Earnings call transcript link here

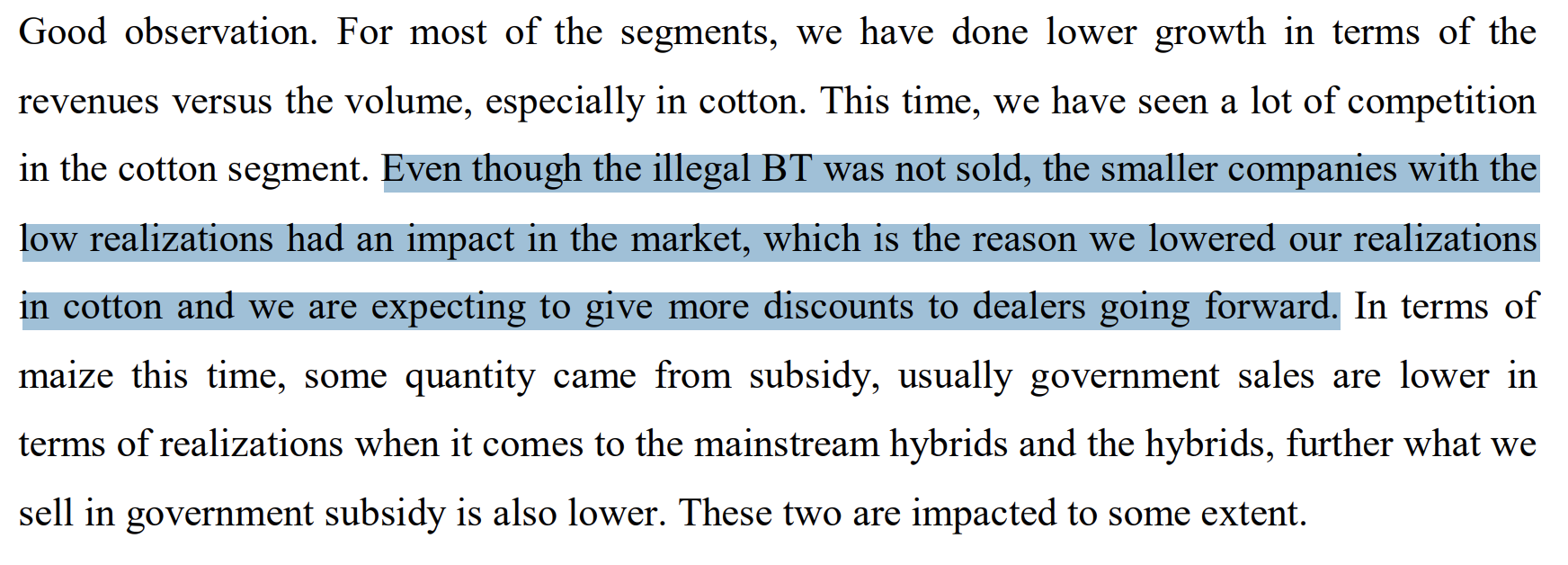

Seems they don’t have much pricing power as their volumes have been increasing yet their revenue has been stagnant. Besides, this time, the excuse of illegal BT is not valid as well. This is a bit of concern.

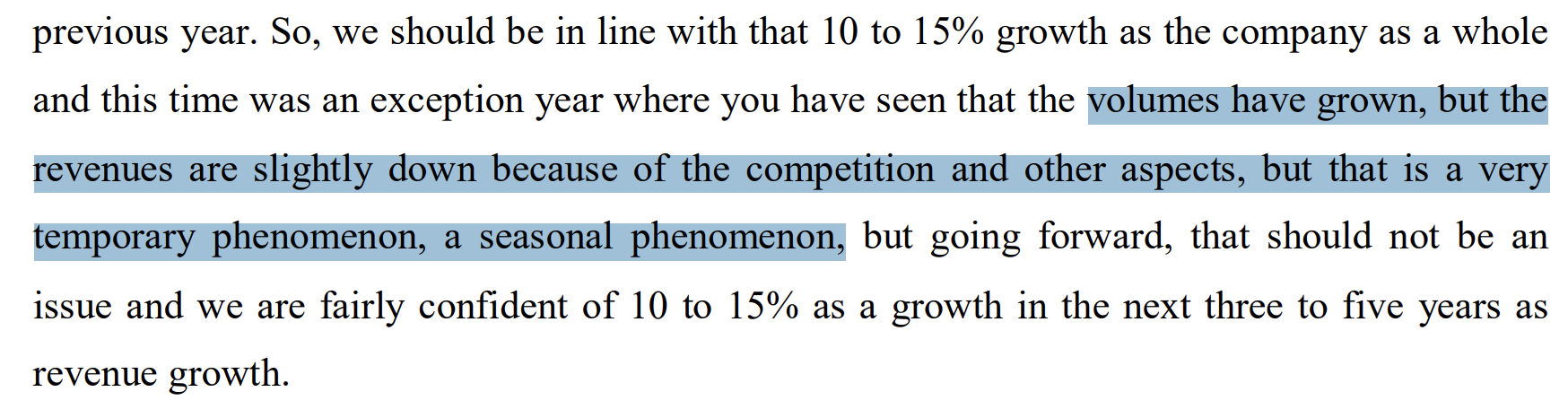

However, the mgmt is quite confident that this is a temporary phenomenon. They mentioned this almost 3 times during earnings call.

The mgmt seem to be conservative and shareholder friendly. Besides, there is a huge barrier to entry. A single hybrid seed would take 2-3 years to be grown and then has a life of 3-4 years. This long cycle, coupled with huge R&D spend is something that can keep competitors at bay.

Need to watch for margin improvements in next few quarters. The R&D efforts and CAPEX should ideally result in more volume growth and margins should revert back to usual. In thats the case, the earnings would improve and potentially PE rerating would occur.

Disc: Invested and might be biased

| Subscribe To Our Free Newsletter |