Hey @nirvana_laha! Yep when I was an investor I too was mostly unable to find much info regarding issues with management. Many investors I respected seemed to hold a negative view of it, and I didn’t know why.

-

Political association. Tanla mentioned in the article, please go through. In fact, My hometown(in Andhra) is a locations where some investments were kept.

Jagan Mohan Reddy is worth Rs 16,97,335 crore: TDP | News Archive News,The Indian Express -

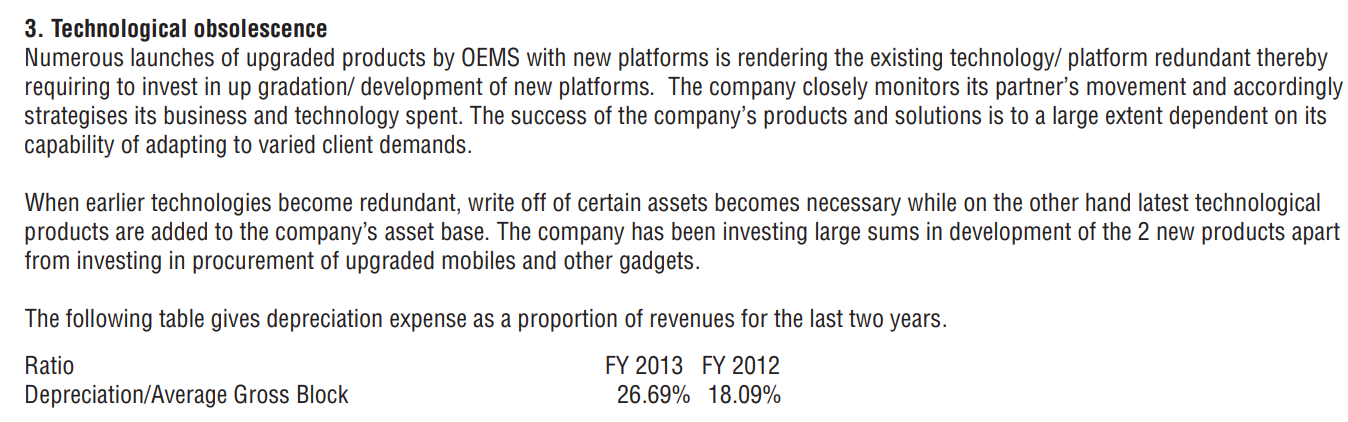

I’m not very good at forensic accounting but the fraud thread at VP pointed me in the direction of purchasing assets(with the help of foreign subsidiaries) and writing them off(essentially insinuating a siphoning of funds). This is not from 2020, this is from previous bull run. Again I’m not very good at this. If someone who was good at this could interpret the statements from 2007-2012 it would be great!

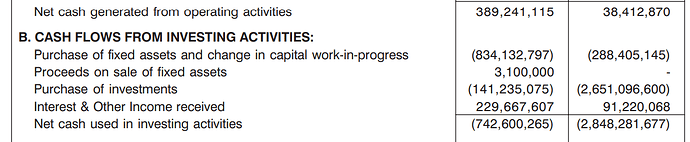

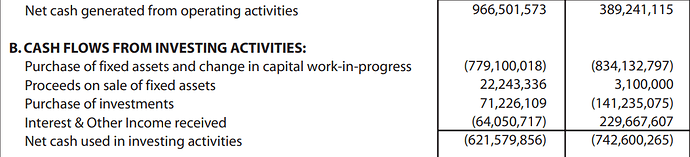

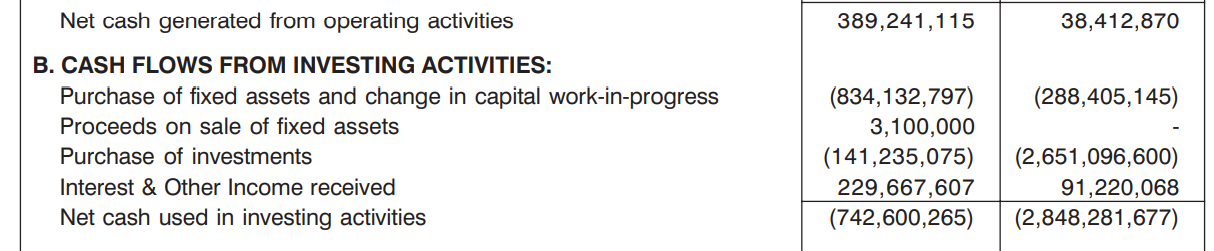

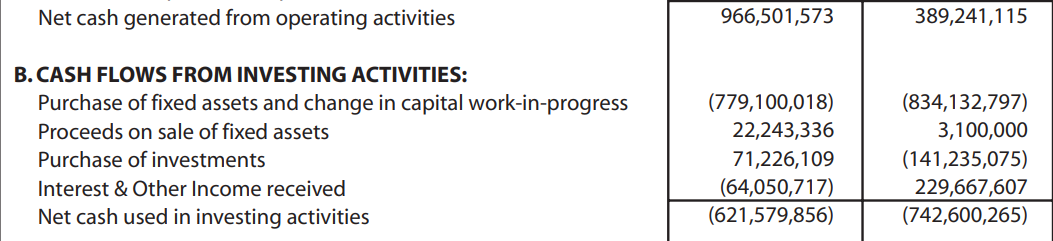

2007

2008

2009

2012 where the ARs mentioned the write offs. Next image shows the writing off of fixed assets on BS. Also they did mention that assets were depreciated differently for Tanla UK and Singapore(I don’t shine at this accounting but a better informed and practised individual feel free to correct me on whether I’ve interpreted this wrongly)

- I remember reading a particular concall where a participant asked about this and IIRC Dasari Uday Kumar Sir was irate at the questioner and changed the topic to business performance and mentioned something along the lines of it not being a point of significance and that the investors should not be worried about it.(he might be right about it being insignificant/things of the past etc but still).

Now to your second point. Yes what Tanla has done is remarkable no doubt, but I didnt say the tonality of inspiration in the article was off to me, what I found rather weird were the lines I highlighted. The rest of the article goes into the inspiring story. We can interpret this differently of course, but for me personally not a big fan.

Tanla might not be comparable to WIPRO imo, it hasnt proved itself where it can comfortably escape scrutiny in shifting business multiple times. Many companies which pivot multiple times/change names have a distrust among investors. Few like Azim Premji sir do it well.

Finally, I have not financial interest here. Hopefully I’m wrong and Tanla shareholders do well. If someone with more experience could read the statements and give a clearer picture than I did, it would be great! If nothing fishy is going on here(too much cash held up in foreign subsidiaries) then great! All I’m saying is that the shady side of tanla’s poor CG of the past should be kept in mind.

P.S mentioning as a side point. Tanla’s price action is one thing to keep in mind. Companies usually dont underperform agaisnt a broad market index as badly as Tanla has without a reason(usually). 2000 all the way to 700 is significant and I don’t think it is all becuase of de-rating and bad biz performance. But price action isnt always perfect which is why I kept it in the end. You can choose to disregard this.

| Subscribe To Our Free Newsletter |