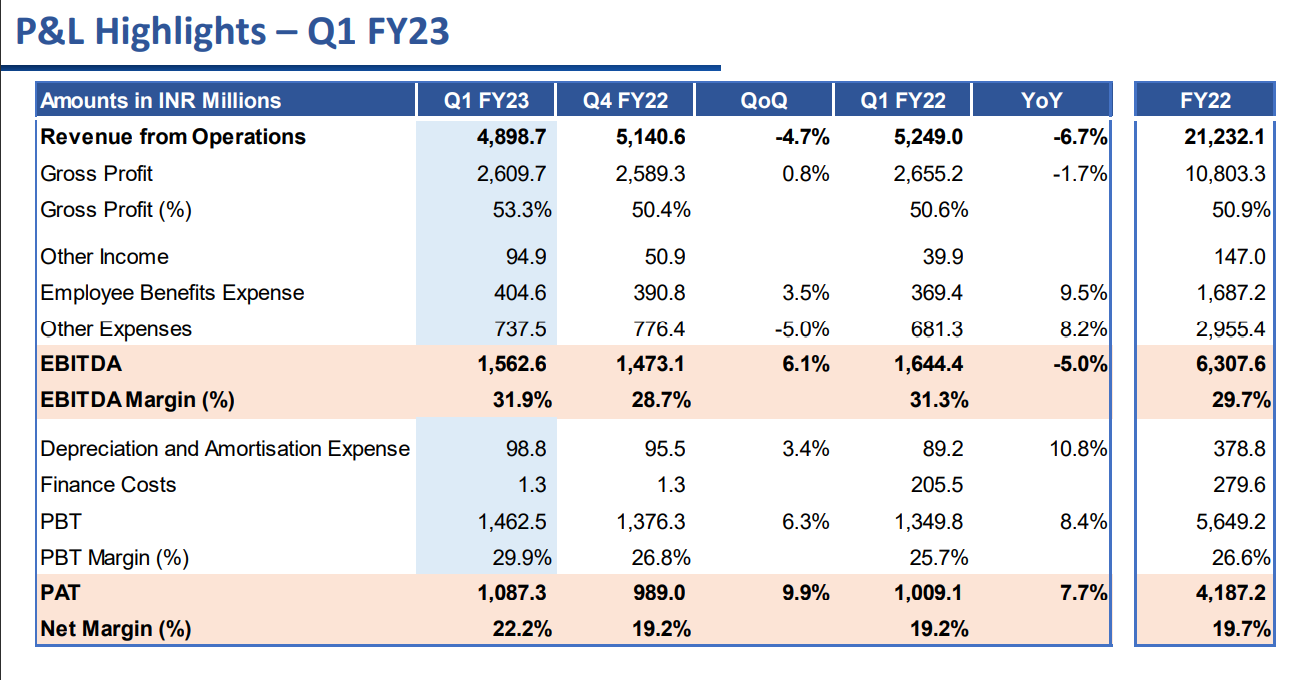

- Margin expansion by 300bps is a pleasant surprise

- Strong profitability in a tough environment. Shows resilience of business

- Marginal decline in topline due to covid sales. Ex-covid sales, reasonable growth.

- CDMO degrowth was a miss

- Delay in capacity addition by one quarter

With:

EV/EBITDA < 10

PE < 15

ROICE of 37%

Cash on books ~514 cr

there is margin of safety in an otherwise expensive market.

D: Invested

| Subscribe To Our Free Newsletter |