From high multiples in low mortgage penetration narrative(2014-2018) in hey days of trailing 2.5-3.3x P/B, over the years rising competitive intensity by banks & own asset quality issues have hit a good track record of delivering consistent profits/roe. While the arg of betting on banks reducing their competitive intensity is less uncertain, the tailwinds of better overall RE sales over next few years – growth in the end market via both volume & price, asset quality issues subsiding, better profitability (rising rates albeit a short term factor) when viewed vs current trailing vals makes this an attractive cyclical bet. Keeping aside vol growth, even mid single digit price rise in RE can help the growth no, prices have been broadly flat for past many years in general in tier 1 cities. In 2010-2014 era of very strong loan book growth, price rise too was a factor.

Housing finance has less profitability/roes given the yields, in general has merits in terms of being less risky, long duration, less cyclical.

Outcome is a little less uncertain, allocations accordingly, the payoffs can be really good if nos come through in next 2 years. Hfcs are very negatively viewed in recent times given banks have gone all out in capturing mortgage growth, raising the possibility that growth being shown now by hfcs is on account of more riskier customers than in the past. That could be the case in hindsight. Why bother then? trailing vals discount a lot of negatives & tailwinds help.

1QFY23: “Strength lies in reach. Will have share in the market. Then recently, we have also what you call equipped our the other line of officers. We call that the processing centers at some important centers for what happen now. Our digital operations, what we now engaged into there, also giving good results. So going forward, I think we’ll have a very good edge in the market as for the new disbursements are concerned. And growth for the current year, we are almost aiming at 12% to 15% in our disbursements. That’s one thing. Then as – given our existing book, the total portfolio also will be more or less moving in the same range of 12% to 15% by end of the year.”

1 negative is asset quality issues can further pop up spoiling nos for next 1-2 quarters. Not necessarily, management does not expect it, but it can be the case. Still unless it’s very material, given the growth outlook vs baked in valuations today, it’s worth a buy.

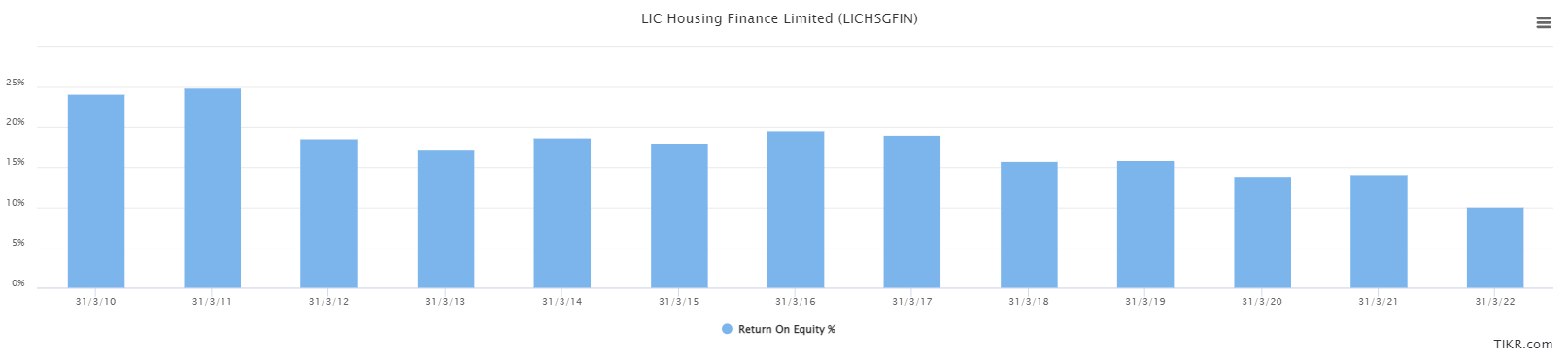

Over the past decade, roes have come off first from above 20%+ to 15%+ to about 10% in FY22. Better not to expect too much in terms of improvement, not going back to 16-18-20%, if we get double digit loan book growth, and roes head back to 13-14%, earnings growth & val rerating to say 1.5x can give 60-70% upside.

Disclosure: invested

| Subscribe To Our Free Newsletter |