I like the growth in revenues which is in line with management’s commentary.

However there are a few items in the AR which spook me.

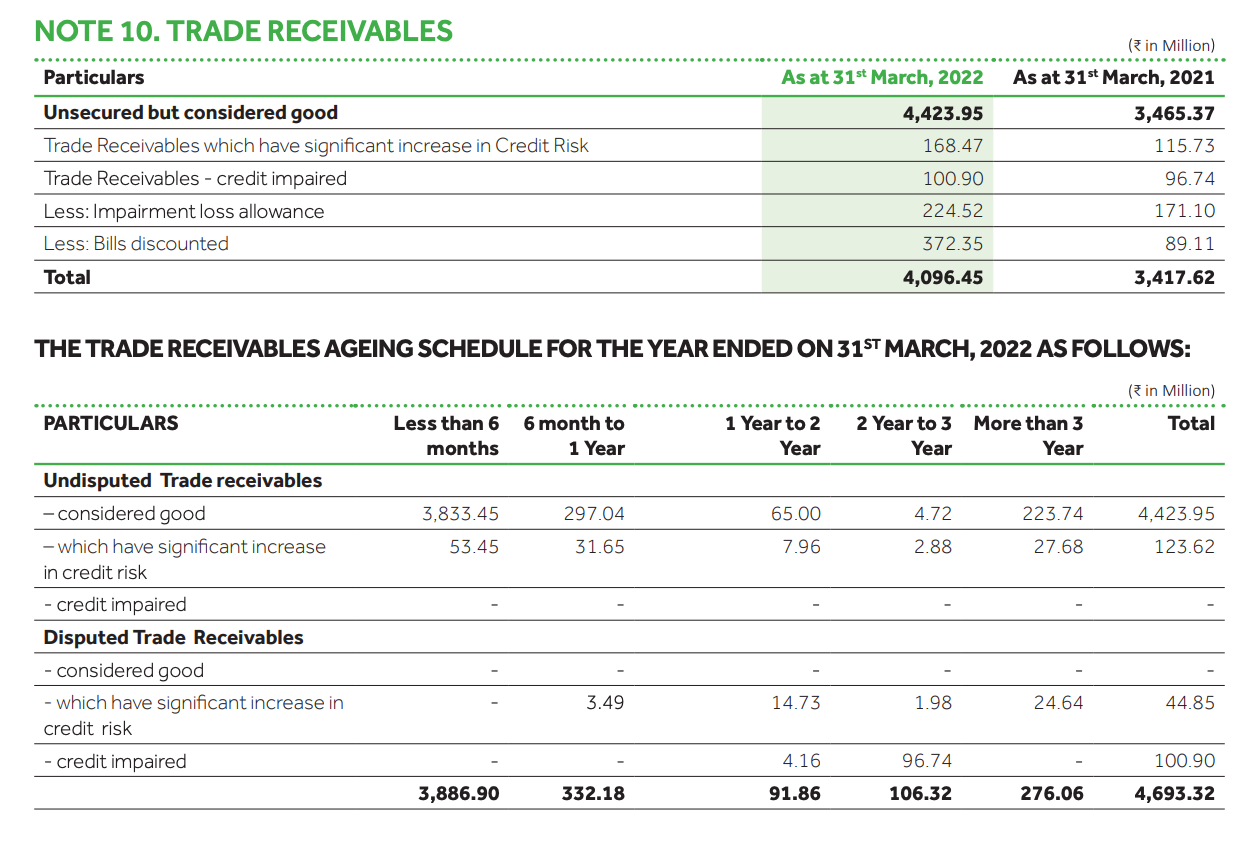

- Receivables: This is quite bad for Heranba and I read above in this VP thread that management has guided that issue will start correcting by end of FY22.

Net receivables increased from 341cr to 409cr. To put things in perspective, the PAT is 189cr.

Then there is 22cr credit impairment allowance, which is 11% of PAT.

Receivables with significant increase in credit risk + credit impaired = 27cr. This most likely will be next years credit impairment allowance.

Then there is bills discounted of 37.2cr. From what I understand the company sold receivables worth 37.2 cr to a third party/ bank. Will touch this again at the end of this post.

-

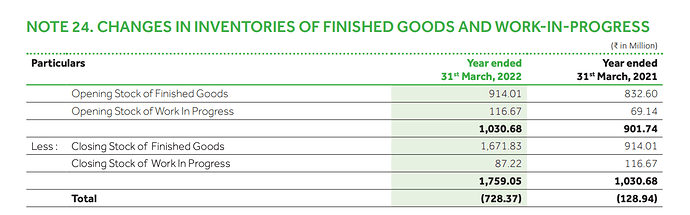

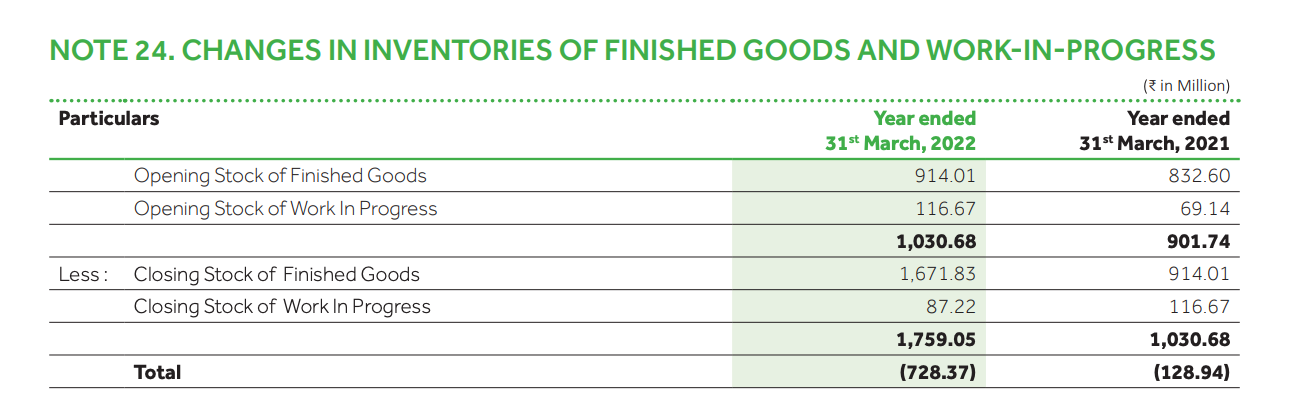

Inventory buildup of 73 cr. Is this inventory mismanagement?

-

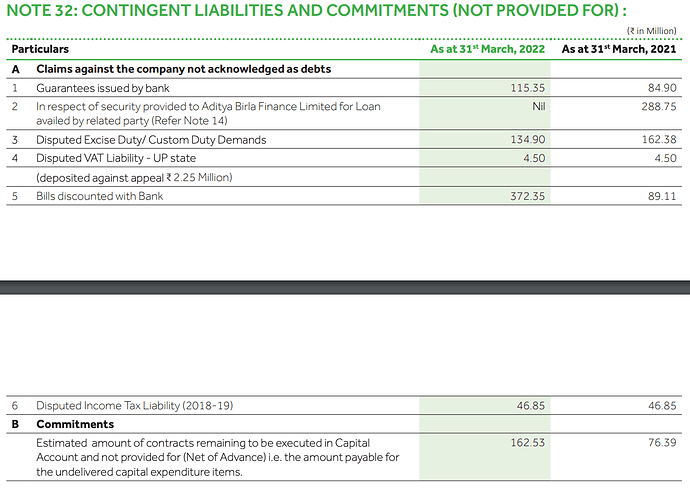

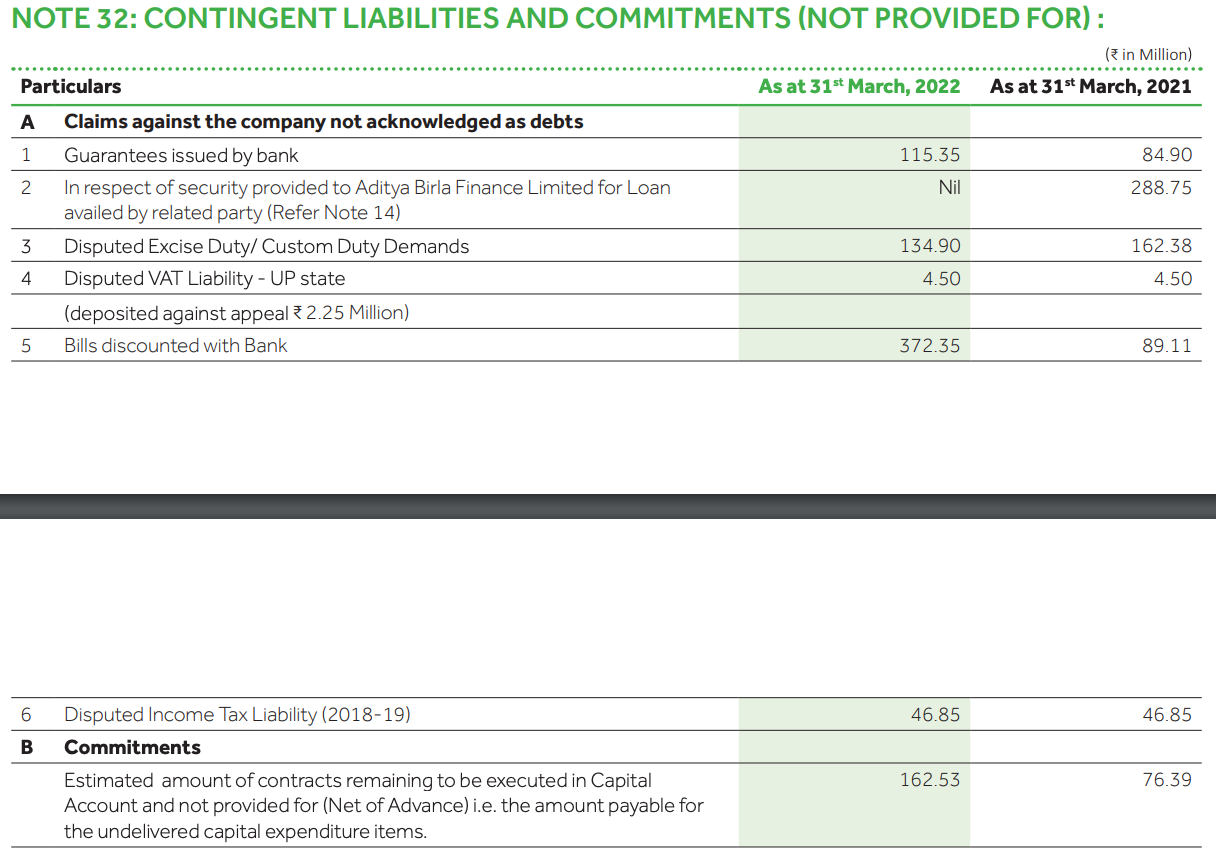

Contingent liabilities & discounted bills

#5 reads that there is a contingent liability on the Co for 37.235cr. This means that the company is still liable for recovery of this amount even though it sold the receivable to a bank.

Can anybody please educate me if this is the correct understanding?

disc: invested, not a large position

| Subscribe To Our Free Newsletter |