Below average results by Sandhar.

-

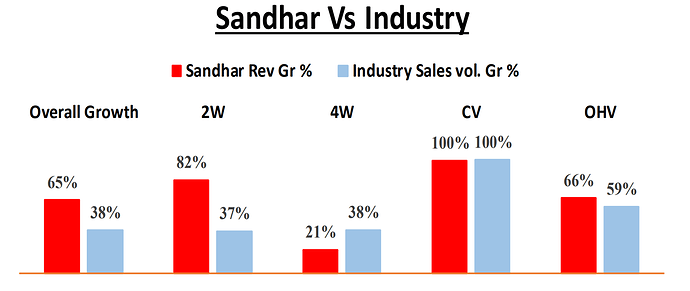

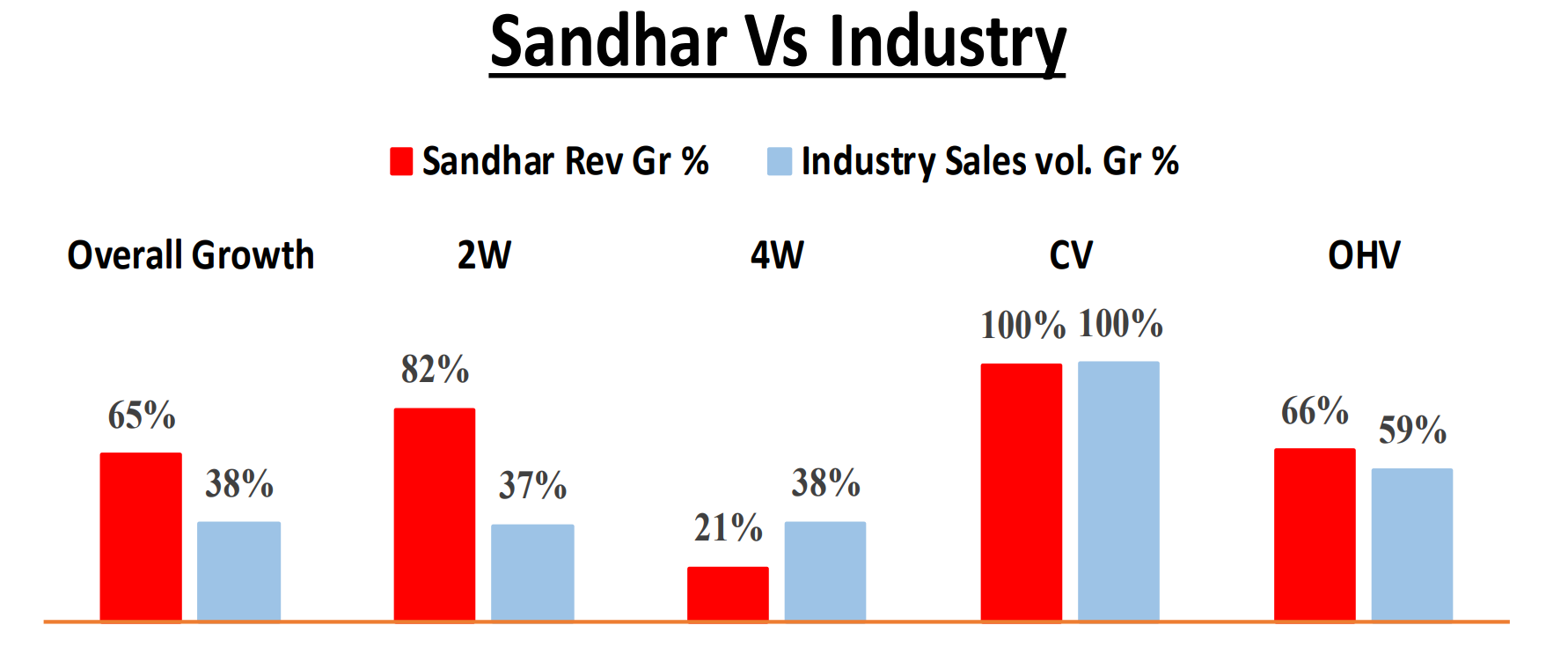

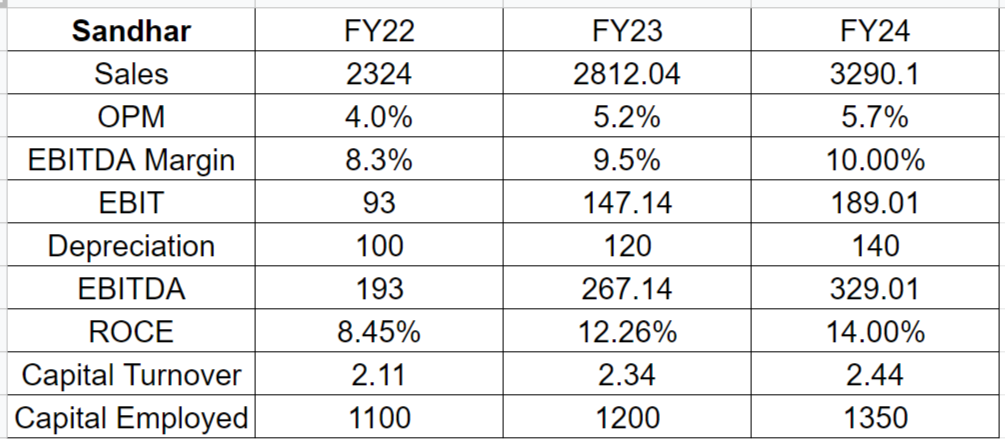

On revenues. Flattish Q-on-Q. Aggresive guidance by mgmt hasnt yet played out. Although they have continued to do better than their industry overall.

-

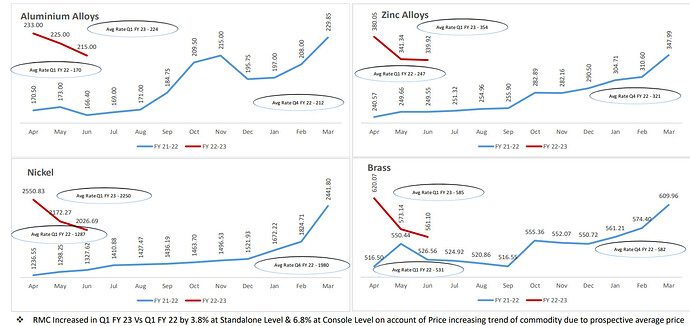

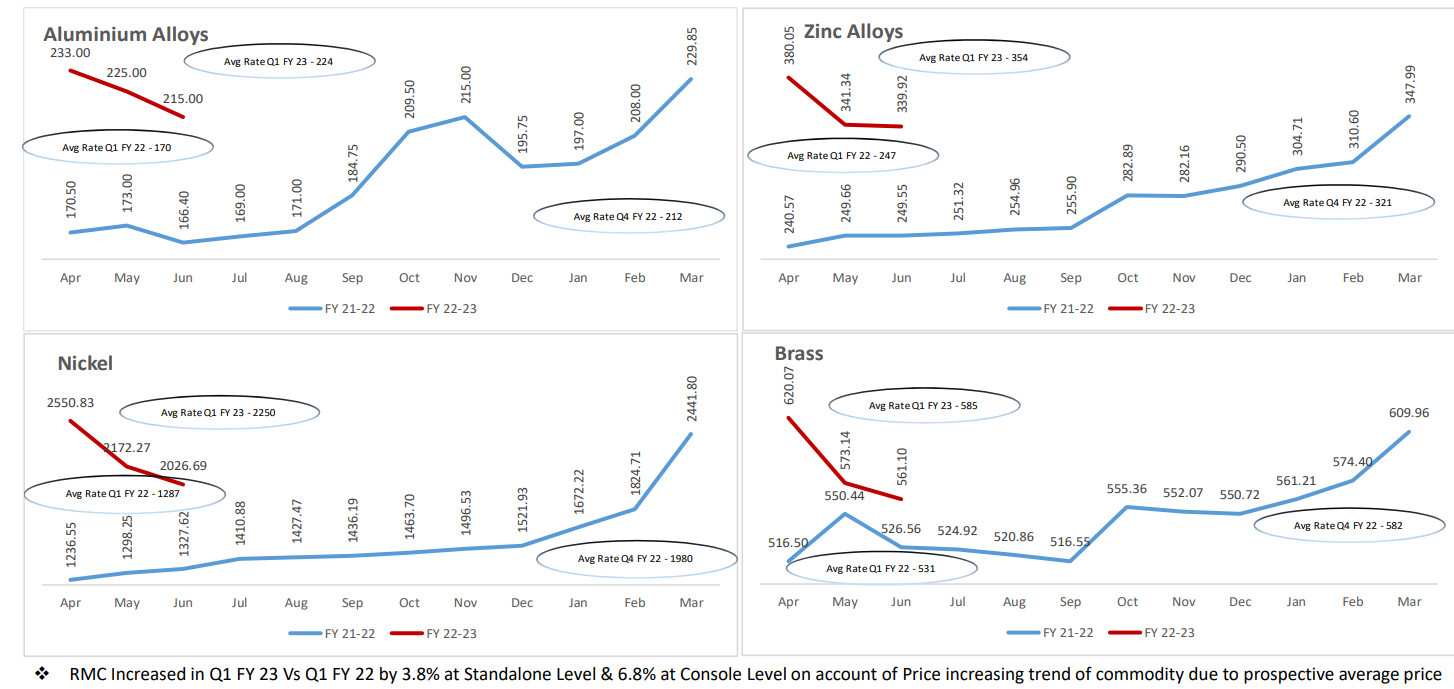

On margin front. A central part of my thesis is RM cooling off which has also continued to rise(not under managements control). Costs continue to be a drag.

Auto sector volumes look promising, in Sandhar’s case, 2W industry has not come back to its 2019 numbers yet. We might be poised for a cyclical upturn.

Over the next 2 years, RM prices should ideally cool off and margins can surpass 10% mark easily. IMO, if company can register a sales growth of 20-25% or higher for the year with 9.5%+ margins for FY23 with an auto upcycle, it could trade 1x price to sales.

Another thing to monitor is cost of debt. Sandhar has a levered b/s with 0.7x D/E(high considering ROEs here are sub 10%). Higher interest rates could visibly dent Sandhars P/L. Already interest costs have risen from 4 crores to 7 crores. For a not very profitable biz like Sandhar these costs will affect earnings by a lot. Will be interesting to see interest costs for Q2.

They have also depreciated 29 crores(I assume this would increase over the year) as against ~25 crores.

As against what I projected, depreciation qrtrly run rate is already up there, so looks like it would increase.

Key things to monitor here on IMO would be RM prices + mgmt execution on increasing wallet share. As mentioned, Hero isnt doing as well as TVS and M&M.

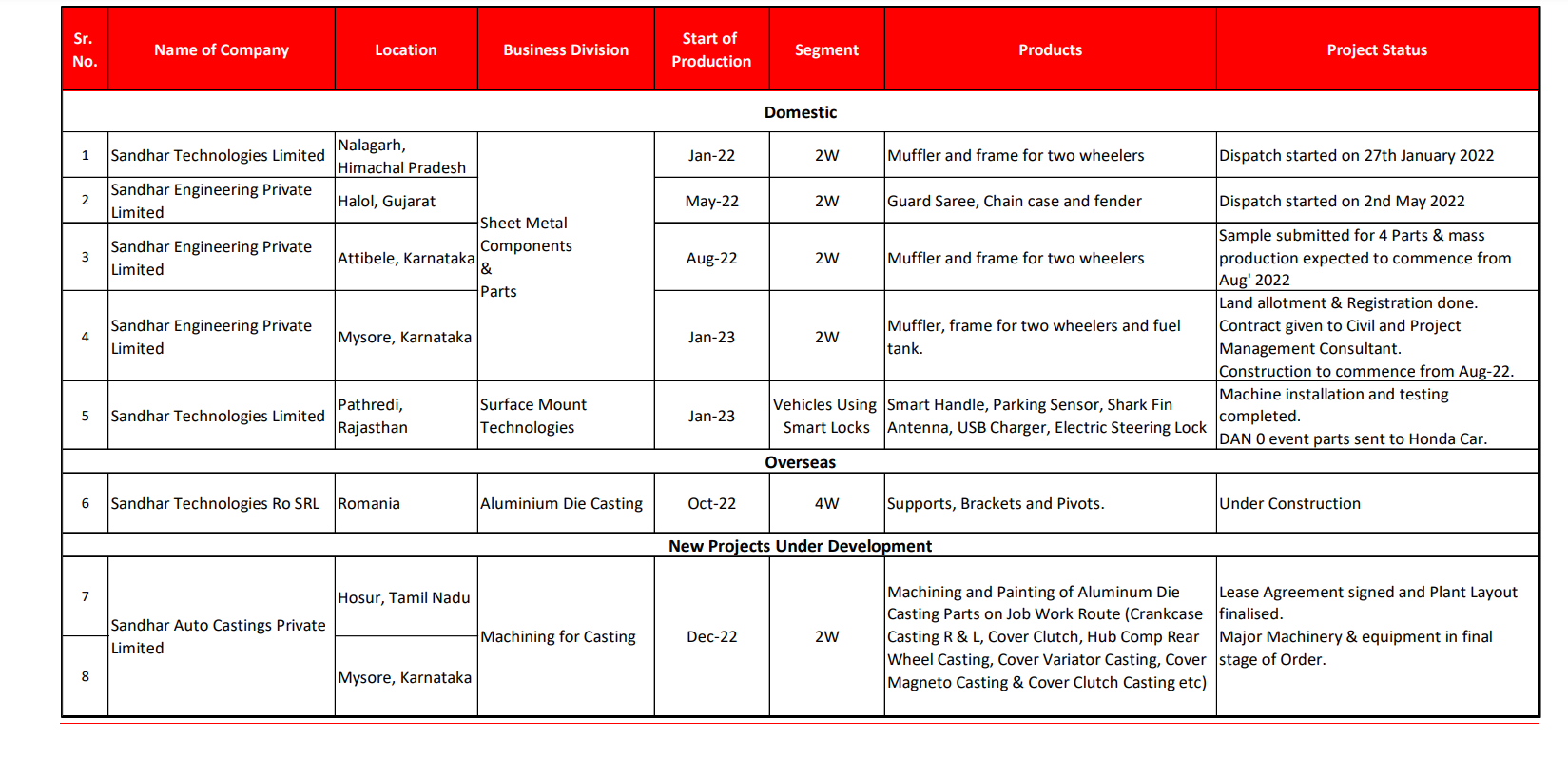

A few projects have been postponed. Prev qrtr vs Q1 FY23.

Overall still bullish over 2 years but RM continues to drag Sandhar. Waiting for mgmt commentary.

Disc – invested. Position sizing here.

Technically setting up decently, relative underperformance to auto index is shown. Important resistance at 265 or so. Higher low has been taken which is good.

| Subscribe To Our Free Newsletter |