Some pointers from the PI Industries Annual Report for FY2021-22:

Financial

-

Consolidated Revenue from operations for the year was Rs.5,300 crore and PAT was Rs.844 crore. Revenue growth for the year was 16% and PAT growth was 14%. Operating margins stood steady at 22% while Cash Flow from Operations was down Rs.725 crore to Rs.529 crore, thanks to increased working capital requirements. Free cash stood at more than Rs.2150 crore.

-

More than 4 % of the income now comes from Subsidiaries. Main operating subsidiary is Jivagro, which houses the company’s horticulture business. Its revenues for the FY22 were Rs.282.1 crore with a PAT of Rs.15.6 crore.

-

Total CAPEX entailed in FY 2021-22 was Rs.320 crore and assets capitalised during the year were Rs.481 crore. Capital WIP now is just Rs.64 crore which implies much less capex will be incurred in the current year.

Business

- Three fourths of the business came from active ingredients & intermediates, and a quarter from formulations. Broadly, this should correspond to the CSM and domestic business respectively.

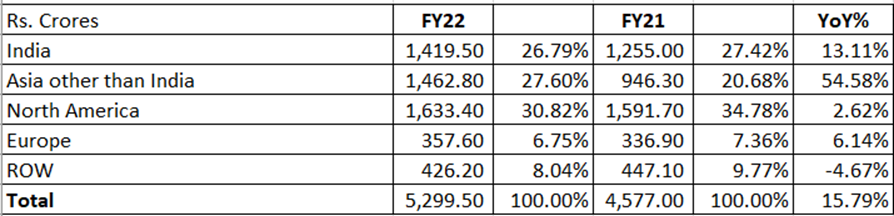

- Geographical distribution was well distributed with around a quarter to one third coming from India, Asia (mainly Japan I guess) and North America respectively.

-

Company has five formulation facilities and 15 multipurpose plants under its four manufacturing locations, 400 scientists and researchers and deep symbiotic relationships with over 20 global innovators.

-

Piloted a drone application. Last year, company made a successful foray into electronics chemicals.

-

During the year, 2 additional Multi-Purpose Plants (MPPs) were fully commissioned. 2 new Electronic Chemicals were launched marking the company’s foray into this niche specialized field offering promising potential in future.

-

In CSM exports, the 9 new molecules commercialized were the highest in a single year. The company has also operationalized “Flow-Chemistry” at pilot level and also successfully commissioned manufacturing facility for MMH and established Azide chemistry at a commercial scale.

-

In domestic agri brands, PI received 3 regulatory approvals during the year, which also included the first product to receive MRL exemption in India.

-

Horticulture portfolio under Jivagro saw launch of 13 specialised brands at a go. This, by far, was the highest number of brand launches in a single year.

-

During the year, the R&D team worked upon more than 40 products at different development stages and pipeline has more than 20% non ag-chem products. PI crossed the milestone of having filed more than 130+ patents. Total R&D expenditure as a percentage of revenue was 2.71%.

-

The Company commissioned a pharma lab at Udaipur (Rajasthan) and is also working on technology scale up of novel catalysts, enzyme technology and green chemistry (ecoscale).

-

The company incorporated one wholly owned subsidiary having its registered office in the State of Rajasthan for carrying out pharma activities namely – PI Health Sciences Limited.

-

During the year under review, Isagro (Asia) Agrochemicals Private Limited business other than B2C got merged with PI Industries Limited

-

Regulatory delays in securing the approval for new products delayed many of the new launches during the year and has some impact on the business for the year.

Accounting

-

The Board declared an interim dividend of Rs. 3/- per equity share in February 2022. In addition, a final dividend of Rs. 3/- per equity share is recommended.

-

Promoter remuneration for Mr. Mayank Singhal is Rs.16.50 crore and Rs.29 lacs for Mr. Arvind Singhal. This is 2 % of the Consolidated PAT.

-

There is an unrealised loss on foreign currency transactions (Net) to the tune of Rs.60 crore in Cash Flow Statement compared to an unrealised gain of Rs.31 crore.

-

Provision for Bad and Doubtful debts & Advances is made for Rs.22.50 crore. This was Nil last year.

-

Disputed tax liabilities have increased from Rs.43 crore last year to Rs.106 this year.

-

There is one customer having revenue of Rs.1743.5 crore including an amount of Rs. 869 crore and Rs.874 crore arising from shipments to United States of America and Japan respectively.

Going ahead

-

The Annual Report says the company is likely to benefit from the maturing of its new product launches of the recent year.

-

In addition, the company is planning to launch 5 new products in the domestic markets in FY 2022-23.

-

Moreover, its focussed approach to horticulture segment through Jivagro coupled with a healthy pipeline of new launches shall support growth in domestic markets in FY 2022-23 and beyond.

-

With scheduled commercialisation of 7 new molecules and 2 new process innovations, the company is well placed to sustain its growth and profitability trends in FY2022-23.

-

Order book position continues to stay strong at $1.4 billion with high visibility growth for the next couple of years.

-

On bio-pesticides, the report says emergence of bio-pesticides is making a splash in the existing crop protection market. However, product features of bio-pesticides are so limited as compared with traditional CPC products that later has not gained popularity.

(Disc: Invested)

| Subscribe To Our Free Newsletter |