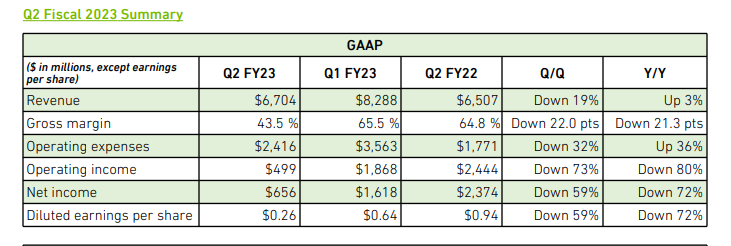

NVIDIA earnings out – (they did a preliminary release on 8th August to warn about shortfall)

Post the pre announcement of earnings… the gross margin will be a shocker for the market. Because nvda has set the bar for > 60% gross margins for long.

From earnings call:

- Intel Sapphire rapids delay has created some problem

OK. Our Hopper supports previous-generation CPUs. But I guess, next-generation GPUs – CPUs, Sapphire Rapids and Genoa after that, as well as Graviton. And so we certify and test across all of the CPUs because the cloud service providers demand it.

And they intend to deploy NVIDIA accelerators, NVIDIA Hoppers, across a large number of CPUs. There is no question that the delay is disruptive and a lot of engineers have to scramble. It would have been a lot easier if next-generation CPUs were to have executed more perfectly. However, Hopper goes into an environment with CSPs where they connect our PCI Express connectors to old-generation, current-generation CPUs as well.

→ More sales for AMD CPUs until intel SPR/nvidia grace CPUs come in.

- Unable to say how much the decline is contributed by crypto!!!

We are unable to accurately quantify the extent to which reduced crypto money contributed to the decline in Gaming demand. While Gaming navigates significant short-term macroeconomic challenges, we believe the long-term fundamentals in Gaming remain strong.

→ We will know in two quarters. This cannot be hidden like earlier when only NVDA was running the show. Since now AMD gaming data will come in and we can see how much gaming recovers from Q4 onwards – Some history. SEC.gov | SEC Charges NVIDIA Corporation with Inadequate Disclosures about Impact of Cryptomining

So our gross margins outside of the inventory charges in Q2, as well as going into Q3 is really about our sales mix that we have and probably also to understand that our sales mix in the next quarter for GPUs is not in the high end. And so that has impacted our gross margin as we move into Q3.

You are correct. We do expect that Data Center will assist in our gross margins, but we also have growth plans in Auto. Auto is below our company average, and so that will tend to offset some of those upper-bound things that we will see in terms of Data Center.

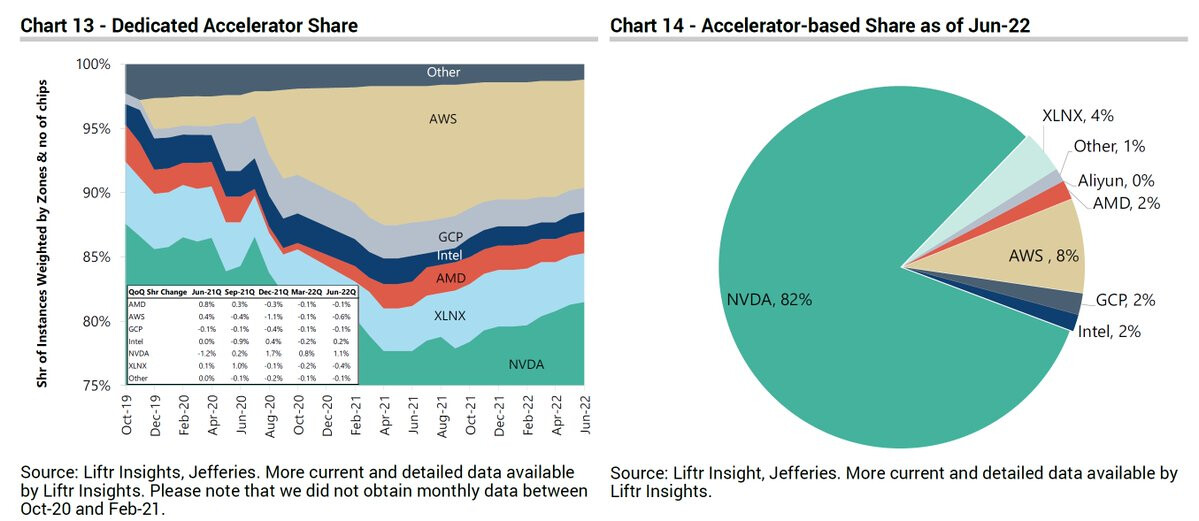

Long term still good. But it does hurt to be a market leader in retail when competition comes in. Also notice the stickiness of data center. One reason we focus on datacenter. Data center accelerator space, nvidia owns it… based on the charts shown below

I will put in some more personal banter on this in my next post.

| Subscribe To Our Free Newsletter |