Q1FY23 Concall Notes

- Gold Loan Business

-

“Pressure from banks and fintechs seen easing somewhat in the face of reversal of RBI’s COVID-related LTV relaxation for banks and tighter liquidity conditions for fintechs. Going forward, the Company intends to prune the low yielding, high ticket loans (6.9% teaser portfolio that was introduced during Covid). This is a conscious measure and the income associated with such portfolio is not high.”

-

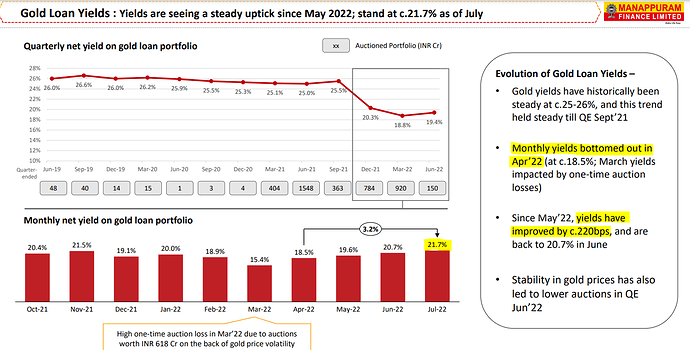

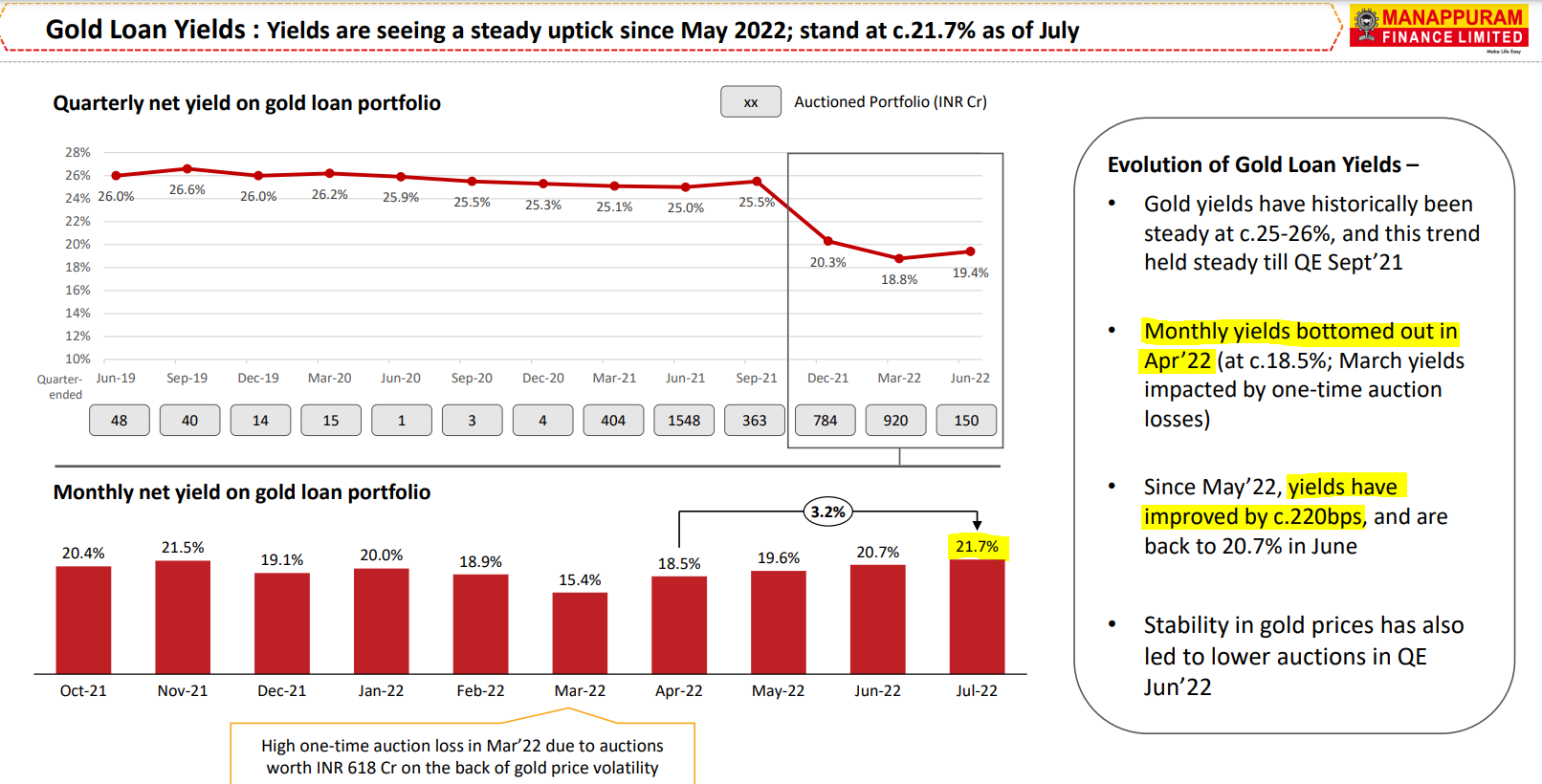

“Net yields on Gold Loans improved from 18.8% in QE Mar’22 to 19.4% in the current quarter. As at the end of July, yields have further increased to 21.7%. Yield improvement largely driven by rationalization of low-yielding schemes.”

-

Yields will settle at around 21-22%

-

- MFI Business

-

collection efficiency for the quarter at 102%

-

GNPA of new book (disbursals post May’21) is less than 1%

-

320 Gold loan branches under Asirvad as of now.

- Gold AUM currently at Rs.421 crs

- No RBI approval needed here but the cap is at 25% of total AUM

-

Management believes that high provisioning for Asirvad is coming to an end of cycle.

-

Incremental disbursement NIM is around 15%

-

- Cost of borrowing increased by 10 bps on a sequential basis during 1QFY23.

- Central bank hiked the custom duty on 1st July 2022 from 7.5% to 12.5%.

- 10% of book is still under teaser loan.

- Maturity upto December 2022

- Might come back during diwali. (One has to keep eye)

-

Competition is similar to 6 months back.

-

The demand from lower segment has yet to come back to Pre-COVID levels

- Demand picks up sowing season that is from September.

- Demand for gold loan is stagnant as of now

-

The demand from lower segment has yet to come back to Pre-COVID levels

- Guidance of provision:

- half of last year

- Might increase next quarter but would stabilize in second half of the year.

| Subscribe To Our Free Newsletter |