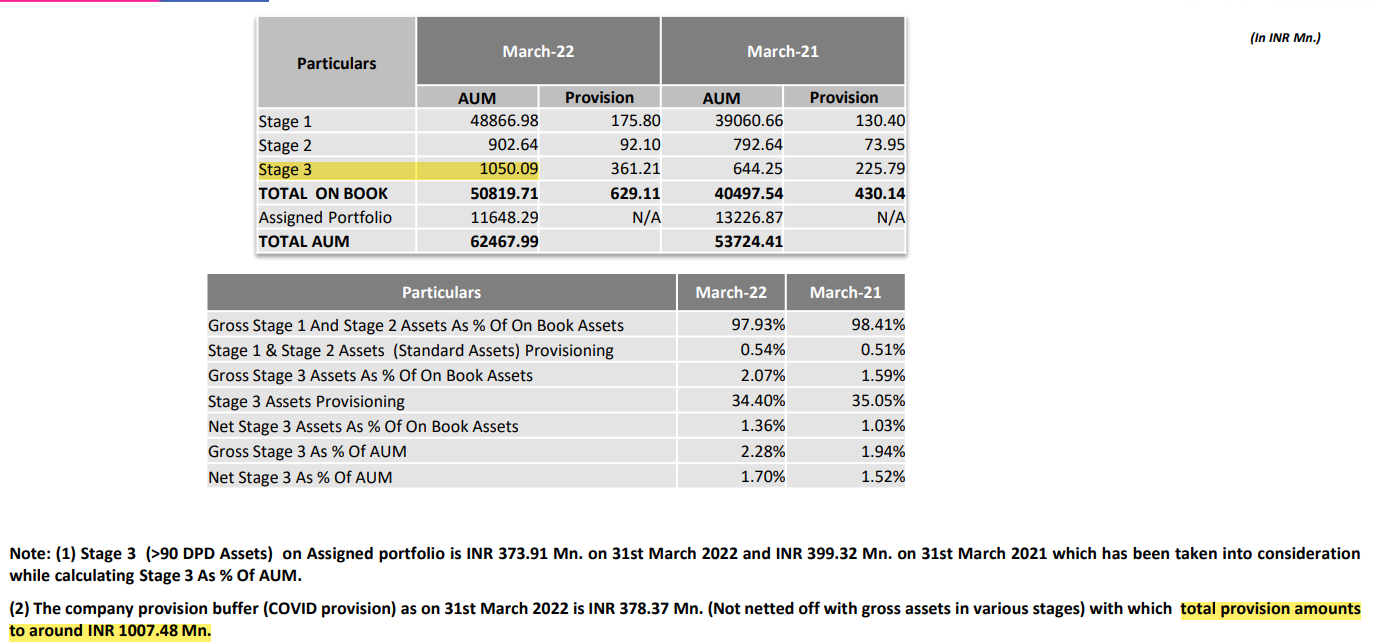

Negatives: Though GNPA & NNPA ratios improved QOQ but absolute numbers have jumped at a faster rate than AUM growth. Total provisions more or less same.

Valuation wise company is at PB ratio of 2.35 used to be available at PB ratio of 4 pre-covid. So the question boils down to can it touch pre-covid ROE while maintaining the asset quality? What gives comfort is when DIIs and retail fellows sold in recent correction the Promoter bought from open market.

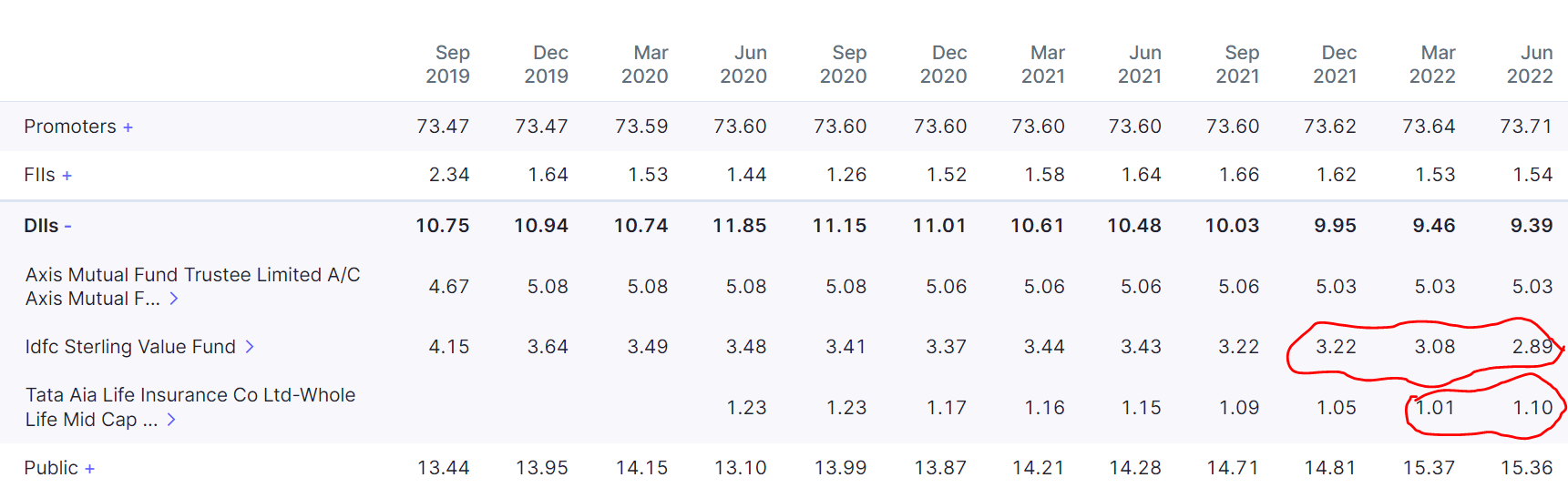

Looks like once IDFC Sterling Value Fund stops selling the stock will go up. Till then it’ll consolidate maybe.

Disclosure: Invested and biased.

| Subscribe To Our Free Newsletter |