True, results are inline with expectations. Margins look worse but discounting for peak inflation and supposed fall in glass prices, these are decent numbers. Topline holding at ~170cr suggests either glass prices stayed around 132-135 levels or there was better volumes or better product mix. Coming quarters should see re-entry into mgmt guidance zone of 30-35% ebitda with sliding commodities.

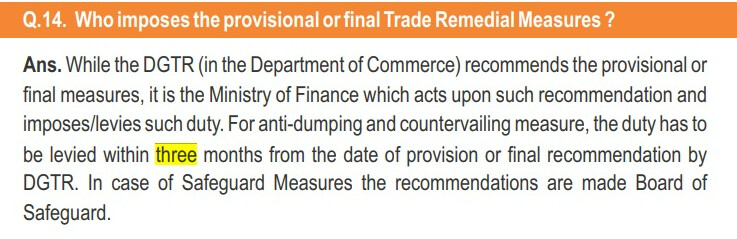

However, the elephant in the room is ADD extension. Here’s a clip from a publicly available govt doc on duties.

“Duty has to be levied within three months from the date of provision or final recommendation by DGTR”…

We are 1 week away from that expiry date!!

| Subscribe To Our Free Newsletter |