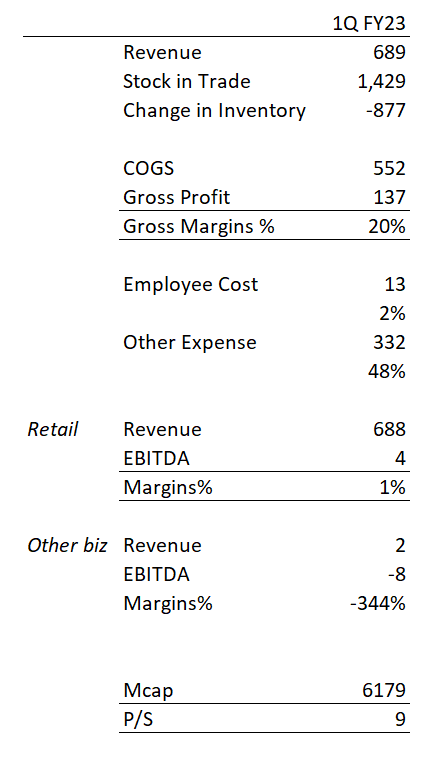

Did a quick review of numbers. >99% revenue is from Retail, COGS is ~80% of revenue. Gross margins are thin and so does EBITDA margins. Not sure if they’ll be able to scale the margins higher.

Out of 332Cr other expenses, 207cr is because of notional loss of Market-cap of RTN power. Normalized EBITDA margins are -1%.

Another point to note from presentation : Majority Shareholders of Revolt Intellicorp Private Limited (“the associate company”) and REL have alleged certain matters against each other, under the shareholders agreement between them and made certain claims and counter claims against each party which are subjected to arbitration and not crystalized so far. REL believes that the aforesaid matter does not impact the consolidated financial results of the Group.

Disc: No investments. Valuations also doesn’t provide much comfort for me at this stage.

| Subscribe To Our Free Newsletter |