Incorporated in 2002, Vedant Fashions Ltd. (VFL) is the only pan India franchisee in the Indian wedding and celebration wear segment in a market having regional players. It offers one stop destination with wide array of offering across its 5 brands – i) Manyavar, ii) Mohey, iii) Mebaz, iv) Manthan, and v) Twamev.

India is a land of festivals that celebrates weddings in glorious ways. VFL benefits from the 3-5 days wedding culture in the country (estimated to have ~1 crore weddings every year) giving it the scope to sell multiple products to a single customer. The shift towards ready-made wear due to quick and enhanced product experience while compared to tailor-made also provides a huge scope for growth.

We are optimistic on Manyavar due to-

- Optionality through Mohey- Mohey took 5 yrs to reach 90 cr, Manyavar took 9 yrs. Mohey TAM is 10x Manyavar, we feel if the management cracks the women wedding market right, there could be exponential hyper scaling in store

- Differentiated business model through franchises-royalty on the growth of others

- High quality forensics- implying shareholder friendliness

- Performance indicators against leading consumer brands show power of monopoly- best in class growth , ROCE, revenue CAGR

Watch webinar here:- Is Vedant Fashions the next Titan in the making – YouTube

Download pdf here- Vedant Fashions- The Titan of Wedding Retail- Satwik Jain – Generational Capital

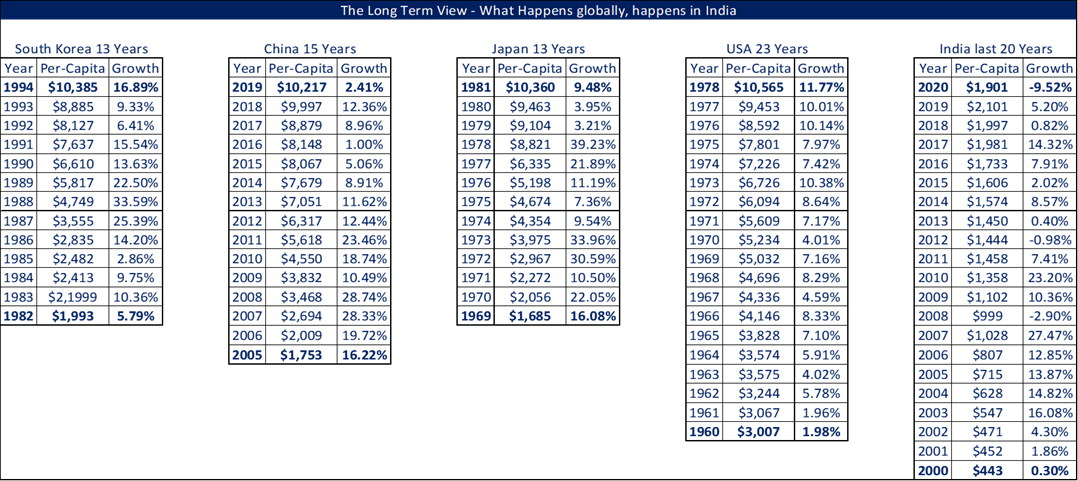

Long term view- what happens globally, happens in India

India is at the cusp of multi-year consumption boom with per capita GDP crossing $2000. Historically we have witnessed massive consumption and equity markets boom in countries in the journey from 2000 to $10000/capita.

As their needs for “roti,kapda,makaan”are satisfied people increasingly spend on aspirational and discretionary goods, leading to a Lalapalooza effect. My sense is India would take between 18-25 years to reach this figure given our growth rates. We cannot waste this opportunity buying companies growing at 5-10% and should look at blitz scalers with ability to double profits in 3-4 years.

Company background

Founded by the iconic retailer, Mr. Ravi Modi 2002, Vedant Fashions Ltd. (VFL) is the only pan India franchisee in the Indian wedding and celebration wear segment in a market having regional players. It offers a one-stop destination with a wide-spectrum of product offerings for every celebratory occasion through its 5 brands – i) Manyavar, ii) Mohey, iii) Mebaz, iv) Manthan, and v) Twamev catering to different segments in terms of price points. As of FY 22, ~90% of its sales was generated from franchisee owned EBOs and the rest by MBOs, large format stores (LFS) and online platforms.

Jewelry market is highly fragmented with 70% organized industry with largest organized player having only 10% market share and 2nd largest player having 5%

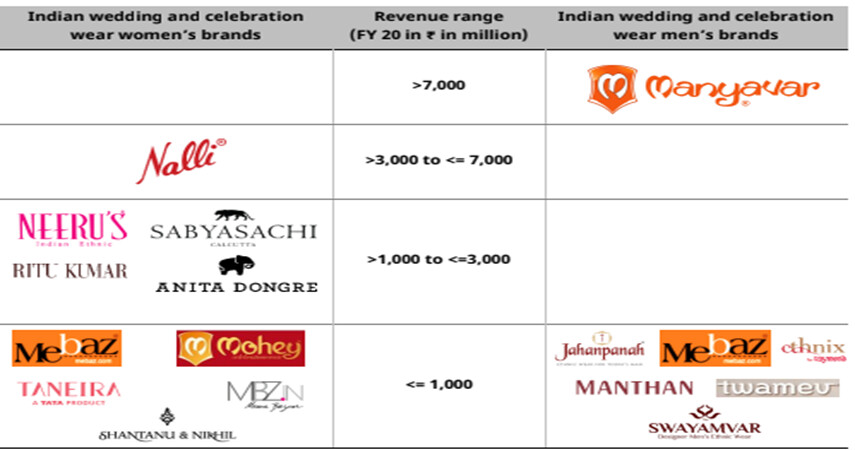

The construct in INR 133 billion Men’s wedding wear market is similar. Organized players comprise 20-25% . The Indian women’s wedding and celebration wear market is estimated at Rs735bn, with an even lower contribution from organized players, at ~15-20%. VFL with ~1000 cr sales has around 10% of organized market, ie 26x of its next competitor in men’s Jahapanah with 40% EBITDA margins where others do not even touch double digits.

Decimating competition- Not the number one, but only one

Despite a large presence in the men’s wear space, VFL boasts of sales that are ~1.6x that of the second-largest organized player in wedding and celebration wear – Nalli, which predominantly occupies the larger, women’s wear space. Within men’s wedding and celebration wear, VFL’s sales are 26x that of second-largest player Jahanpanah Clothing. Further, while EBITDA margin of VFL is impressive at ~40%, that of the rest of the players does not even touch the double-digit.

The secret sauce of quality growth- “franchises”- royalty on the growth of others

VFL follows a franchisee-owned franchisee-operated model, wherein the nitty-gritties of handling store operations are taken care of by the franchisee so that VFL can focus on the more complex aspects of branding, assortment, up-to-date designs, new store openings, etc. This is similar to Titan’s approach, wherein 2/3rds of its sales come from stores operated by franchisees.

Also, both Titan & VFL, via their franchisees, have been able to command extensive town coverage of 231 & 222 cities/towns, respectively, in India.

VFL has two franchisee models:

• One, where VFL bears the rental costs, and margins given to the franchisee are lower, at 18%.

• Two, where the franchisee bears the rental costs, and margins given to the franchisee are higher, at 29.5%.

Typical payback periods of franchises are 3-3.5 years leading to IRR of 20-24% making compelling business propositions. Proof of concept- more than 90% sales are from franchises, 75% franchises are more than 3 years old, 2/3rd franchises operate more than two stores

Optionality- Expanding into adjacencies with everyday festivity wear (Manthan), women( Mohey), HNI Segment (Twamev)

The women wedding wear segment is 10x that of men’s with higher margins & ASP. My blue sky scenario is VFL cracking this market

Proof of concept – Mohey took 5 years to reach 90 cr., Manyavar took 9 years.

Management said on con call they will go into hyper-scaling mode once they reach INR 10000/sq feet from Mohey stores, currently they are between 6000-7000

That might be the pivot

Forensics of very high-quality implying shareholder friendliness

We run a 20 ratio forensics analysis on the accounts of any potential investment along with a 150 key word fraud search to check the background and willing of promoters to share wealth with minority shareholders. We could not find any anomaly there except some minor tax related issues.

Performance indicators against leading consumer brands show power of monopoly- best in class growth , ROCE, revenue CAGR

“There is no capex, there is no fixed expense other than corporate head office salary. Every rupee of working capital can generate an equal rupee of PAT, with 90-95 percent free cash flow. Only Unilever will have a ROCE (return on capital employed) of 100 percent, and we might be the second, and within a year or two, we will be at more than 100 percent.”- Ravi Modi to Forbes

Best regards

Satwik Jain

Disclaimer: – RH Perennial Fund is regulated by the Securities and Exchange Board of India as a provider of Portfolio Management Services (SEBI Registration No. IINA200002601). The information provided in this newsletter does not, and is not intended to, constitute investment advice; instead, all information, content, and materials available in this newsletter are for general informational purposes only. It is safe to assume that we have allocations to all stocks mentioned here and may also sell them without prior notice

| Subscribe To Our Free Newsletter |