I had looked at Rossell few weeks back and in the couple of hours I spent, I came away with so many questions and doubts. I see that this company has piqued the interest of the investing community due to this Techsys division’s foray into aviation/defense manufacturing. It does sound exciting but this did not pass some of my basic filters and smell tests.

- We would assume this is high-tech vertical in the defence space but looking at the margins doesn’t seem to say so.

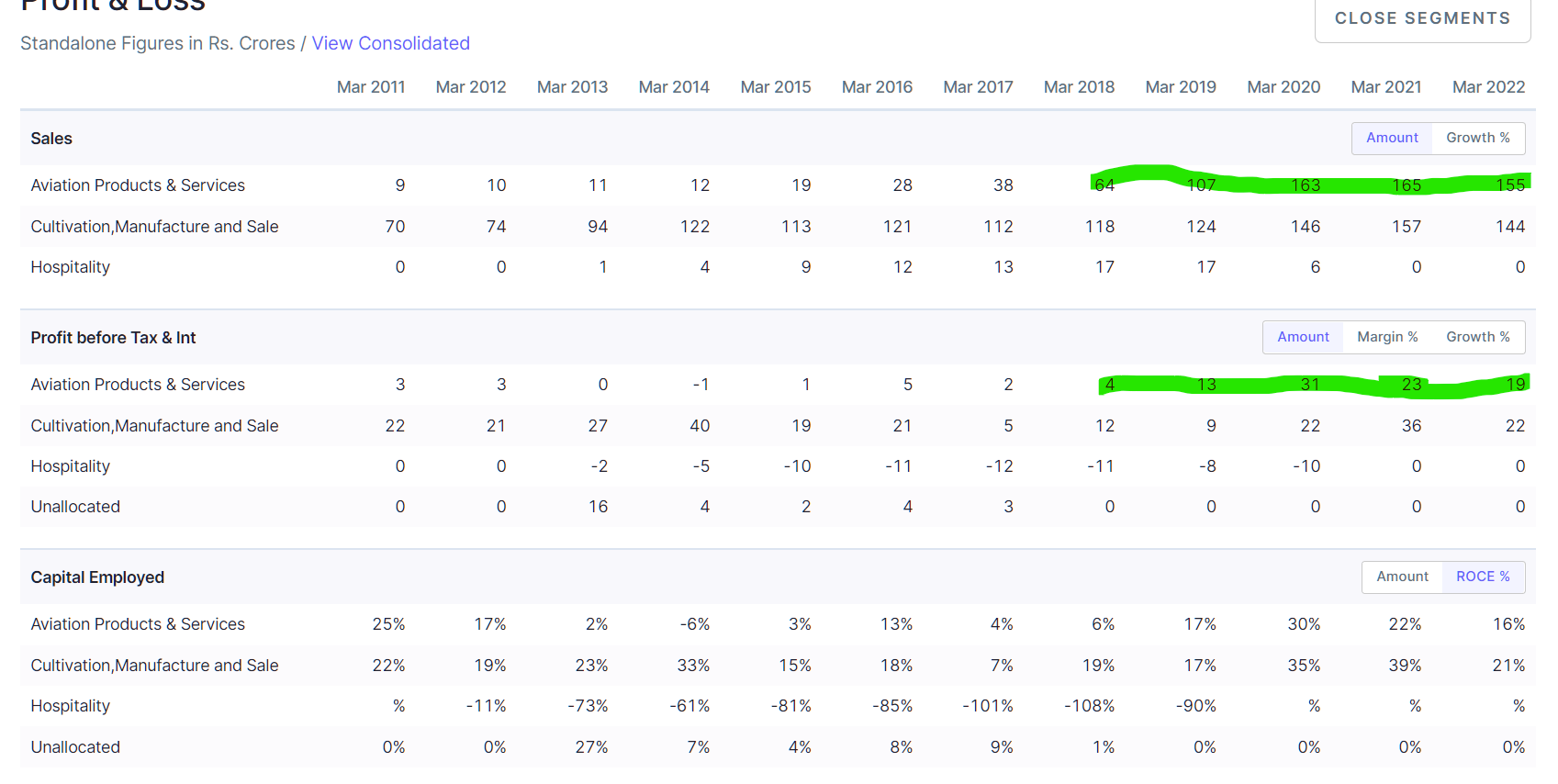

Although the topline has grown consistently, the margins between FY18-FY22 has gone like this 6% → 12% → 19% → 14% → 12%. That’s a wide range and a lot of variation. This does not give the impression of a business doing a lot of value-add. It means that the value-add is minimal/marginal and is being drowned out by the variation in gross margins?

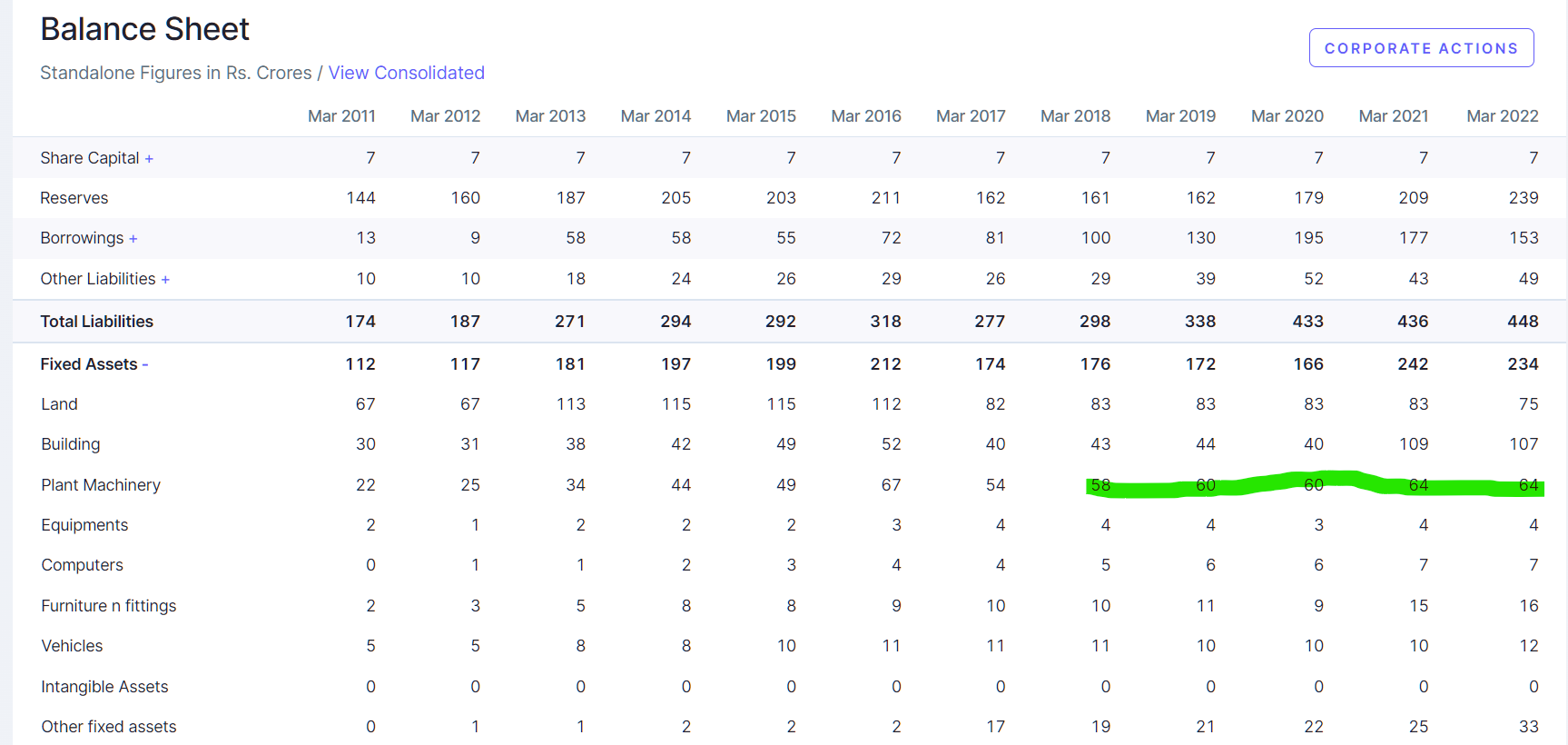

- While the topline has grown from 64 Cr to 155 Cr. Has the company put up any capex in plant and machinery to handle these new orders?

Clearly, this business doesn’t need a lot of investment in plant & machinery, so the possibility is that this is a very labour intensive business and probably the value-add in this business is purely labour? That might also explain the good RoCE (Tea is a labour intensive industry – so this business is more close to Tea business than a pure-play defense business like HAL with 24% OPM and ~55% GM?) So does it mean that when this business get a 2000 Cr order, they will have to hire a lot of labour to scale?

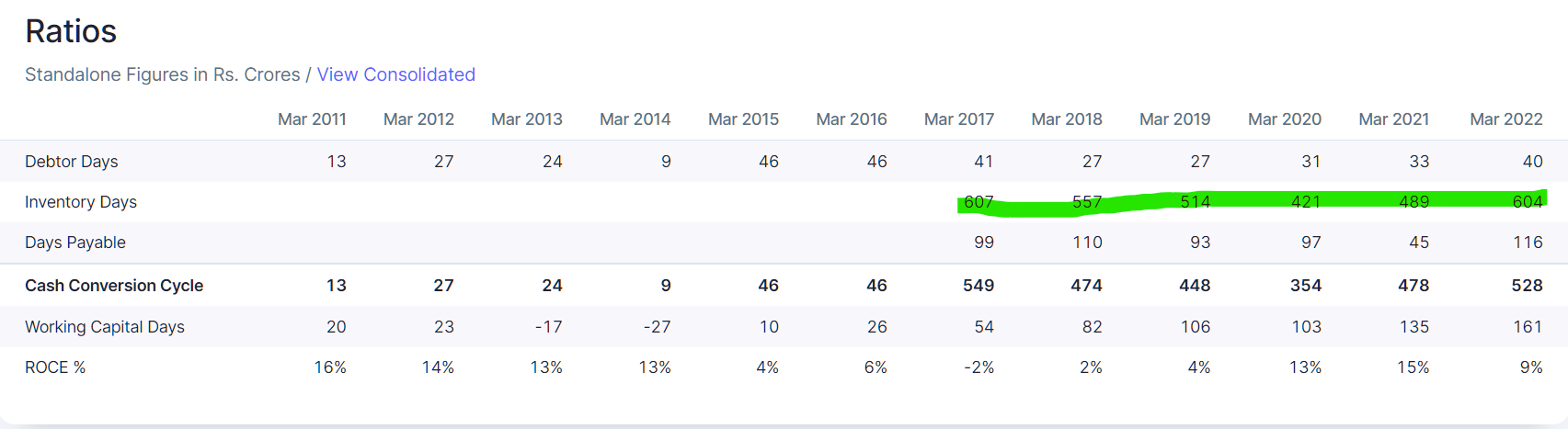

- Another line of thought, that jumps up when looking at Inventory days.

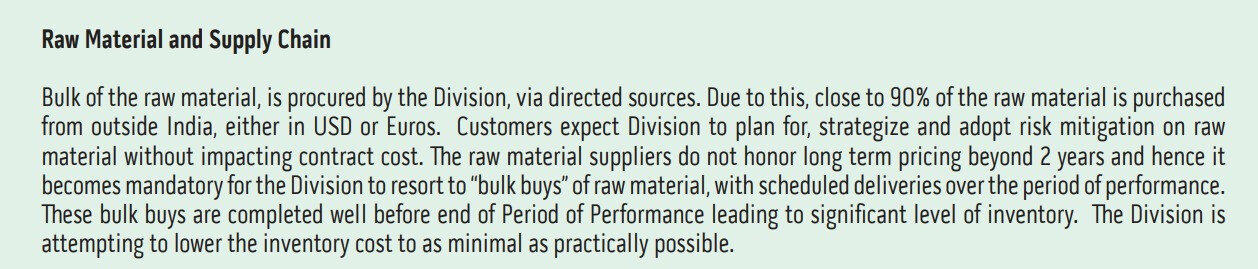

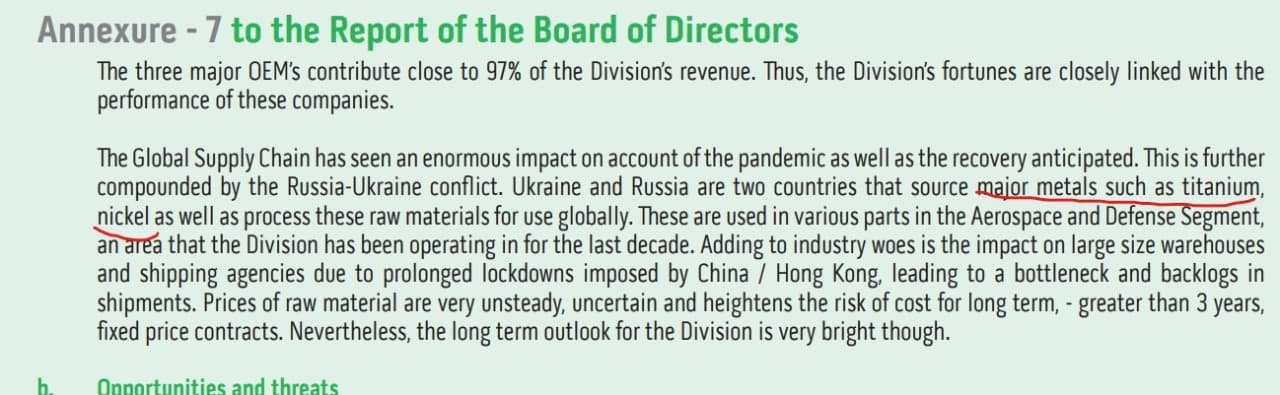

The inventory days are awfully high. That’s like a 1.5 years or so! No other tea business has such poor cash conversion cycle. So clearly this has something to do with Techsys division. They have to procure RM and perform labour-intensive tasks on it for a year or more before they can ship? Does the vendor cover forex fluctuations? The management seems to think that Rupee depreciation is a natual hedge. What happens when Rupee appreciates instead?

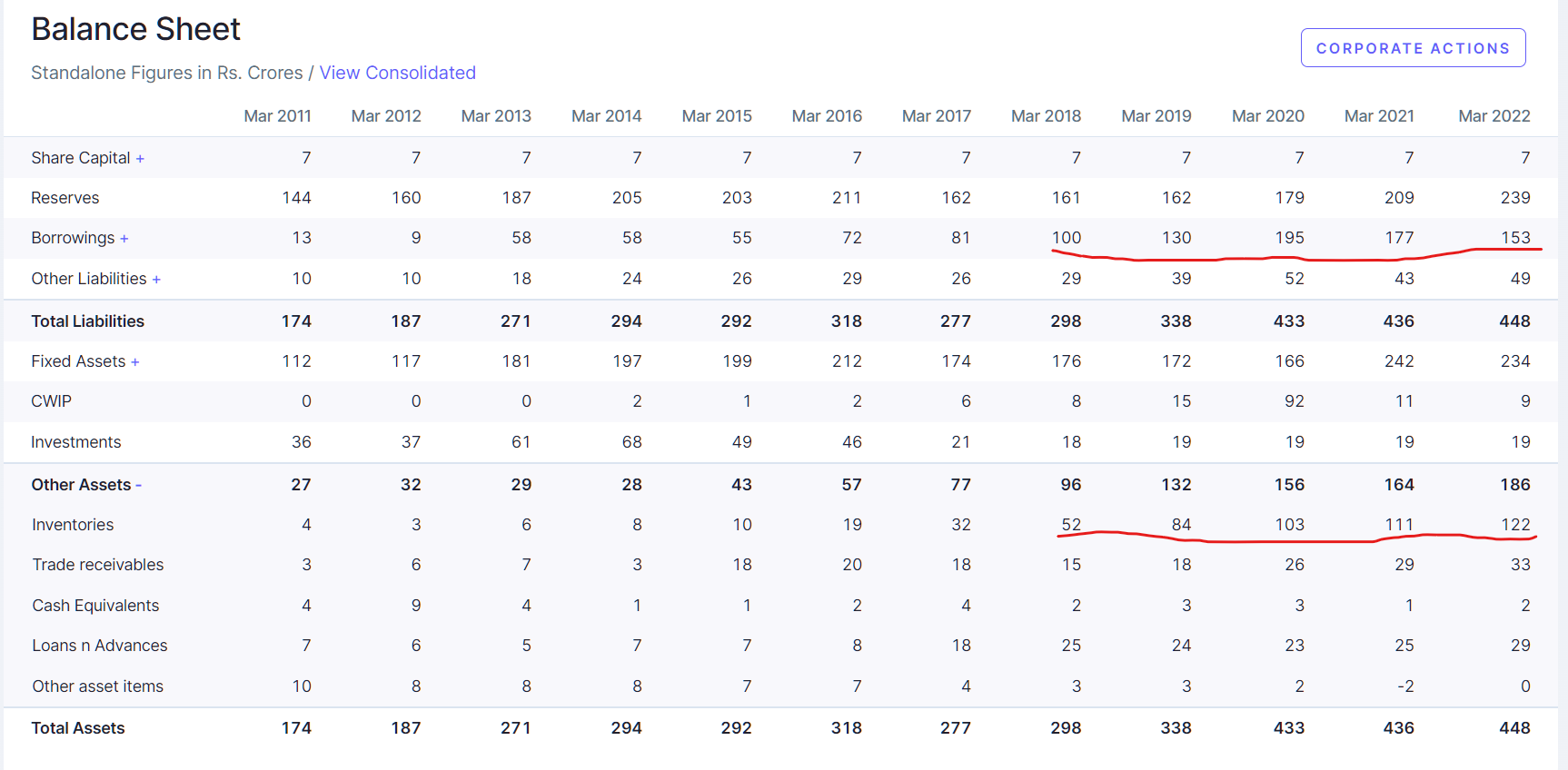

- So who funds this inventory? Do they have a relationship with Boeing or whoever to fund this liability? Looking the balance sheet sheds some light

So these guys have to borrow to buy whatever this commodity is on their own for orders to be delivered 1.5-2 years later. So a 2000 Cr order might mean they may have to borrow 1200-1500 Cr and trust the Rupee to be a natural hedge? (90% of RM is imported)

If you see the above two, the RM price fluctuates over the long-term a fair bit and going by back of the envelope calculations, the Gross Margins here may not be more than 20% and the labour value-add perhaps around 5% (Am assuming this is unskilled labour with a low-wage)

The worst case for this company is when they win a 2000 Cr order, raise debt and buy inventory and RM price crashes over the next year and Rupee appreciates. It can essentially wipe-out everything.

Again, I am making a lot of guesswork here because the AR or AGM transcript is so opaque. So many good questions asked by participants and the answers by the management are outright comical (in my opinion)

Whenever I see stuff like this, I run away.

Disc: Just a customary glance and not invested due to lack of clarity and what I consider are red flags. Posting here because I might be missing something.

| Subscribe To Our Free Newsletter |