I have been adding MSTC since the past one year now. As this thread has been dead for some time, I thought I would update it with my thesis and rationale to help other investors as well as move the discussion forward.

I will not add too much about the background of the company since it has all been already discussed. The video uploaded above in the thread gives a good background of the transformation the company is going through. I will simply share 3 reasons why I feel this is an attractive opportunity –

1. The write offs from the trading business are complete

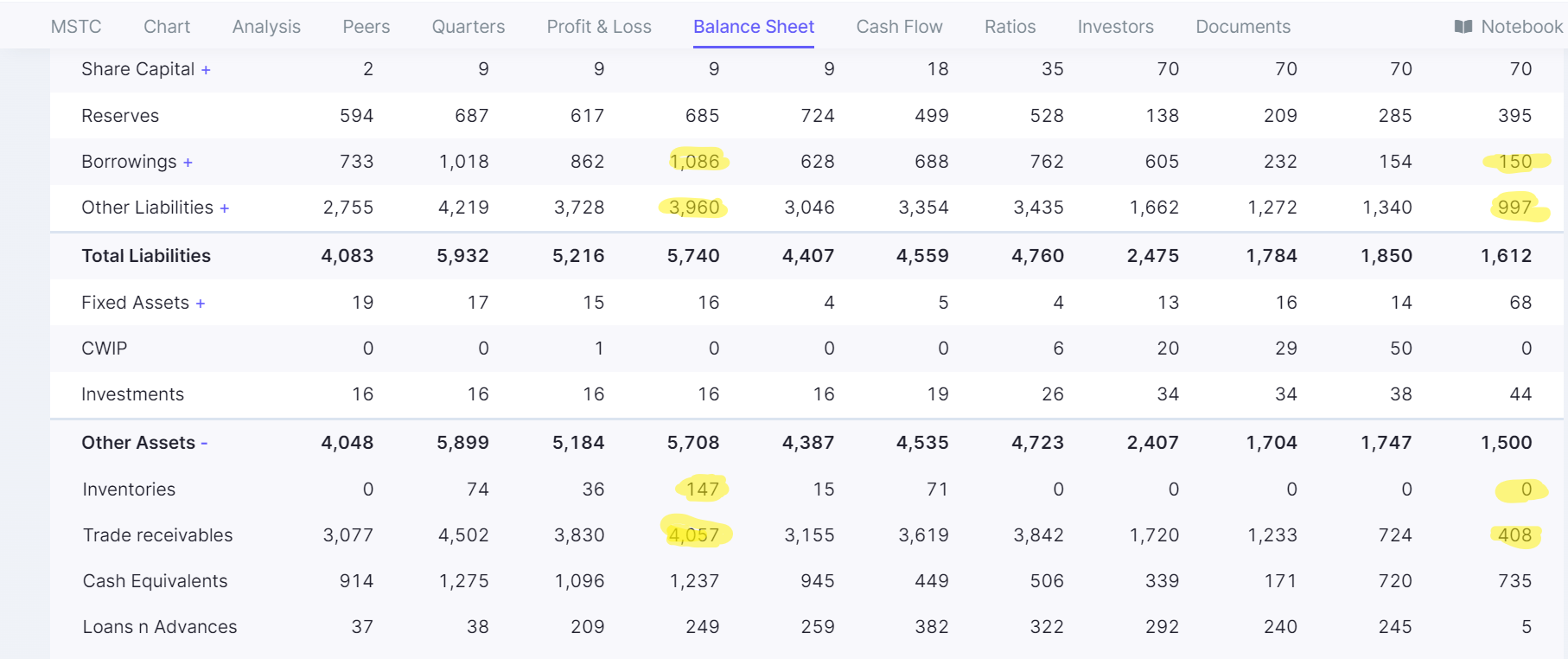

MSTC was into a completely different business until a few years ago. It was into scrap trading and that business had terrible receivable days and bad debts. It took the company multiple years of write offs to wipe them out. But today, their focus is completely on the e-commerce unit and all other divisions are either been shut down or sold off.

Look at how beautifully the balance sheet has been cleaned up. From borrowings to trade receivable to trade payables, all of them have been significantly reduced to move towards an asset light e-commerce model

2. E-commerce revenues, profit and growth looks robust

| 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | ||

|---|---|---|---|---|---|---|---|---|

| Revenue | ||||||||

| Marketing | 2811 | 1326 | 2262 | 2748 | 646 | 406 | 413 | |

| E-commerce | 127 | 161 | 190 | 213 | 202 | 221 | 294 | |

| Others | 21 | 59 | 6 | 7 | 43 | 11 | 0 | |

| Scrap | 346 | 328 | 339 | 378 | 409 | 364 | 415 |

Look at the revenues for the e-commerce division. It has been growing every year at a steady pace. The overall growth has been 15% cagr from 2016-22. This shows that the business is not cyclical or one off.

The revenues are also well diversified with less dependence on any single customer. Even though the GOI is the major customer, MSTC has contracts with most of the state governments, union territories and PSUs and not just the central government. They have also started to enter the private space and have contracts from Reliance, Vedanta, etc. The management has taken active efforts in reducing dependencies on scrap auctions and diversifying in other segments (coal auctions, telecom, NPA auctions, Property, etc)

If you read the news, you might have noticed every other day there is some news on new items being auctioned off on MSTC. The government wants to ensure a transparent way to auction and hence the growth is very real and very visible.

All of these are auctioned off on MSTC

3. The company is massively undervalued

Current Market cap – 1780 cr

Standalone cash on books – 780 cr

Subsidiary FSNL valuation – 400 cr (roughly)

The procedure for sale of FSNL has already been started and looks like it might be completed soon. As per last financial year, FSNL had revenues of 405 cr and PAT of 40 cr. It has cash on books worth 161 cr. It has no long-term debt. Looking at all of this, 400 crore seems like a conservative valuation.

So overall MSTC is available at a net value of 600 cr. All this for a company that has no long-term debt, has a steady e-commerce business growing every year and made 200 crores of net profit last year. The cherry on top is the 5% dividend yield the company is available at right now.

There is also the optionality of benefiting from the vehicle scrappage policy. MSTC has a 50-50 JV with Mahindra called Cero, focused on vehicle scrapping. Though real growth may be a few years away, Cero will have some early mover advantage.

The obvious and major risk here is that MSTC is a PSU company after all. Like most investors, I am no fan of GOI as an owner, but I also believe there is a price for every asset no matter what. After the sale, MSTC will be available at less than 3x EV/EBIDTA. For a diversified & growing asset light e-commerce company with optionalities and regular dividend payouts, this seems incredibly low.

| Subscribe To Our Free Newsletter |