@Surender : Your question isn’t very clear, but I’m assuming that you are referring to the bidding for the prospective privatisation of the steel plant. Firstly, I definitely would not make any investment decision on based on this news considering the government’s sketchy track record of PSU privatisation (BPCL, SCI, BEML, etc.). The poor accessibility was the history of the location and not the current status. The mines are operational since several years and thousands of crores of equipment have been delivered to the steel plant. So it is obvious that the roads have been built by now. Both Transport Corporation of India (TCI) and Associated Road Carriers (ARC) have full fledged transport hubs in Jagdalpur. You can look up their Branch Office Locator for PIN Code 494001. Having said that, the rail network is still quite poor in this region owing to a topography of dense forests. So there is scope for improvement of road / rail infrastructure. But that’s not really in direct control of NMDC.

That’s why you need to study their Slurry Pipeline and Pellet Plant projects which will make the evacuation of the ores a lot easier. I will have to write a separate post on both of these, else this will become a very long essay. ![]()

@Gothamcapital: Same reply for your query as above; that I would not make any investment decision on whether any high profile investor / government is buying or selling shares of the company. This is because we have no prior information regarding what price and volume did they enter or exit. By the time the news comes out in public, it is stale and mostly irrelevant.

Regarding the core iron ore mining business, I would not base any investment decisions on the price movement of iron ore as that is akin to astrology.

In order to invest in these types of companies, please study the following:

- Ore quality (concentration of minerals) and quantity of extractable reserves

- Ease of extraction (surface level ores or deep underground mines)

- Ease of evacuation (connectivity to the location of consumption)

- Longevity of the mining license and royalty pay-out to the Government

- Long term tie ups with downstream consumers and ability to be a price maker instead of being a pure price taker (no one can completely dictate prices, but at least they should have some bargaining power)

- Track record of the miner (following environment / safety norms / accidents, etc, relationship with government & people around the plant)

NMDC controls nearly 30% of the iron ore market in India. So it has decent bargaining power, especially with the smaller buyers that they can sell through auctions, since JSW and Arcelor Mittal (former Essar Steel) are now trying to use their own captive mines.

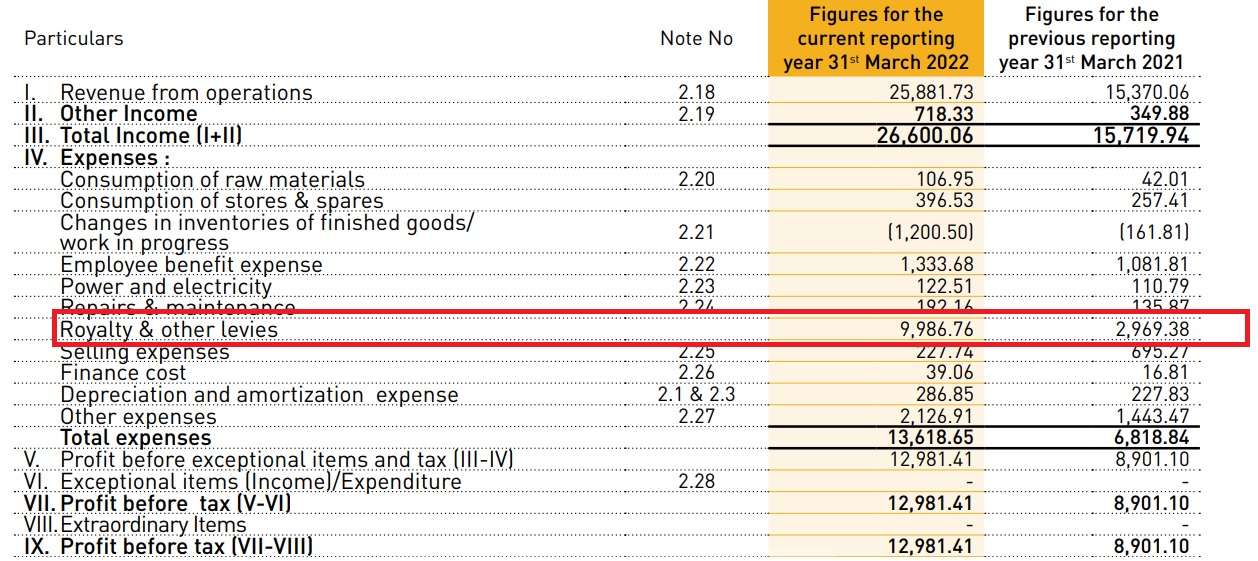

The biggest hit on NMDC’s profitability is the increase in Royalties. From Rs. 2969 crores in March 2021, it has gone up to Rs. 9,986 crores in March 2022.

If the government gets too greedy with royalties / levies / taxes, it can be trouble for the entire mining industry and not just NMDC (remember telecom licences?). On the flip side, it also means that new entrants will find it that much tougher to venture into the mining business and compete with the incumbents.

I read a lot of comments from the investor community that all commodity business are brutal and that any tom-dick-harry can come and suddenly increasing supply. However, that is not a very accurate way of assessing the business especially in the backdrop of high pro-ESG stand by governments, investors and public sentiment. It takes years to operationalise mines or steel plants and start commercial production.

This doesn’t mean that steels and mining businesses should be trading at P/B of 4 or 5. However, I feel that the present share prices are unduly pessimistic. With 12% dividend yield, the current prices offer decent margin of safety ( I of course could be wrong and you need to do your own research).

| Subscribe To Our Free Newsletter |