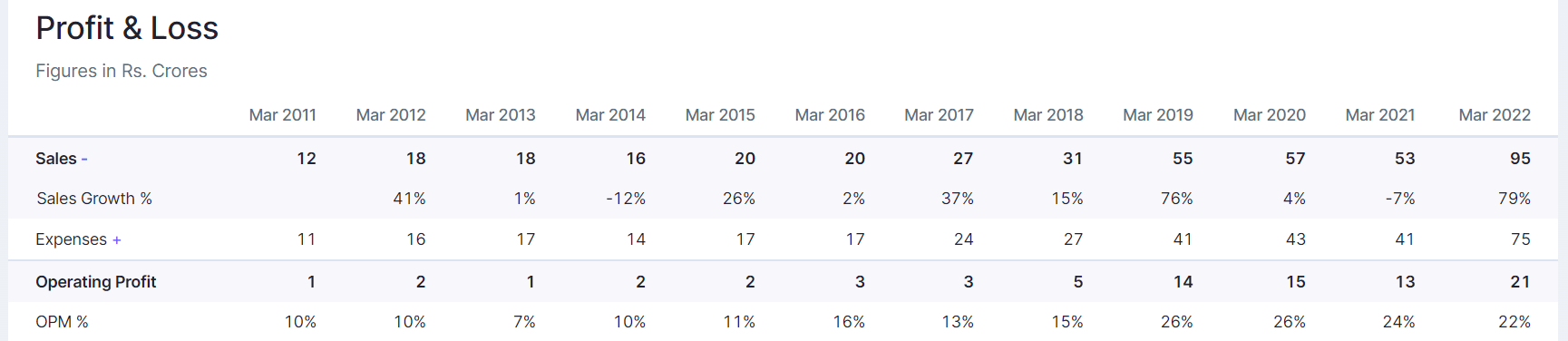

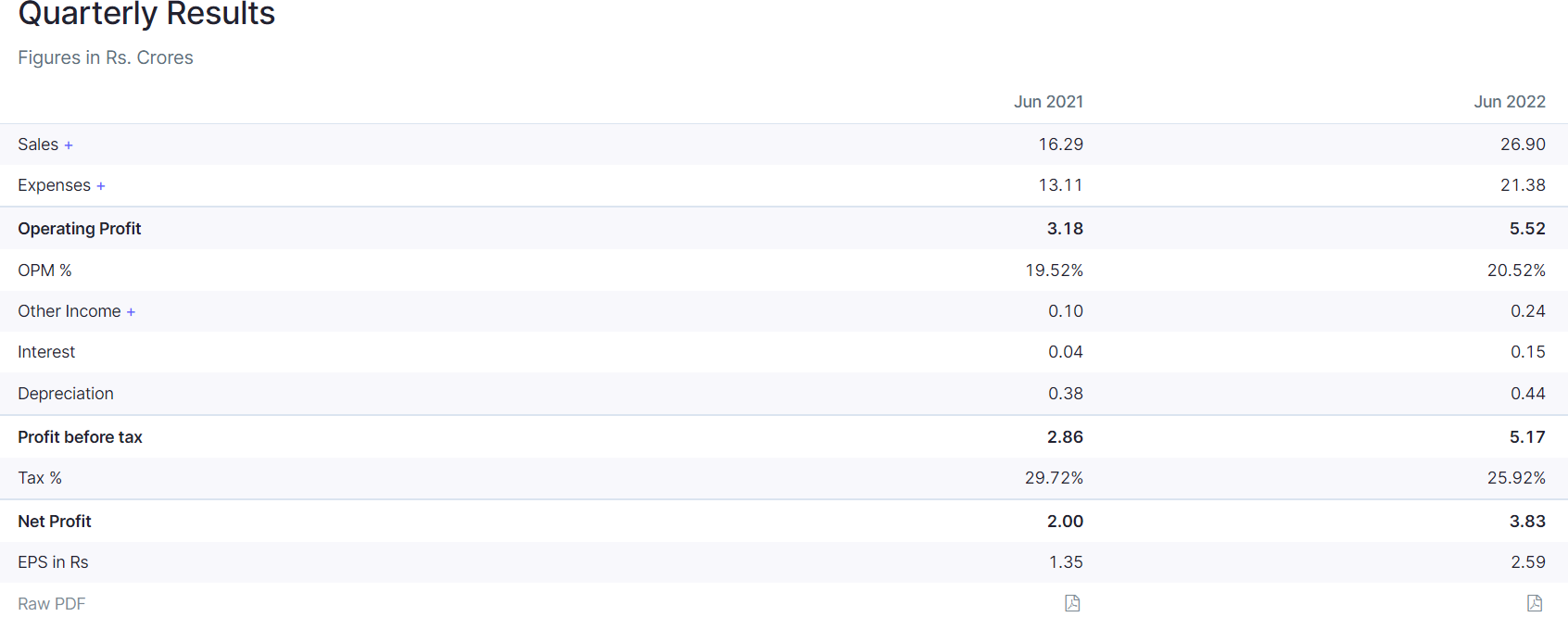

I think Chemcrux had posted a very good performance. The company was on a flat revenue for last 3 years and look at the jump in FY22. They did almost 27cr in Q1 vs 16.3 cr yoy. So even without the new capacity they have been able to post this good performance. We should also keep in mind that many chemical cos margins have come off sharply, some have barely posted profits.

Here is a guy who posted great numbers and managed very well on margins. Its still early days but if they can keep at it, the new capacity will take CY 2025 numbers in another orbit. A company with 100 odd cr annual revenue is planning a capex of 80cr. That is a large number for a brownfield capacity. I feel it is checking all boxes for a big winner. Valuations are not cheap after the sharp move from 270 to 470. Theoretically, a 50 PE on TTM basis is 25PE 1 year fwd if they can double the profits. Need to get more details from the management about the capex surprise of 80cr vs 27cr earlier.

Discl: Invested

| Subscribe To Our Free Newsletter |