Had posted this today itself in the 52W high thread and post was up for approval – good to see thread started and putting in my points here now.

Rico Auto – close to 52 week high

- Rico is a manufacturer of Aluminium and Ferrous castings for Auto OEMs with clients such as Maruti, Kia, Tata, Honda, Bajaj

- It serves the CV, PV and 2W industry, with ~77% revenues coming from India

– Fundamentals look good in my opinion as there could be scope for sales growth + margin expansion + valuation expansion if the auto cycle plays out

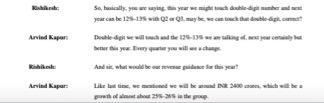

**Sales growth and Margin expansion guidance from latest con-call **

- Management guiding in latest concall for 25-26% sales growth with FY 23 revenue at 2400 Cr (1860 Cr revenue in FY 22)

- Management guiding for margin expansion to 11-12% by FY 24, and at least double digit margins in coming quarters. OPM for FY 22 was 8%

Potential valuation upside in case guidance is met?

Market Cap to sales currently is still at range lows of 0.3x.

This is still below 10 year median (0.4x sales) and far below peak of last auto cycle (1.3x sales)

Disclosure : I am invested and biased

| Subscribe To Our Free Newsletter |