- As of this week, have added a large weight in Arman Financial. This is a Microfinance company management that I have come to admire. Aalok Patel has come in and transformed the company from a 1 state (Gujarat), 1 product (Microfinance) company to a multi-state, multi-product entity in the last 4 years. This while facing numerous black swan events over the last 5 years, through which the management has managed to mantain best-in-class asset quality. As mentioned in the previous sport, I think the worst is behind in terms of asset quality in the microfinance sector. In addition, the new govt regulations have structurally improved the economics of the sector by allowing free pricing for MFI NBFCs. Most NBFCs have taken interest rate hikes of 2-4%. Even with cross cyclical credit cost assumptions of 3%, at Arman’s cost structure, it should be able to do 25%+ ROEs at the higher yields. Valuations here were a concern at ~5x P/B. However, promoters provided an attractive optional convertible structure that limits downside and provides a yield that makes the valuation more palatable. My equity should convert in 18 months at ~3 P/B.

My brief assumptions for FY24 are as follows:

FY24 Book Value (Post fund-raise): 427 cr

FY24 P/B Multiple: 3.5 (in line with historical average though I think the fair value for a company with 25% cross cycle ROE growing at 25-30% should be more like 6x P/B)

FY24 Share Price: ~Rs 1650

Expected IRR with preferential dividend of 10% for 18 months: 24%

This is a highly cyclical sector, so I will take a call on what to do with the convertibles after 18 months.

- In addition, have sold some Faze Three in response to the price run up and added some Ganesha Ecosphere instead. Ganesha is well positioned with structural demand tailwinds and new capex coming on stream.

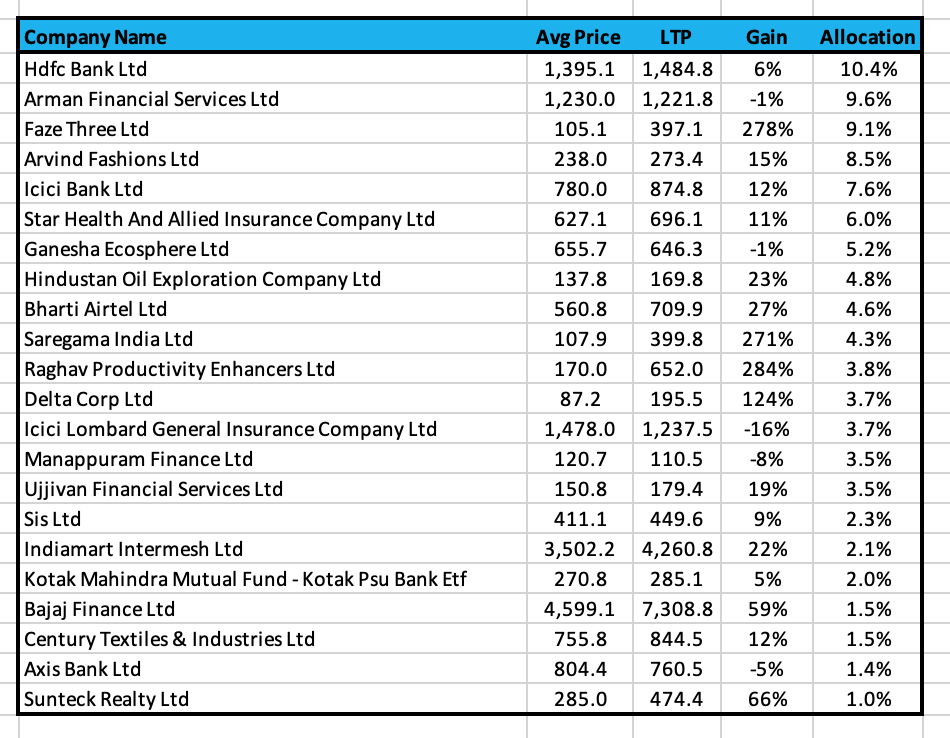

The portfolio now looks as follows:

| Subscribe To Our Free Newsletter |